- Quick take

- 24 September 2020

- France

French business confidence stable despite new Covid restrictions

New measures to fight Covid-19 should have a lasting impact on confidence, slowing 4Q20 growth. Today’s business confidence indicators, albeit improving, also show that the recovery remains fragile

In France, measures have been put in place again to fight the Covid-19 epidemic.

Bars and restaurants will have to close at 10:00 pm, sports facilities will be shut down in major cities where gatherings of more than 10 people are now prohibited. For now, schools remain open and workers are back at work with all the social distancing artillery. We expect these new measures to have a limited direct impact on some sectors, those where the rebound in activity has been the weakest (events, tourism, performing arts, restaurants). As long as schools remain open and people can either go to work safely or work from home, the rebound in activity is not in jeopardy. However, we expect these measures to have a large impact on confidence with consumers getting saving even more in October.

From that perspective, September business confidence indicators published earlier today reflect the fact that these measures, for the time being, are mainly impacting services.

Confidence in the manufacturing industry indeed continued to recover, in line with the uptick shown yesterday in PMI’s (which increased from 49.8 to 50.9). The survey shows that improving order books and lower inventories allow manufacturers to keep planning production, while recent production levels were increasing faster. They still remain cautious when it comes to their own financial situation but overall, confidence is not far from its pre-crisis levels.

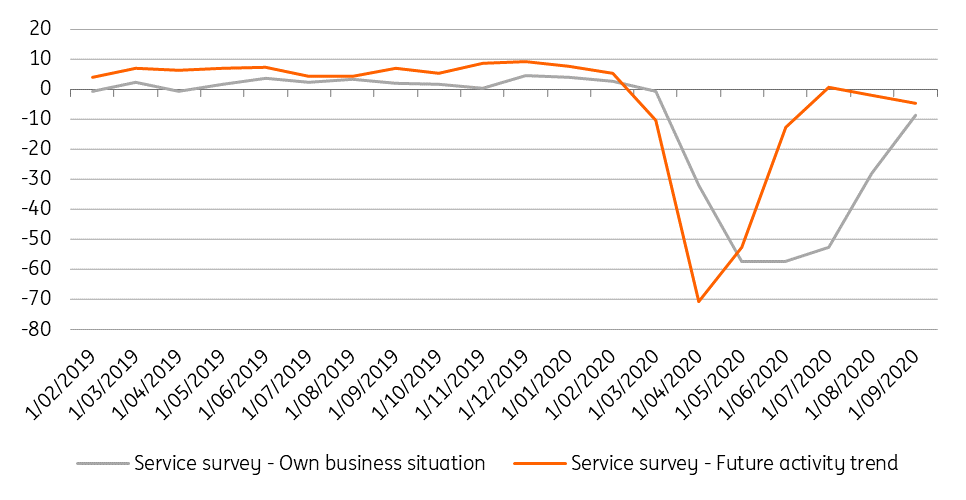

In the service sector, where the rebound in activity was steeper at first, pessimism is back and the recent measures taken to fight the epidemic will not change its course.

Although the survey shows that recent activity has been better and that the business situation has been improving without interruption since May, it also suggests that the wind is turning for the outlook (Figure 1). Likewise, investment intentions remain on the rise, though hiring intentions have deteriorated in September (only temporary work seem to progress).

Overall, service confidence increased in September, but with its most forward-looking components deteriorating (which partly explains yesterday’s bad PMI survey where the service sector component tanked to 47.5). This underlines how cautious companies remain in face of the Covid-19 uncertainties, which the last Government measures are certainly increasing.

Service survey shows mixed feelings about the near future

We do not think that all of this should hamper the strong GDP rebound expected for 3Q20 (+55% QoQ annualized). However, it clearly flags the risk of a much slower dynamic in 4Q20, confirming that the French economy will continue to evolve below 95% of pre-Covid activity levels until at least mid-2021.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more