Turkey sees a modest improvement in its current account deficit

Turkey's current account deficit last year improved on 2022 levels. And with a lower-than-expected December number and an improvement in external imbalances, preliminary trade data implies further narrowing in January

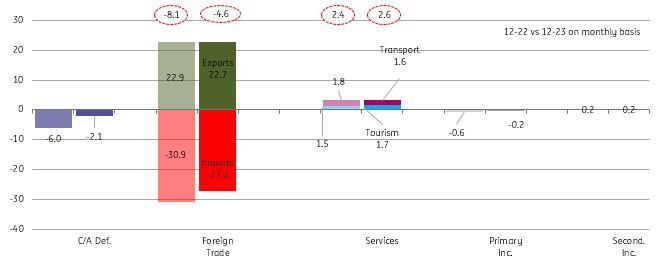

Turkey's December current account posted a deficit of US$2.1bn, significantly lower in comparison to the market consensus of US$3.3bn and our call at US$3.2bn. It comes on the back of higher services and primary income. The breakdown of monthly data shows that improvement in trade balances stemming from energy and gold was the major driver of the decline, along with a small amount of narrowing core trade surplus.

Breakdown of current account (monthly, US$bn)

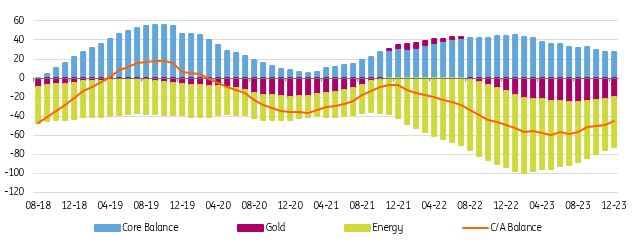

The 12M rolling current account (C/A) balance showed a modest improvement last year on the back of a wider goods deficit with i) declining energy bills (from US$80.1bn to US$52.7bn) and ii) some recovery in services income thanks to stronger tourism. However, a swing in gold imports to a large deficit and a turn to surplus in core deficit (excluding gold and energy) limited the extent of improvement in the current account. Accordingly, the figure showed a $45.2bn deficit (translating into c.4.3% of GDP) at the end of 2023 vs U$49.1bn in 2022.

Current account (12M rolling, US$bn)

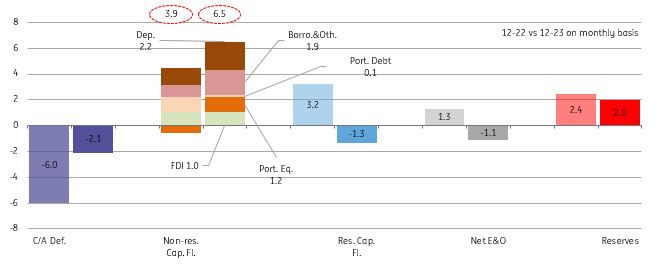

On the capital account, net identified flows turned modestly with US$5.2bn inflows. Errors and omissions outflows that returned in September were at US$1.1bn in December. Despite the monthly C/A deficit and large outflows via net errors & omissions, official reserves recorded a $2.0bn increase thanks to the relatively better shape of the capital account in recent months.

In the breakdown of monthly data, inflows were driven by non-residents’ movements. These items were:

- US$1.3bn trade credits

- US$0.7bn net borrowing by corporates. Accordingly, rollover rates for banks and corporates stood at 101% and 134% in December (vs 115% and 100% in 2023), respectively.

- US$2.2bn deposits placed by non-residents to the local banking system

- US$1.2bn equity purchases of foreign investors

- US$1.0bn inward FDI.

Breakdown of financing (monthly, US$bn)

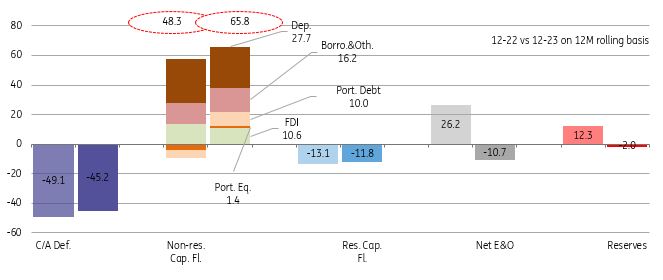

For the whole 2023, despite higher inflows at US$53.8bn vs US$35.2bn in 2022) and large reserve accumulation after the elections, official reserves actually declined by US$2.0bn. This was driven not only by the large C/A deficit but also by US$10.7bn outflows via net errors & omissions (vs large US$26.2bn inflows in 2022 at US$36.9bn). These numbers show a challenging picture for external financing, though the outlook has significantly improved since the elections, with the policy framework turning increasingly supportive of capital inflows.

Breakdown of financing (annual, US$bn)

Overall, after the peak in July on the back of domestic demand pushing imports significantly upwards and a deterioration in the gold trade balance, the current account has adopted an improving trend. According to the provisional customs data released by the Ministry of Trade, the foreign trade deficit dropped by 56.8% to US$6.2bn in January from the record high level in the same month of the previous year. The data implies a sharp recovery in the January current account, given a large deficit in the same month of last year at US$10.5bn while providing support to the conjecture that the impact of the current policy framework on the external balances is getting stronger. Accordingly, the trend will likely continue in the period ahead with ongoing tightening in financial conditions, and hence a visible deceleration in growth.

Regarding the capital account on the other hand, given the policymakers’ priority to replenish reserves and higher external financing needs require continuation of the strength in capital inflows.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap