Real rising wages are no cure-all, as the Hungarian retail sector can confirm

The volume of retail sales stagnated in September despite the possible return of positive real wage growth. And that could be an indication of how long the road to normalisation will take

| -7.3% |

Retail sales volume (YoY, wda)ING estimate: -7.8% / Previous: -7.1% |

Retail sales in Hungary aren't getting significantly better. Based on the September figures, retail trade volumes were essentially unchanged, and the Year-on-Year index deteriorated from the previous month. Those figures are on a monthly basis, calculated with seasonally and working day adjusted data. Specifically, sales were 7.3% lower, adjusted for calendar effects, compared with the same period last year.

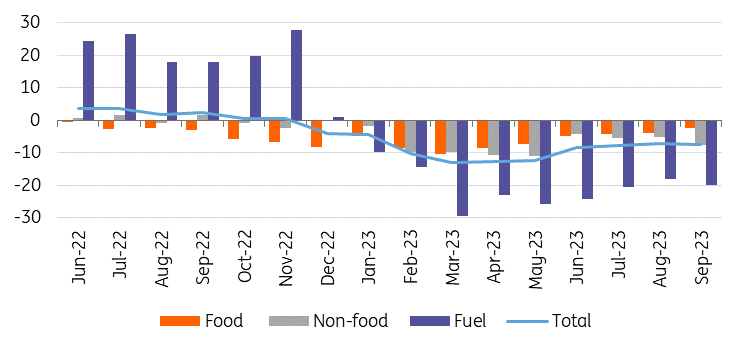

Breakdown of retail sales

% Y-o-Y, Working Day Adjusted.

Looking at the details, there were no major changes in the structure of retail sales. On a monthly basis, the sales volume in food stores increased by 0.1% compared to August, a slightly positive change in the wake of the declines of the previous two months. On an annual basis, however, the relapse remains significant. Despite the moderation in food inflation, price levels are still much higher than a year ago, encouraging consumers to be more cautious in their spending.

Moreover, this segment is the one most likely to be affected by shopping tourism. In other words, the fact that an increasing proportion of the population is choosing to shop abroad (and this is no longer only true for people living close to the country border) will continue to have a significant impact on the domestic performance of food retailing.

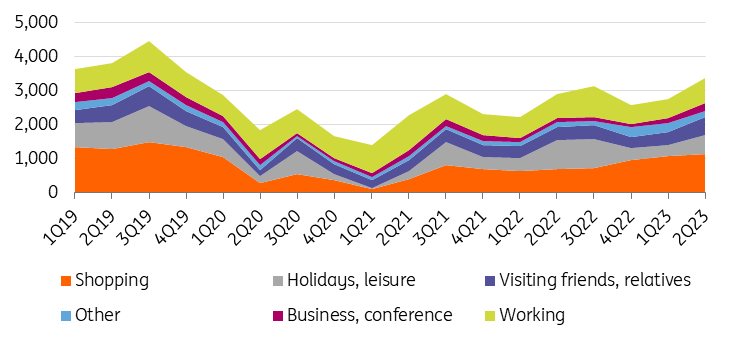

Same-day outbound trips by main motivation of travel

Number of trips in thousands

Sales volume in non-food stores fell by 0.9% month-on-month. September's performance was boosted by the back-to-school season and the resulting increase in sales of books and newspapers (up by 2.7% MoM), while sales in textiles, clothing, and footwear stores fell by a further 5.7% on a monthly basis. Sales volumes also dropped in furniture and electrical goods suppliers by 1.5%, and shops selling manufactured goods were facing a downtrend, too. In a nutshell, households remain very conscious of cutting back on non-essential spending.

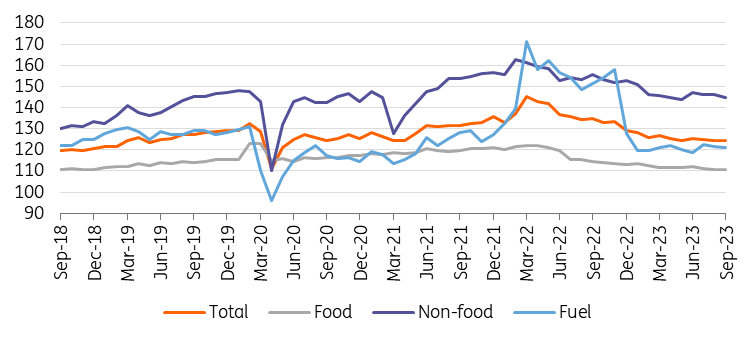

Monthly changes are important, but if we look at the fall in the level of recent sales volume in each of the main sectors on a historical basis, we can see how drastic the changes have been. The current sales volume in food stores is at a level last seen in 2018-2019. Turnover in non-food stores is currently in line with the performance seen in 2020. Fuel sales are matching levels seen around 2020-2021. With the inflationary surge now more than two years old (and it is still with us), the retail sector is in a 'time travel' mode, and the time machine called inflation has taken it back to where we were around four to five years ago.

Retail sales volume in detail

(2015 = 100%)

Our overall conclusion is that none of the main retail sector segments shows any kind of significant improvement, supporting the view of an approaching sustainable recovery. We are still waiting for the September wage growth data, but we can be almost sure that with recent disinflation, real wage growth was back in positive territory. As we've mentioned on several occasions, a mere change in statistical data does not necessarily translate into an immediate turnaround in the real economy.

The retail sector has a very long and painful road ahead to make up for the years lost. Although real wages are expected to rise further in the coming months, this is unlikely to translate into dynamic consumption growth. Households will mainly deleverage and rebuild their reserves before consumption picks up. This is also reflected in the fact that consumer confidence remains at an almost 10-year low. Trust, therefore, needs to recover before the population can start to increase consumption in a meaningful way. As a result, the impact of rising purchasing power on the real economy is not expected to be reflected in retail sales data until 2024, in our view.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap