- Quick take

- 21 May 2026

- Hungary

Hungary records robust wage growth in March, but the good times may be short-lived

As expected, March's wage data revealed a strong increase in Hungary. As inflation remains low, real wage growth is high. However, if the economic turnaround is not sustainable, companies will adapt to the pressure sooner rather than later

| 9.2% |

Average wage growth (March)ING Forecast 9.0% / Previous 9.7% |

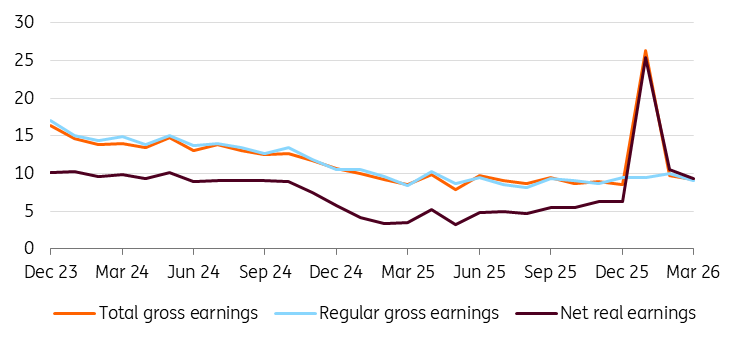

The latest wage statistics from the Hungarian Central Statistical Office (HCSO) paint a positive picture of wage trends. The data show a year-on-year increase of 9.2% in the average gross wage in March 2026. Although this represents a slight slowdown compared to the previous month, the figures are in line with market consensus and indicate strong dynamics. Net earnings continued to grow at a rate exceeding 11%. The disparity between gross and net wage growth can be attributed to changes in family tax allowance and personal income tax exemptions for mothers applying from this year.

Nominal and real wage growth (% YoY)

Perhaps even more important than the average wage is the change in the median wage. Here, we continue to see an annual increase of 10.7%, which is almost identical to the rise in the minimum wage. This clearly indicates that the increase in the minimum wage has caused compression of wages in the middle three income quintiles, a situation that companies have been trying to manage. This is why the March wage statistics are important, and why the April figures will be important too, because most multinational companies decide on wage changes during the spring. Based on what we have seen so far, it appears that these large companies have ultimately opted for significant wage increases too.

Examining the increase in the purchasing power of the average wage reveals that the year-on-year change in real earnings has remained high, exceeding 9%, due to persistently low inflation and robust wage growth. Households' disposable income is therefore expanding significantly, as evidenced by retail sales data, and this is likely to be reflected in the first-quarter GDP figures in the form of a more substantial increase in consumption.

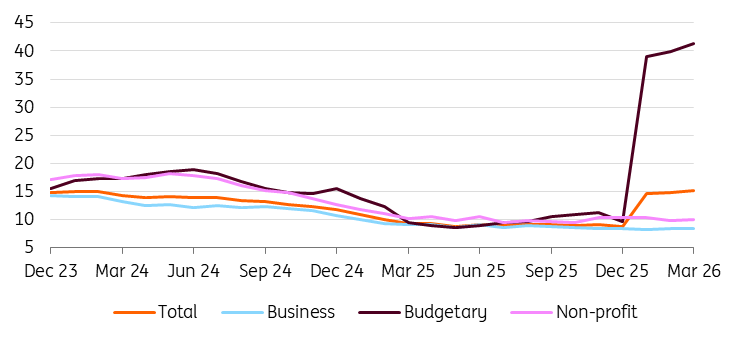

Looking into the underlying trends, we observe a slight slowdown in the pace of wage growth across all major sectors in March compared to the previous month. However, wage growth remains robust. Above-average wage growth was observed in agriculture in the private sector, likely due to increased labour demand linked to the spring planting season. Average wage growth in the energy sector has also accelerated significantly. However, wage growth in the manufacturing sector has slowed. The average wage increase is generally strong in certain service sector areas, except for human health and social work.

Wage dynamics (3-month moving average, % YoY)

The 11% and 7% increases in the minimum wage and guaranteed minimum wage, which were implemented in January, are clearly having a significant impact on this year's annual wage dynamics. This is reinforced by the fact that companies currently engaged in the spring wage-setting cycle have adjusted their policies accordingly. Wage trends continue to be significantly influenced by the fact that many companies are hoarding some workforce, while demographic trends are putting structural pressure on the supply side of the labour market, even in the short term.

The latest March data did not alter our overall outlook, so we anticipate annual average wage growth of approximately 9-10% for all of 2026. The biggest question is how companies will act amid cost shocks caused by the war in the Middle East, more persistent labour cost increases, and external downside risks to economic growth. The business confidence index surged dramatically after the elections, which could temporarily protect against layoffs as companies may choose to wait and see in the hope that the new economic policies will boost the economy. However, external risks are intensifying as we approach a point at which physical shortages of energy sources and certain raw materials become a reality. Consequently, it is increasingly likely that companies will respond to this shock by significantly reducing their workforce.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more