- Quick take

- 13 March

- Poland

Petrol price surge puts Poland’s low‑inflation trajectory at risk

The January and February CPI readings of 2.1% were excellent, but now feel like a thing of the past, with oil prices surpassing US$100 per barrel, which has sent petrol prices soaring. In March, CPI may exceed 3%, and the overall inflation outlook has deteriorated. Monetary easing is off the agenda for now

Inflation below target at the beginning of the year

In February, CPI inflation was 2.1% year-on-year – unchanged from the January reading (revised from 2.2%YoY) and still below the National Bank of Poland (NBP) target of 2.5% (+/- 1 percentage point).

There were no significant changes in the annual trends of the major CPI basket categories in February compared with January.

Prices of food and non-alcoholic beverages were up by 2.4% YoY (same as in January), while prices in transport fell by 5.7%YoY after a decline of 5.8%YoY in the previous month. Higher growth was reported in the costs related to housing and house energy (4.3% YoY vs. 3.8% YoY). There was a notable slowdown in the prices of recreation, sport and culture (2.4% YoY vs. 4.3%YoY in January).

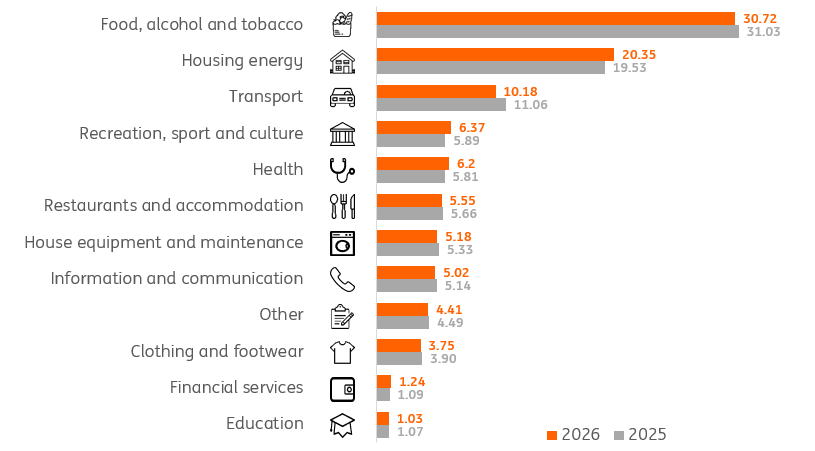

New basket weights broadly neutral for inflation

Traditionally, the StatOffice updates the CPI basket weights in March. Last year, it reduced the January figure by 0.4 percentage points, but this year its impact was negligible (around 0.1 pp). The biggest increase was in “housing, water, electricity, gas and other fuels” – from 19.53% in 2025 to 29.35% in 2026 – as costs linked to housing rose faster than overall inflation last year. A substantial decline in weight took place in the case of tobacco and alcoholic beverages (from 5.19% to 4.81%) and outlays linked to transport (down from 11.07% to 10.18%).

Core inflation probably continued moderating

With relatively stable annual growth of food prices in the first two months of 2026 compared to December last year, the decline in headline inflation from 2.4% YoY at the end of 2025 to 2.1% YoY at the beginning of this year was probably driven by the decline in core inflation. We estimate it moderated to 2.4-2.5% YoY, down from 2.7% YoY in December.

Inflation outlook deteriorates amid Middle East conflict...

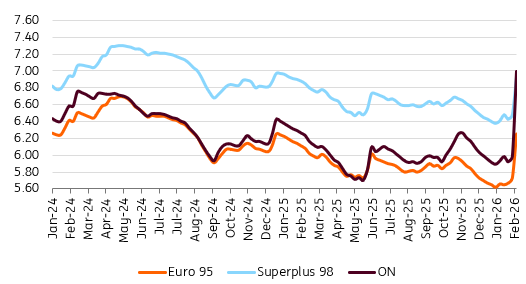

Data for January and February now look outdated, as March has brought a marked shift in the inflation outlook due to the war in Iran. Whereas the earlier environment was dominated by disinflationary forces – slowing wage growth, favourable food market conditions, cheap imports from China, and stable energy prices – the blockade of the Strait of Hormuz and the resulting surge in oil and gas prices now constitute a significant pro‑inflationary shock. The impact of the energy crisis on inflation will depend on how long the conflict in the Middle East lasts. At the same time, the scale of the shock is so far clearly smaller than in 2022 (particularly in the case of gas prices) and is unfolding under different macroeconomic conditions.

The situation remains fluid, but our previous forecast of average annual inflation close to 2% is now outdated. We currently expect consumer prices to rise by around 2.5% this year, with upside risks should the conflict persist. Average retail fuel prices in the first half of March were roughly 15% higher than the February average. If this increase in fuel prices is maintained, it could lift March inflation by about 0.8 percentage points, and the headline rate may exceed 3% YoY.

.… leaving little to no room for further rate cuts in Poland

Although the rise in oil prices is primarily a supply‑side shock, it may nevertheless fuel inflation expectations and generate second‑round effects, pushing up the medium‑term cost of transported goods.

In the current environment, the Monetary Policy Council (RPP) has effectively shifted to a ‘wait‑and‑see’ mode. Over the coming months, interest rates set by the National Bank of Poland are likely to remain unchanged. Should the period of energy market turbulence prove short‑lived, and the July NBP projection continue to show favourable inflation prospects, a further 25bp rate cut in the second half of the year cannot be ruled out.

However, a scenario in which monetary policy remains on hold throughout the year is also highly plausible. Previously, we had assumed a decline in NBP rates to 3.25%, but under current global conditions, this no longer appears feasible. For the time being, monetary easing is off the agenda.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more