- Quick take

- 21 September 2023

- Romania

Monitoring Romania

Romania's economy has been slowing and this has been filtering through into most sectors since the second quarter. This has led to below-plan budget revenues, forcing the government to propose some rather unpopular fiscal measures aimed at containing the deficit. This has some potential to dampen growth in 2024

Authors

A snapshot of Romania’s economy

- GDP: We have revised our 2023 growth forecast from 2.5% to 1.5% based on a slightly disappointing first half of the year and limited prospects for an acceleration in the second part. We are also revising lower our long-standing GDP estimate of 3.7% for 2024 as we now expect real growth of only 2.8%.

- Inflation: We now see the year-end inflation rate at 7.1%, slightly higher than our previous 6.9% estimate but still consistently below most market estimates. For the end of 2024, we expect inflation to decline to 4.0%, although the intra-year profile could be higher than previously estimated.

- Fiscal: Discussions about the fiscal reform have been all over the place in the last few months. While at the moment there is an official fiscal package being proposed, we still don’t know the new budget deficit targets. Based on current information, we estimate that in 2023 the budget deficit will be around 5.5% of GDP; it should decline toward the 4.0% area in 2024 and possibly closer to 3.0% of GDP in 2025.

- Monetary policy: We believe that rate cuts can be excluded this year and that the start of the easing cycle should come in the first quarter of next year, with a total of 150bp cuts by year-end. This might be done alongside the gradual restriction on liquidity conditions in the interbank market. Should the disinflation path disappoint, the probability of a higher-for-longer rates scenario materially increases.

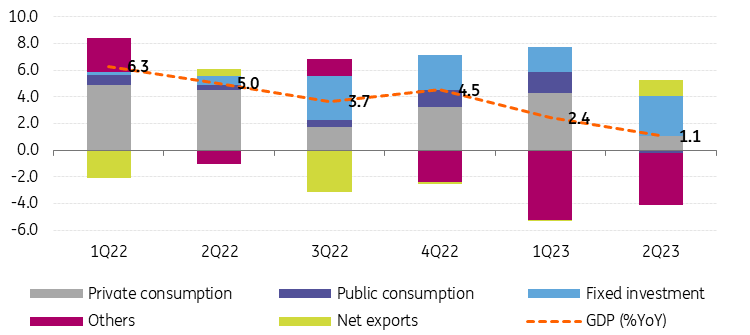

GDP growth: from resilience to weakness

Annual growth in Romania slowed significantly to an average of 1.7% over the first half of the year, down from 5.7% in the same period of 2022. Weaker private and public spending, as well as exports, took their toll on production output, most likely the result of high interest rates starting to bite and worsening demand from key trading partners in the eurozone. That said, fixed investment stemming from EU-funded public infrastructure projects kept the economy afloat, overtaking private consumption and accounting for the lion’s share of growth contribution.

On the supply side of the economy, with the notable exception of civil engineering-related activities, most manufacturing and services activities are now a drag on output growth.

GDP growth (YoY%)

July’s weak retail sales reading and the contraction in German industrial production reaffirm our view that Romania's economy will continue to slow in the second half of 2023. The weaker-than-expected tax collection over the summer months could be an early indication that the economy is already slowing below expectations. Furthermore, the higher tax burden and minimum wage increase agreed by the government coalition could be a drag on the supply side of the economy, especially if private consumption continues to remain weak as we expect.

For 2024, our view is that growth will accelerate but our forecasts remain below consensus at 2.8%, down from 3.7%. On the one hand, we think that next year’s four rounds of elections have the potential to slow the much-needed budget consolidation process, leading to overall stimulative fiscal policy. Moreover, rising wages will limit the downside to private consumption while the ongoing public investment projects should still support activity.

On the other hand, the latest fiscal package might add pressure to the disinflation process and growth, increasing the downside risks on growth and potentially leading to a higher-for-longer rates environment. Moreover, our view is that eurozone growth looks set to stagnate next year and not accelerate like the consensus believes, which doesn't bode well for Romania’s external sector.

Industrial production

Industrial production deteriorated further during the first half of 2023, following an already weak 2022. With two successive annual contractions in the first and second quarters, the manufacturing sector (which accounts for approximately 80% of the index), weighed on activity the most this year.

The energy sector experienced even larger year-on-year declines during the same period, while the mining sector’s rebound has contributed positively so far this year, contrasting with its negative 2022 contribution.

Industrial production by main groups

The latest confidence data for August do not point to any significant improvements, with declining order books remaining the key issue.

Looking ahead, we think that industrial activity will continue to remain weak. Indeed, easing supply chain pressures and favourable conditions in the gas market have supported and might continue to deflate input costs further – year-on-year producer prices fell marginally in July for the first time since October 2020. But with their levels still historically elevated, coupled with still-high interest rates and a gloomy outlook of the German economy – Romania’s key export market – industrial activity looks set to continue to be a drag on output.

Retail sales

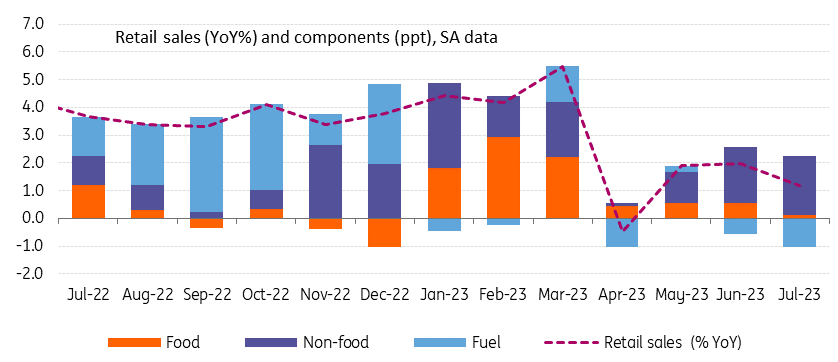

Retail sales advanced by 2.9% in annual terms in the first half of 2023, losing significant momentum compared to last year’s annual increase of 5.1%. The second quarter’s lacklustre performance was a key contributor to the overall slowdown. Moreover, with an annual increase of only 1.2% in July, retail sales experienced a weak start to the third quarter too.

Looking at the sectoral breakdown, key changes since the second quarter include the transition of fuel from a positive to a negative contributor, as well as the diminishing positive contribution of food items.

Flattening retail sales

So far, the numbers are consistent with a continued slowdown in private consumption, which we believe will continue. Admittedly, disposable incomes will find some support ahead from real wage growth, which we expect to remain positive for the foreseeable future due to both minimum wage hikes and lower inflation – impacted positively by the likely extension of the essential food items price cap by the government.

However, the possible negative impact of the new fiscal package on the labour market and inflation will likely limit these gains, limiting potential growth and even potentially leading to a higher-for-longer rates scenario. All told, we think that retail sales growth will continue to remain relatively weak, with better wages and the general electoral context unlikely to meaningfully change the dynamics.

Construction

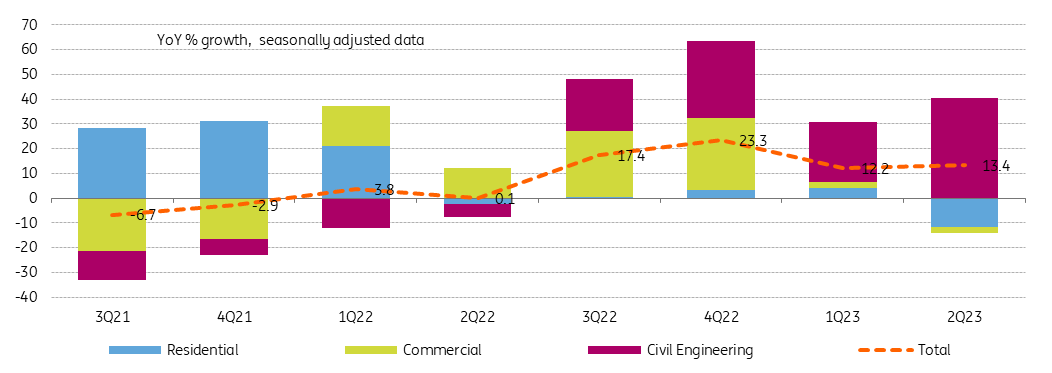

The construction sector performed strongly during the second half of last year and has continued to surprise positively this year too, with annual growth rates of 12.2% and 13.4% in the first and second quarters, respectively. That said, the key difference compared to last year is in the sectoral distribution of these strong growth rates. Specifically, had it not been for this year’s significant positive contribution of civil engineering projects, construction output would have likely followed the current contractionary path of residential and commercial projects.

Construction by main groups

Looking ahead, the lagged impact of monetary tightening continues to feed through the economy, hence we believe that EU-funded civil engineering projects, i.e. public infrastructure investments, will remain the key growth driver. This could more than offset the weak performance of commercial and residential projects for the rest of this year and next.

