- Quick take

Philippines: Central bank’s dovish hike points to currency weakness ahead

- 23 June 2022

- Philippines

The Philippines' central bank, Bangko Sentral ng Pilipinas (BSP) hiked rates by 25 bps, signalling a gradual hike cycle and a weaker peso

| 2.5% |

BSP policy rate |

| As expected | |

BSP sticks to dovish ways

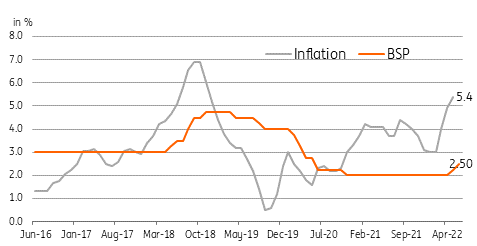

The BSP hiked policy rates by 25 bps, a move anticipated by the majority of market participants, taking the overnight repurchase rate to 2.5%. Incoming BSP Governor, Felipe Medalla, telegraphed a modest rate hike for today’s meeting while also indicating a preference for a potential follow-up 25 bps hike at the August meeting. The central bank prefers the relatively less aggressive pace of tightening pointing to the need to support growth. Despite inflation blowing past target again this year, the BSP believes that the current surge in prices is largely cost-push and therefore does not warrant an aggressive rate hike cycle. Latest BSP forecasts point to inflation breaching its target both in 2022 (5%) and 2023 (4.2%).

BSP carries out dovish hike despite expected inflation breach in 2022 and 2023

Up ahead: faster inflation and weaker PHP

With the BSP signalling its preference for a dovish rate hike cycle in the face of aggressive tightening from global central banks, we can expect even faster inflation and a weaker peso for the rest of the year. PHP recently tumbled to multi-year weakness in rection to dovish rhetoric from the Bank and we could see the currency come under added pressure especially with the Fed signalling as much as 75 bps worth of tightening at the July meeting. Domestic inflation is currently at 5.4% and we could see price pressures push up the headline number past 6% in the next month due to still elevated commodity prices and a weaker currency fanning imported inflation pressures. We will need to revisit our PHP and inflation forecasts but we will likely adjust both given BSP’s dovish leaning in contrast to the more hawkish Fed.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more