- Quick take

- 6 July 2023

- Hungary

Hungary’s retail sales and industrial output continue to plunge

With domestic demand severely constrained, both the retail sector and Hungarian industry are struggling, and we don’t see a path for a swift recovery

There is nothing surprising in the latest data release from the Hungarian Central Statistical Office (HCSO). As we predicted in our latest Monitoring Hungary report, the drop in real wages has been constraining both household consumption and domestic demand towards goods. Now the latest economic activity figures for May confirm this, as the volume of retail sales dropped by 12.3% year-on-year (YoY), while industry registered a 4.6% YoY plunge in the volume of production (both working-day adjusted data).

As both sectors continue to struggle with weak domestic demand, the fate of GDP growth in the second quarter hinges vastly on the outperformance of agriculture.

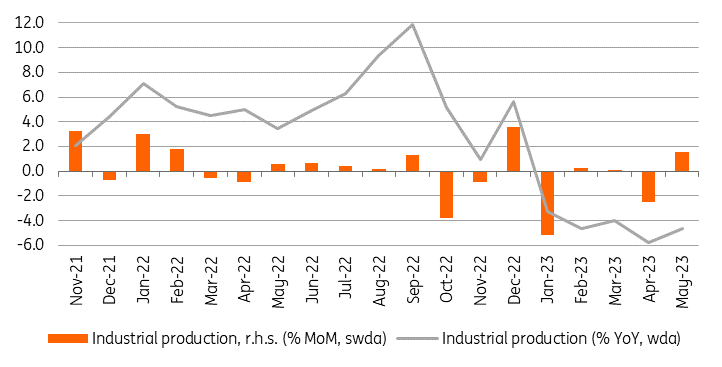

Industry continues to face opposing forces

| -4.6% |

Industrial production (YoY, wda)ING estimate: -6.5% / Previous: -5.8% |

| Better than expected | |

Hungary's industry continued to underperform in May, as the volume of industrial production fell by 4.6% YoY, after adjusting for calendar effects. The yearly based drop is the result of a 1.6% month-on-month increase in the volume of industrial production, after adjusting for seasonal and calendar effects. However, the rebound in May was not significant enough to break the sector's negative trend, as output is still below the level recorded at the beginning of the year.

Performance of Hungarian industry

Even though the Statistical Office will release the detailed data next week (13 July), the preliminary statement highlights that the majority of the manufacturing subsectors contributed to the production decline. As always, the exceptions are electrical equipment and transport equipment manufacturing (e.g. electric vehicle batteries and cars). Both sectors expanded on a yearly basis in May. In contrast, the other two most important sectors: computer electronics and food manufacturing recorded declines in production, according to the Statistical Office’s commentary.

In this regard, only manufacturers related to the automotive industry are able to breathe any kind of life into Hungarian industry. At the same time, this confirms the picture of steadily shrinking domestic demand in the economy, which is also reflected in the latest retail sales data. The picture is therefore very clear: export sales are essentially able to compensate to some extent for the very weak performance of companies producing for the domestic market.

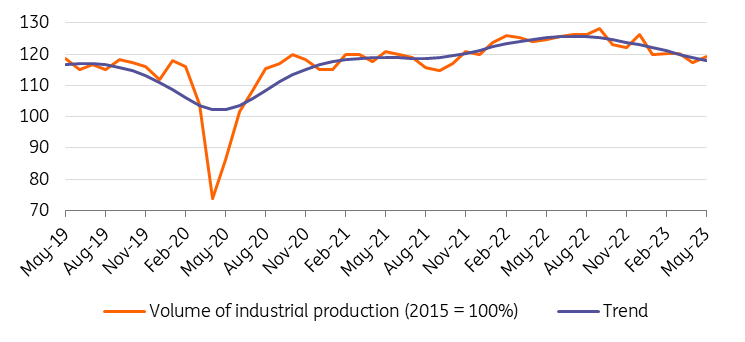

Volume of industrial production

Going forward, we expect this dichotomy to persist. In this regard, order books show a similar picture, as export order books are holding up, while domestic order books have collapsed. The big question remains, how long can the export momentum last given that recent PMIs and other surveys across the globe suggest that manufacturing activity is weakening again and that order books are shrinking worldwide?

The expected positive impact of the reopening of China has largely failed to materialise, and the high global interest rate environment is increasingly dampening domestic demand in the developed world. These dynamics have a clear negative impact on both the current situation and the outlook for Hungarian industry.

Despite today’s positive surprise, we still expect industrial production to be negative for the year as a whole. Therefore, we believe that agriculture could remain the sole saviour of economic growth in 2023, as the latest industry data do not seem to indicate a turnaround in domestic demand.

