- Quick take

- 9 February 2024

- Hungary

Hungarian inflation back in the central bank’s tolerance band

January's inflation data surprised on the downside, with the headline figure falling below the upper limit of the central bank's tolerance band. However, it would be premature to declare victory as we expect inflation to reaccelerate

| 3.8% |

Headline inflation (YoY)ING estimate 3.7% / Previous 5.5% |

| Higher than expected | |

This is the last month when exceptionally high base effects helped

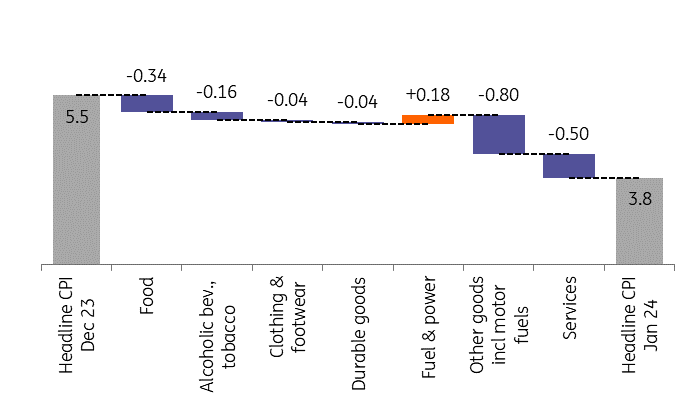

Inflation in Hungary continued to fall in January, with the Hungarian Central Statistical Office (HCSO) reporting a much lower inflation rate than the market consensus and closer to our own estimate. Compared with December, headline inflation fell by 1.7ppt to 3.8% year-on-year. As a result, headline inflation fell within the National Bank of Hungary's (NBH) tolerance band for the first time since March 2021.

This time, unlike in previous months, the continued disinflation was essentially due to favourable base effects, as the monthly repricing was 0.7%. At the same time, core inflation rose by 0.4% month-on-month (MoM), suggesting that price pressures were lower among the items included in the core basket.

Main drivers of the change in headline CPI (%)

The details

- Even though food prices rose by 1.2% MoM – the highest across all components – last year’s high base brought the annual food inflation rate to 3.6%. On a monthly basis, unprocessed food prices increased more than processed food prices, mirroring the monthly dynamics of headline and core inflation.

- Fuel prices dropped by 0.5% MoM, which was very surprising to us. In January, fuel prices were raised in two steps, by a total of 41 forints due to the pre-announced increase in excise duties, therefore we expected an increase in this regard.

- Prices of durable goods rose by 0.5% MoM in January, which is surprising given the easing of external inflation and relatively stable EUR/HUF. In addition, prices of fuel and power have likewise increased by 0.9% MoM, which basically can be regarded as household energy.

- Services prices rose by 0.5% MoM, which is lower than the usual start-of-the-year repricing. However, this also shows that the high services price adjustment in December was, in fact, a good part of the price adjustment at the beginning of the year brought forward by the early minimum wage increase. Looking at the two months together, the combined repricing is slightly higher than the usual one.

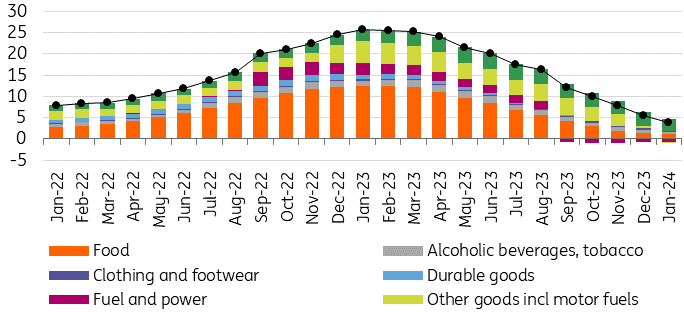

The composition of headline inflation (ppt)

Core inflation keeps moving in the right direction for now

Core inflation decelerated by 1.5ppt to 6.1% YoY in January, while the NBH's measure of inflation for sticky prices also decreased, displaying a reading of 7.7% YoY. However, the 0.4% MoM increase in core inflation is still relatively high by historic standards, suggesting that the year-on-year deceleration is largely due to base effects. Price pressures in the services sector are certainly an area we'll be watching closely, especially as we expect backwards-looking price adjustments in February and March in the insurance, banking, and telecom services sectors, which could mean double-digit price increases again in these areas.

Headline and underlying inflation measures (% YoY)

In our view, it is premature to declare victory over inflation

All in all, we have rather mixed feelings about the January inflation figure, as it does raise a number of questions including whether the excise duty hike on fuel prices has been considered. Against this backdrop, in our view, the 0.7% MoM increase in headline inflation at the beginning of the year is already a cause for concern. Bearing in mind that in the peacetime period (2016-2020), before the inflation shock of recent years, the average January repricing for the entire consumer basket was 0.4%.

In any case, headline inflation has already fallen below the upper limit of the central bank’s tolerance band, i.e. below 4%. However, it would be very premature to declare victory, as favourable base effects have essentially run their course. As a result, we expect inflation to stabilise (or ease slightly) in the coming months and to pick up again, especially in the second half of the year. While inflation is likely to average below 4% in the first half, it could be around 5% in the second half of 2024 and around 5.5-6.0% at the end of the year.

Forint momentum might urge the central bank to remain cautious

While favourable inflation developments could pave the way for the central bank to cut interest rates at a faster pace, the situation is not nearly as simple as it first appears. Both market and political pressure on the central bank may intensify, which could ultimately lead to a further weakening of the forint in the coming weeks. This implies further inflation risks, which the central bank will have to consider. In the end, there may be no room for a rate cut of more than 75 basis points.

The correlation between retail price expectations and core inflation

Moreover, the latest retail price expectations suggest that underlying dynamics of repricing could continue at a relatively strong pace in early 2024. Finally, the crisis over the Red Sea hasn’t been resolved, while political risks that are weighing on financial markets and that led the NBH to adopt a more cautious stance in January remain. So, looking at the big picture, we believe that all factors other than the headline inflation indicator would tend to warrant caution and we currently believe that the NBH may stick to its 75bp rate-cut pace in the coming months.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more