Services

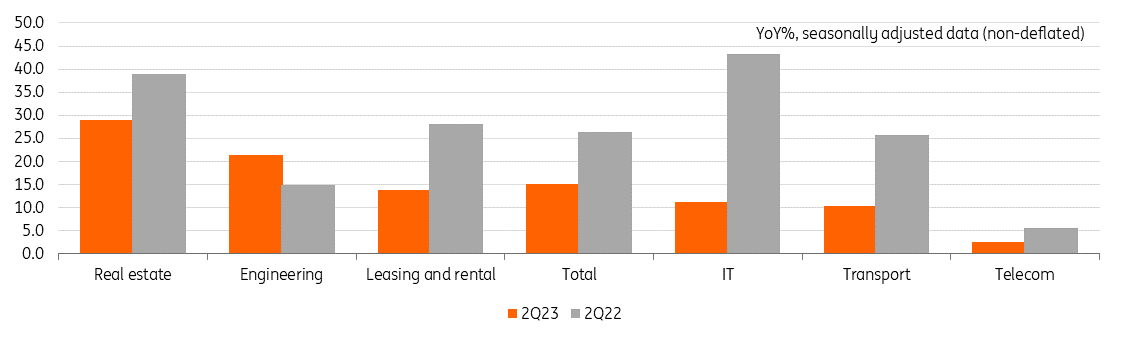

While slowing sharply since the beginning of the year due to base effects, the growth rate of the services for companies’ output is now broadly back to its pre-pandemic trend.

Consistent with the trend in construction, the resilience in momentum was driven by engineering-related services, with the most likely deliverables including the likes of feasibility studies and impact assessments. As such, all the other subsectors experienced growth slowdowns, with the IT and transport sectors losing the most momentum in annual terms in 2Q23.

Services rendered to companies

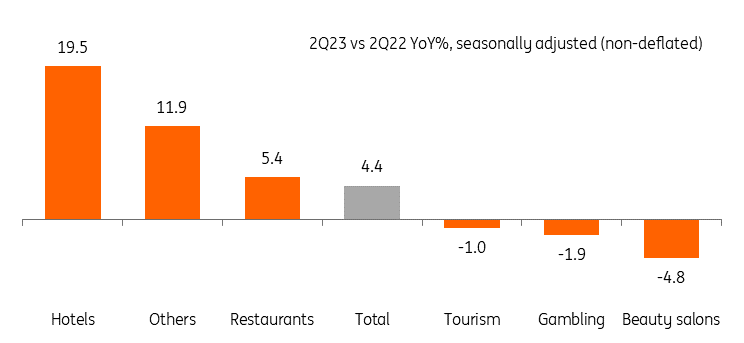

When it comes to the services provided to the population, all subsectors slowed in the first half of 2023. That said, the HoReCa (hotel / restaurant / catering) industry still experienced a strong annual growth rate of 17.1% in the first half of the year, slowing the least. On the other hand, during the same period, growth rates of beauty salons and gambling activities, useful proxies of some discretionary spending habits, remained the weakest.

Services for the population

Looking ahead, we believe that overall momentum in the services sector will continue to weaken. So far, the key reason has been related to the abovementioned slowdown in demand. Downside risks come as well from a higher fiscal burden on companies, potentially resulting in a hit to both growth and the disinflation trajectory.

Our conviction is that services growth will slow even more, most likely hitting a bottom in the lower single-digit area. Additional risks also come from a possible higher-from-longer rates scenario. All in all, we think that neither rising wages nor the resilience of order books will prove to be enough to offset these downward pressures.

Trade balance and the current account

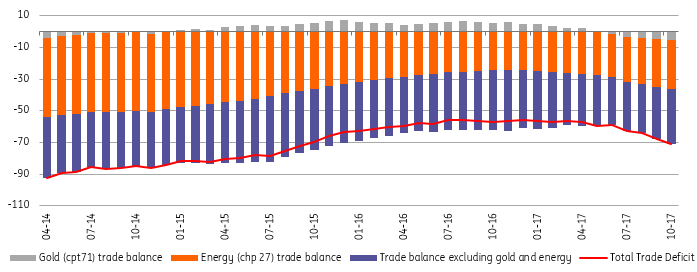

During the first seven months of 2023, the trade balance posted a €15.6bn deficit, 17% narrower than in the same period of last year. The improvements were broad-based; with the exception of food items, all the other categories posted lower deficits than in the same period of 2022. This is likely driven by the general economic growth slowdown and by better terms of trade, especially in the commodities sector.

Overall, this led to a reduction in the trade balance deficit as a percentage of GDP to -4.9% after seven months of 2023, versus -6.6% in the same period of 2022. That said, a sharp industrial activity downturn is currently taking place in Germany which will weigh on Romanian exports in the second half of the year and likely beyond, impacting the balance negatively.

Trade balance by main groups

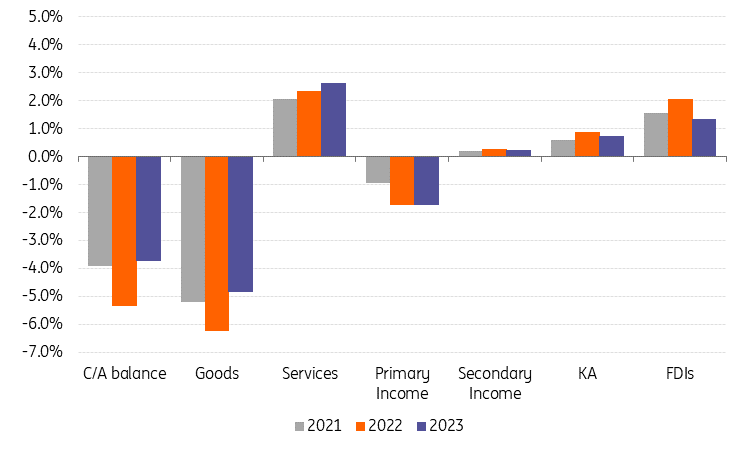

On the current account side, we see mixed trends in 2023, but overall, we think that the full-year deficit will shrink to around -7.5% of GDP, from -9.3% of GDP in 2022. The recent rise in oil prices – which we expect to linger – could offset the better terms of trade, although they are unlikely to change the picture for this year.

Moreover, a stronger surplus on the services side will contribute positively. That said, a failure to reduce the public deficit to sustainable levels will delay the long-expected current account improvement.

Balance of payments by main categories (Jan-Jul each year, % of GDP)

Budget deficit

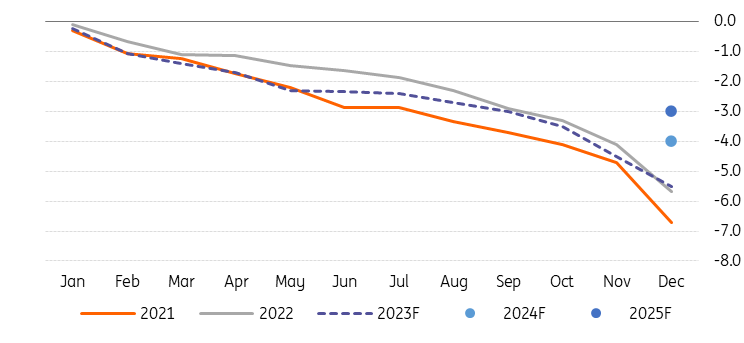

The multi-annual effort to bring back the budget deficit to below 3.0% of GDP has faltered even before touching 2023’s target of 4.4% of GDP, which earlier in the year seemed within reach. A combination of slower GDP growth, below-plan revenues and above-plan expenditures is never a good thing, and since the middle of the year it has become clear that additional measures are needed. At the time of writing, a legislative draft has been published which encompasses various measures on both the expenditures and revenue side, with a strong emphasis on the latter.

On net, the budgetary impact should be around 1.2% of GDP in each of the following two to three years. While at this moment we don’t know the new budget deficit targets, we estimate that in 2023 the budget deficit will be around 5.5% of GDP; it should decline towards the 4.0% area in 2024 and possibly closer to 3.0% of GDP in 2025. However, this is highly contingent on still relatively strong GDP growth numbers. To the extent that the new targets will be agreed with the European Commission (and we believe they will be), it shouldn’t shake the market’s confidence much and/or the flow of EU funds.

Budget gap (% of GDP)

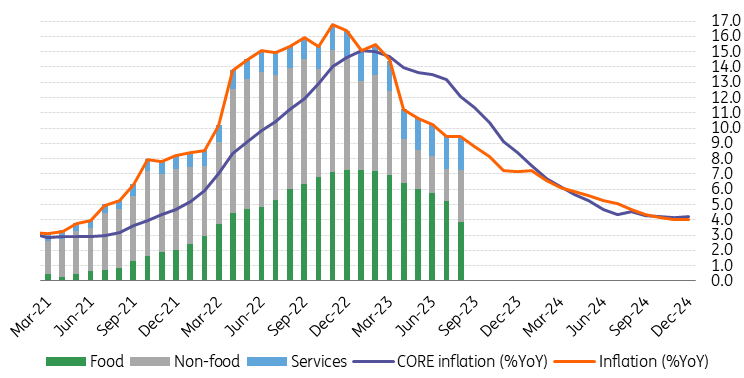

Inflation and the central bank

With price pressures back in single digits as of July, the disinflation path looks set to continue but might suffer slightly. We now see the year-end inflation rate at 7.1% (versus our old 6.9% estimate). For end-2024, we expect price pressures to decline to 4.0%, although the intra-year profile could be higher than previously estimated.