Retail sales plunge in parallel with deteriorating purchasing power

| -12.3% |

Volume of retail sales (YoY, wda)ING estimate: -11.5% / Previous: -12.6% |

| Worse than expected | |

On a monthly basis, the volume of retail sales has been falling steadily since the end of last year, with March being the exception. The latest data from May confirm the downtrend as volume in retail shops fell by 0.8% MoM, adjusted for seasonal and calendar effects. The monthly drop reveals the fact that the pleasing improvement regarding the annualised index (-12.3%) is mainly due to base effects. Thus, there is little reason for joy as short-term dynamics do not point to a rebound in sales volume.

Looking at the breakdown, only food sales performed relatively well in May, as sales increased by 0.1% MoM. From a trend perspective, however, this is not particularly good news, as it is only the third time in the last 12 months that food sales have risen, two of which were just 0.1% increases. Nevertheless, with annualised food inflation still at a very high level of 33.5%, it is understandable that households are still cutting back on food spending. Given that real wages have been falling steadily for eight months, we do not expect to see a significant recovery in food retailing in the second quarter, despite the easing of food price pressures.

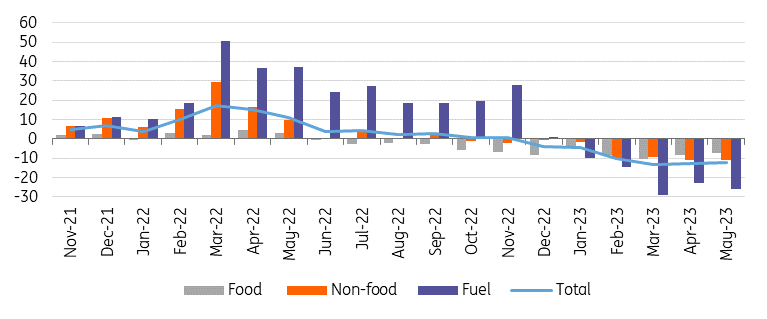

Breakdown of retail sales (% YoY, wda)

In contrast with the food segment, non-food retailing dropped on a monthly basis, displaying a 0.3% retreat in the volume of sales. As for the detailed shop-based breakdown, the story remains largely unchanged compared to the previous months. Those sub-sectors that continue to perform very poorly typically sell the products on which households are most willing to save, i.e. clothing, furniture, computer equipment and manufactured goods. The remarkable 22.1% YoY fall in the latter’s volume highlights the lack of domestic demand that Hungarian industry has been suffering from.

Another aspect that also reflects the deterioration in household purchasing power comes from the data on fuel retailing. Fuel prices fell in May, as reflected in the May inflation print, where motor fuel prices fell by 6.6% on a monthly basis. However, this time households were inattentive to price elasticity (lower prices lead to increased demand), as fuel retailing dropped by 1.5% MoM. Over the past two decades, the last time such an event occurred, the economy either struggled with deflation (2015) or was in lockdown (2020). By event, we mean when fuel prices fell by more than 5% while the volume of fuel sales fell by at least 1% in the same month.

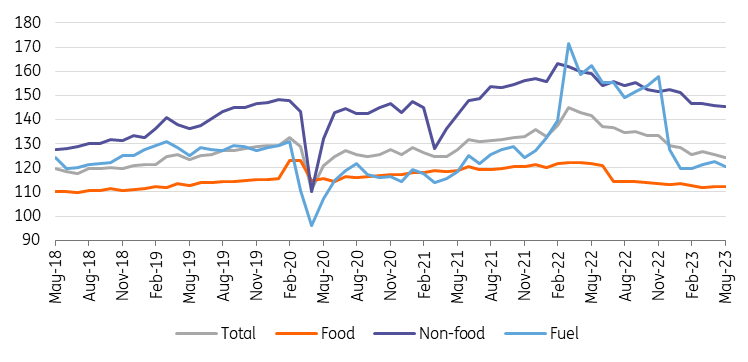

Retail sales volume in detail (2015 = 100%)

Judging by the latest retail and industrial data, we believe that the performance of these two sectors will be very weak in the second quarter and that there is little prospect of any meaningful improvement in these two areas in the coming months. The biggest challenge to a significant turnaround remains the continued erosion of household purchasing power, which has been falling steadily for eight months. Recently-introduced mandatory sales promotions may provide some stimulus to food sales, but no real impetus is expected for non-food and fuel retailing as non-essential spending continues to be cut back.

As a result, we expect consumption to fall sharply in the second quarter and for the year as a whole. By contrast, agricultural production could be very positive, partly due to the favourable weather so far and partly due to last year's extremely low base. This could be just enough to pull the Hungarian economy out of a technical recession in the second quarter, offsetting the weak performance of industry and retail trade.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more