- Quick take

Poland’s current account balance improves due to seasonally higher EU transfers

- 14 December 2022

- Poland

Poland's external current account balance improved in October on the back of seasonally higher transfers from the EU budget. The merchandise trade gap remains large but seems to have stabilised

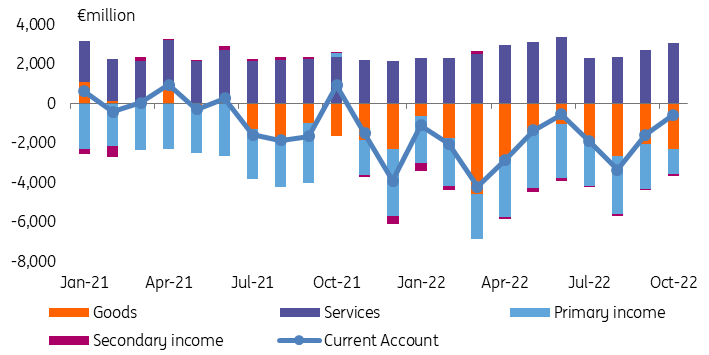

Poland's current account deficit was €0.5bn in October, clearly below the consensus of €0.8bn and quite close to our forecast of €0.3bn, following a deficit of €1.6bn in September. On a 12-month basis, we estimate that the balance deteriorated slightly to about -3.9% of GDP from -3.7% of GDP in September (we recorded a sizable surplus in October 2021). The goods trade deficit was €2.3bn in October, from €2.1bn in September. In cumulative terms, the trade balance deteriorated to about -4.0% of GDP from -3.8% of GDP a month earlier. A high surplus in the services balance of €3.1m fully offset a gap in primary income of €1.3bn and a slightly negative secondary income balance of €0.1bn. The seasonally low deficit in primary income was due to the high inflow of EU funds (more than €1.6bn, according to the National Bank of Poland).

Foreign trade turnover, calculated in euros, is growing at a rate close to 25% year-on-year, but this is mainly due to increases in export and import transaction prices. The annual growth rate of merchandise imports (24.6% YoY) only slightly exceeded that of exports (23.7%), and this was the smallest difference recorded since April 2021. Polish companies are taking advantage of opportunities to increase foreign sales due to the weakening zloty and the easing of tensions in global supply chains, in particular in the automotive industry.

The NBP communiqué states that in October, export growth was driven by sales in the automotive industry benefiting from improved availability of key components, which boosted the European automotive sector. This was reflected in both exports of vehicles (cars, vans and road tractors) as well as spare parts (including batteries and engines). Food also recorded a sizeable expansion. On the import side, a slowdown in import growth was particularly visible in iron and steel and plastics, which indicates weak domestic demand. Large increases were recorded in imports of fuel, due to both continued high prices and rising volumes (the value of coal imports was a record high, while imports of oil was the highest since 2019).

Today's data is neutral for the zloty exchange rate, with the current account deficit turning out to be slightly lower than the consensus. However, the zloty exchange rate has recently been influenced by global factors as well as this week's decisions on interest rate hikes by the US Federal Reserve, European Central Bank and other central banks, and expectations on unlocking EU funds from the Recovery Fund. We expect a gradual widening of the current account deficit in the reminder of the year, and forecast a 4.2% GDP deficit for 2022 as a whole. Our latest Directional Economics presents long-term projections for Poland.

Current account balance and its components

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more