So far this year, key downward contributions have come from lower overall commodities prices versus last year and the recent caps on basic food markups. In August, an unusually large upside surprise came from drug prices, which increased by 20% month-on-month, offsetting the gains from lower food prices and somewhat derailing the disinflation path.

Inflation (YoY%) and components (ppt)

Looking ahead, we think that slowing aggregate demand and still-high interest rates will continue to weigh on demand and price pressures. That said, strong wage growth, the upcoming 10% minimum wage hike in October, significantly higher oil prices, as well as the impact of the recent fiscal package, are likely to slow the disinflationary path and they add upside risks to our projections in both the short and medium terms. These risks are particularly relevant for our 2024 outlook given that the bulk of the fiscal measures are due to be enforced starting 1 January 2024. On balance, despite the upside risks for 2024, we still think that our current projection of 4.0% for the end of 2024 is attainable.

From a monetary policy perspective, we don't believe there will be any rate cuts this year. The start of the easing cycle should come in the first quarter of next year, with a total of 150bp cuts by year-end. This might be done alongside the gradual restriction on liquidity conditions in the interbank market, as the current surplus is likely not giving a lot of comfort to the National Bank of Romania (NBR).

Should the disinflation path disappoint, the probability of a higher-for-longer rates scenario increases materially. If this becomes next year’s reality and the NBR does not ease policy, by the end of the first half of 2024 the economy will have had two years with the highest interbank rates since the aftermath of the Global Financial Crisis. As such, the pressure on the aggregate demand could deter GDP growth even beyond what we currently estimate.

Ratings

We remain of the opinion that Romania will maintain its investment grade for the foreseeable future. In fact, the direction of travel has started to feel slightly opposite, with the relatively strong growth and the Excessive Deficit Procedure (EDP) anchor creating some mild positive perspectives for Romania’s rating. This has faded somewhat as the fiscal consolidation story did not go as initially planned.

The government, nevertheless, looks committed to adopting measures containing the budget deficit and (importantly) agreeing with the EU on the new budget deficit trajectory. We believe that the EU/EDP anchor will continue to provide confidence to markets and agencies that the EU funds are not at risk, though inherent delays might occur.

Rating drivers

FX and markets

Over the summer, the Romanian leu moved towards the upper end of the NBR tolerance band and it is hard to see a reason for the EUR/RON to move much lower. We estimate that the current playing field in the EUR/RON range is 4.94-4.98. We assume that it is more comfortable for the NBR to have pressure on a weaker RON and withdraw some liquidity out of the market. The latter still remains near record surpluses, which is reflected in the fall in market rates well below the policy rate. Should we see further negative surprises in inflation, we can expect more central bank activity in the FX market as a first line of defence.

Looking ahead, in the current situation, it is hard to read when the central bank will allow further upward movement. The chance of crossing the "magical" EUR/RON 5.00 threshold this year is shrinking considerably and will probably be on the table later next year, given tackling inflation is still the bigger priority.

The picture for Romanian government bonds (ROMGBs) has blurred a bit as we expected but we still see good value here. The government recently unveiled the supposedly final version of the government measures and indicated the size of the adjusted government budget deficit. According to our estimates, this should lead to an additional increase in borrowing needs of around RON17bn from the original RON160bn. This itself is not a small number, but given the massive frontloading of ROMGBs issuance in previous months (roughly 90% of the original plan covered) and the recent FX issuance, we expect the market to accommodate the remaining issuance without much trouble.

Thus, overall, coupled with the possible delay of EU money and the upcoming elections, the risk balance of ROMGBs has deteriorated, but they are still one of our favourites within the CEE region. From a valuation perspective, the 10y spread against Polish government bonds (POLGBs) is again well above 100bp and the spread against Hungarian government bonds (HGBs) has reached zero for the first time since the beginning of this year. Both indicate tempting levels of ROMGBs offsetting risks along the way.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more