- Quick take

Hungarian inflation falls on food deflation

- 7 July 2023

- Hungary

The rapid deterioration in corporate pricing power is being reflected in lower inflation readings, which are also being supported by base effects. However, despite the positive outcome, the central bank’s normalisation of policy is now focused solely on market stability

| 20.1% |

Headline inflation (YoY)ING estimate 19.9% / Previous 21.5% |

| Higher than expected | |

Food prices drop for the first time since mid-2021

As expected, the disinflationary process continued in June as headline inflation retreated to 20.1% year-on-year (YoY). In addition to base effects, this was the result of a 0.3% month-on-month (MoM) increase in prices, which shows that inflationary pressures have not fully dissipated. In this regard, it is worth noting that the pace of the monthly price change is still stronger than the historical June repricing, which has typically been around only 0.1%.

What is certainly welcome news, however, is that the structure of inflation has improved. Core inflation fell to 20.8% YoY, which is 2ppt lower than the May figure. In terms of monthly dynamics, core inflation rose by just 0.3%, which is the lowest monthly reading since September 2021.

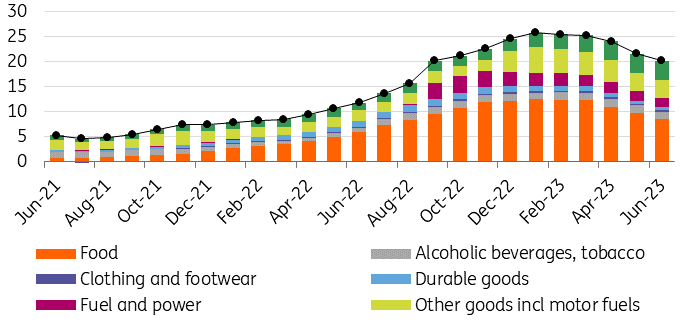

Main drivers of the change in headline CPI (%)

The details

- Food inflation continued to moderate for a sixth consecutive month, as the annualised index retreated to 29.3% YoY. The monthly reading is also promising, as food prices fell by 0.4% between June and May, reflecting price changes in both unprocessed and processed food items. The monthly deflation in food prices is a welcome development, as it has not been seen since June 2021.

- The global disinflationary trend, combined with a stable forint (in June) helped to lower the price of consumer durable goods. With the heating season officially over, households’ average energy bill fell by 2.1% MoM, which contributed to the retreat in headline inflation.

- The rise in global energy prices in June was reflected in motor fuel prices in Hungary, hence the 2.1% month-on-month increase for this component. In this regard, headline inflation fell less than core inflation, as the latter was not affected by the rise in motor fuel prices.

- The moderation in inflation was somewhat offset by the continued rise in services prices, where the annual rate rose further to 14.4% YoY. This was the result of a 0.9% MoM increase in prices, which was mainly dominated by repricing in recreational services.

The composition of headline inflation (ppt)

Underlying price pressure eases as well

The deceleration in headline inflation in June was mainly driven by core factors, among which the sharp monthly-based drop in food prices stands out. Within this, the fall in processed food prices was the main factor, hence the more pronounced deceleration in core inflation. The slump in food sales, as pointed out in our latest piece, is clearly helping to contain inflationary pressures, as competition increases between retail outlets for the overall shrinking disposable income of households.

This, combined with base effects helped core inflation to retreat to 20.8%, shaving off 2ppt compared to the May figure. Other underlying indicators – like declining sticky price inflation – are also showing promising signs that Hungary's inflation problem is gradually improving.

Headline and underlying inflation measures (% YoY)

Single-digit inflation is achievable by November

We expect both headline and core inflation to continue to retreat in the coming months. In light of today’s data, single-digit inflation at the end of the year seems certain. What’s more, if there are no further price shocks, we could even see an inflation print below 10% as early as November. Our 2023 full-year average inflation forecast remains unchanged for the moment, which is expected to be close to 18%.

At the same time, the risk of a persistently high inflation environment has not yet been averted. The very dynamic wage outflows could translate into positive real wage growth in the last quarter of the year, even as early as September. A combination of companies’ typically-retrospective pricing behaviour in Hungary (carrying out price increases based on past inflation releases) and the rise in real wages could trigger further repricing.

On the other hand, we assign less probability to a renewed boom in consumption at the end of the year as households’ savings have been significantly drained in recent months to offset sky-high inflation. Therefore, we believe that positive real wage growth in the fourth quarter will push households to replenish their depleted savings, which in turn might have negative effects on growth prospects and on the repricing power of corporates.

Market stability remains the key driver for monetary policy

In our view, the June inflation release is unlikely to have a significant impact on monetary policy. Given that the central bank still distinguishes between market and price stability and that the current easing cycle is basically a function of market stability, the more important question is to what extent the weakening forint will rewrite the central bank's view. If the forint stabilises around the 380-385 level and does not weaken further, we see no significant obstacle to another 100bp rate cut in July, in line with current market pricing. However, should we see further underperformance of the forint versus its CEE peers, we wouldn’t rule out some hawkish verbal intervention by the National Bank of Hungary. This may be a reminder that the interest rate easing cycle is not carved in stone and in the event of market instability, which may jeopardise the inflation outlook, the central bank is ready to step on the brakes in its normalisation process.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more