- Quick take

- 16 March

- Poland

Poland posted a sizeable current account surplus in January, prior to the energy price shock

Poland’s current and merchandise trade balances in January surprised on the positive side, ahead of the sharp rise in global energy commodity prices in March. We are not concerned about Poland’s solid external position, which is set to deteriorate moderately, and from a low base

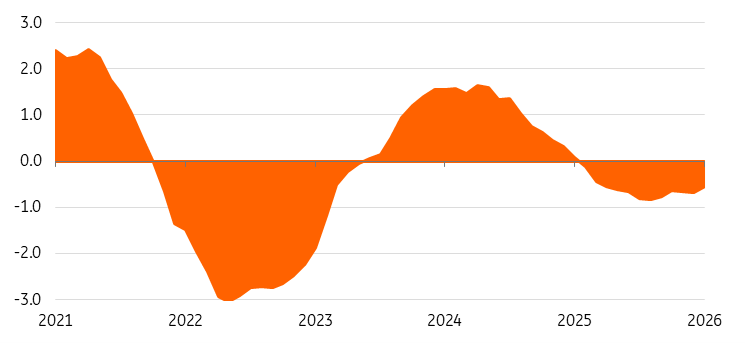

In January, the current account recorded an unexpectedly high surplus of €1,153 million (consensus: -€295 million, our forecast: +€291 million), compared to a deficit of €1,698 million in December 2025. As a result, on a 12-month cumulative basis, the current account deficit fell to 0.6% of GDP from 0.7% of GDP at the end of 2025.

The surplus in the current account in January was the result of: a merchandise goods surplus of €378 million (after a deficit of €2,298 million the previous month), a traditionally high surplus in services trade of €3,276 million, and deficits in primary income (€2,417 million) and secondary income (€84 million).

The surplus in the merchandise goods account occurred alongside a marked decline in turnover: the value of exports expressed in euros fell by 1.8% year-on-year, while imports dropped by as much as 6.1% YoY, whereas in December turnover jumped by 9.7% and 10.1% YoY, respectively. This was due to one fewer working day than a year earlier, and the severe winter in January this year, which hampered activity in transport and logistics. In 12-month terms, the merchandise trade balance improved in January to -1.3% of GDP from -1.4% of GDP a month earlier.

National Bank of Poland (NBP) analysts’ commenting on changes in trade aggregates in zloty, point to a decline in trade turnover, which resulted from fewer working days than in the previous year. In January, a drop in export value was noted in the categories of investment and intermediate goods, and means of transport, while in agricultural products it was due to falling prices. The decline in imports was contributed to by a further drop in oil prices (which today sounds like ancient history) and a base effect. The NBP also mentions a decrease in the value of imports of intermediate and investment goods. Increases, meanwhile, were recorded in imports of passenger cars, computer parts, and iron and steel structures.

The war in the Middle East and higher prices for energy commodities, will somewhat disrupt Poland’s external equilibrium, but the disturbance should be much smaller in scale than in 2022. We estimate that if prices for crude oil and variable gas remain at US$100 per barrel and €50 per MWh, respectively, until the end of this year, and if imports of both commodities are comparable to 2025, import expenditure would rise by PLN26 billion, or about 0.6% of GDP. By comparison, in 2022, expenditure on oil and gas imports increased by 1.3% of GDP. Additionally, the starting point (forecast current account deficit of 0.9% of GDP this year) is low, which in the negative scenario of energy commodity prices would inflate the current account deficit to about 1.5% of GDP this year.

The level of external imbalance in Poland remains low and is largely irrelevant for the PLN exchange rate. The resilience of the Polish currency during times of severe turbulence on global markets may also be attributed to the activity of BGK development bank in the forex market. In the EUR/US$ market, the further course of the war in the Middle East and the expected decisions of global central banks will be of key importance. The zloty exchange rate will remain influenced by global factors as well as decisions and communications from the Monetary Policy Council.

Poland's current account balance, 12-month rolling, % of GDP

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more