- Quick take

Poland: Buoyant growth allows MPC to focus on fighting inflation

- 17 May 2022

- Poland

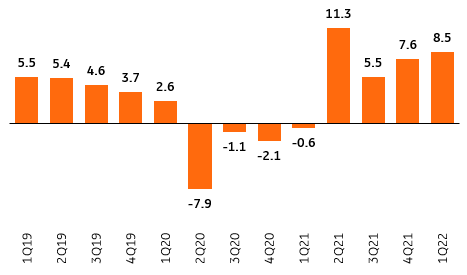

In the first quarter, Poland’s GDP went up by 8.5% year-on-year vs. 7.6% year-on-year in 4Q21. This is in line with our estimate and above market expectations. In the near term, GDP will be close to its potential so the MPC should not be concerned about the labour market outlook and will continue monetary tightening. We still foresee terminal rate at 8.5%

In the first quarter of 2022, Poland’s GDP jumped up by 8.5% year-on-year vs. 7.6% year-on-year in the fourth quarter of 2021. This reading matched our expectations and exceeded the market consensus of 8.1% year-on-year. Economic growth accelerated from 1.8% quarter-on-quarter, seasonally-adjusted in 4Q21 to 2.4% quarter-on-quarter, seasonally-adjusted in 1Q22. Detailed data on GDP composition will be unveiled on 31 May, but in our view, economic growth was still driven by robust household consumption and solid fixed investment, as suggested by data on construction output in 1Q22. At the same time, businesses continued restocking their inventories of inputs, which contributed markedly to GDP growth in 1Q22.

A high starting point means that, on average, GDP will rise by more than 4% this year despite the expected cooling of economic conditions in the coming quarters. The solid average figure somewhat blurs the deteriorating outlook. At the end of 2022 annual GDP growth is projected to moderate below 2% year-on-year.

According to our estimates, upcoming quarters will bring GDP towards its potential, so the Monetary Policy Council (MPC) will continue its monetary tightening cycle. Policymakers will focus on fighting inflation amid a lack of serious concerns about labour market prospects. The continuation of the consumption boom, boosted additionally by fiscal expansion, translates into persistent upward pressure on prices. We continue stressing the strength of the second-round effect and the fact that the recent upswing in costs of energy, materials, transport and labour is not yet fully reflected in retail prices and this process will be continued. As a result, the peak of inflation is still ahead as we expect CPI inflation to top around 15% year-on-year in 4Q22. The real interest rate remains deeply negative. Our baseline monetary scenario remains unchanged and assumes the main National Bank of Poland policy rate to be lifted to 7.5% in 2022. We still see the terminal rate at 8.5%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more