Hungarian industry runs on exports alone

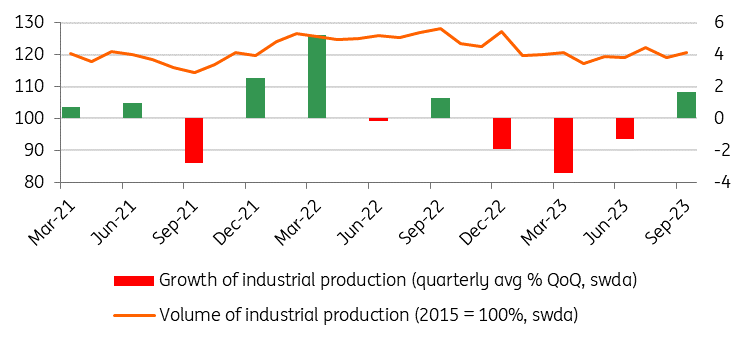

Although September brought some recovery in Hungarian industry, domestic demand is still limiting the overall performance. The silver lining is that the third quarter was good enough to take Hungary out of technical recession

| -5.8% |

Industrial production (YoY, wda)ING estimate: -6.7% / Previous: -6.1% |

| Better than expected | |

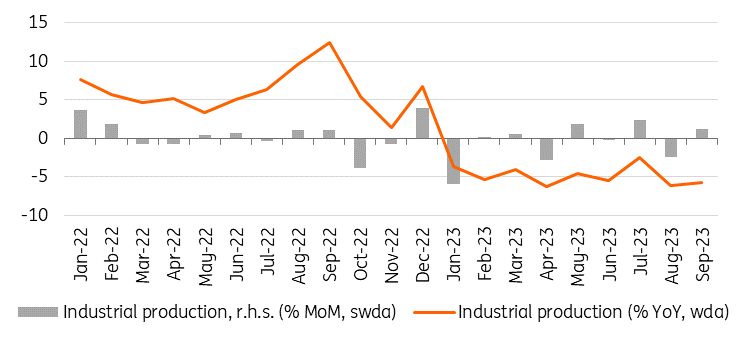

Industry surprised on the upside in September, with output rising by 1.2% month-on-month, according to the latest release from the Hungarian Central Statistical Office. This also means that, contrary to the expected deterioration, the year-on-year index for the working day adjusted indicator improved in September compared with August. Although the change in September can be seen as a positive development, the overall picture remains unimpressive, with production levels failing to reach the levels seen in July. Moreover, the level of industrial production is still hovering around the levels seen after the recovery from the Covid crisis.

Volume of industrial production

With the September data, we now have the performance for the third quarter as a whole as well. Our estimates show that industry grew by around 1.7% on a quarterly basis, meaning that the sector could have made a positive contribution to GDP growth in the third quarter. This raises the possibility that, after four quarters, we may see a positive quarter-on-quarter change in GDP, i.e. an end to the technical recession in Hungary.

Production level and quarterly performance of industry

Detailed data is yet to be released, but according to preliminary data from the Hungarian Central Statistical Office (KSH), there were no significant changes in the structure of industrial production. While the majority of sub-sectors contributed to the decline in output, the exceptions remain the manufacture of EV batteries and the car industry. The improved performance in September was thus due to export sectors returning to full capacity after the summer shutdowns. Moreover, the data suggests that the technical problem experienced by Volkswagen at the end of September did not lead to a production shortfall that would have dragged down the industry's performance.

Performance of Hungarian industry

In our view, as long as there is no lasting change in the economic environment, industrial production will hover around the levels of 2021-2022. This also means that we can expect industrial production to contract by around 5% for the year as a whole.

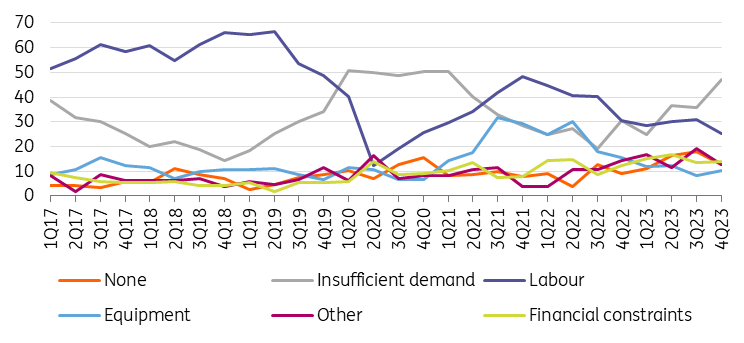

In terms of risks regarding the outlook, there have been no significant changes over the past month. The clouds are gathering on the external demand side, i.e. on the side of the export-producing sectors, as European industrial performance continues to struggle to find its footing, while growth in China is still weak, which is hardly helping a recovery in world trade. Over the past two months, new orders in the manufacturing sector have contracted, and order books have also weakened. While the level of total orders in June was 10.6% higher on a yearly basis, we see the possibility of it falling into negative territory in September due to the high base. Turning to domestic factors, there are still no signs of a rapid pick-up in output growth in domestic demand (consumption and investment) in the short term.

Factors limiting production in Hungarian industry (% of respondents)

Looking at the end of this year and the outlook for 2024, there are some positives. Industrial companies will be able to renegotiate their energy contracts this winter at a much more favourable market price. This could lead to a significant reduction in their costs, which in turn could lead to a pick-up in production in sectors that are currently underperforming due to sunk costs (mostly sectors driven by domestic demand). This could also be helped by the fact that, as inflation moderates and household purchasing power recovers from the end of the year onwards, industrial sectors producing for the domestic market could receive some positive impetus not only from the supply side but also from the demand side, which could offset the initial weakening of industrial exports.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap