- Quick take

- 7 July 2025

- Czech Republic

Czech industry likely bottoms out while construction thrives

Annual growth in industrial production gained pace in May when adjusted for the number of working days. A continued pick-up in new orders provides hope that Czech manufacturing is bottoming out. The construction sector is buzzing, with demand for properties remaining robust. Wage gains are still solid, though the pace is a bit softer than before

Industrial production gains solid ground

Czech industrial production rose by 2.2% year-on-year in real terms in May when adjusted for the number of working days, while it was down by 1.6% month-on-month. As in previous months, the annual rate of industrial production in May was partially influenced by the low comparison base in electricity generation. Annual growth was supported by a good performance in other transport equipment, and machinery, where significant long-term contracts were completed.

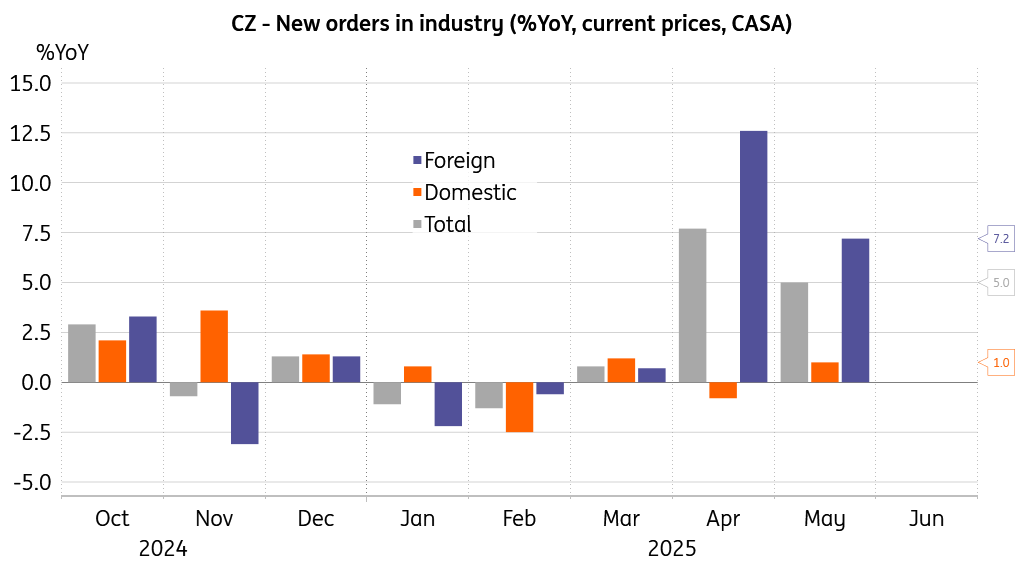

Adjusted series suggests firming manufacturing

The value of new orders in nominal terms rose 5.0% YoY, while on a monthly basis, new orders declined 3.9% in May. Foreign new orders gained 7.2% YoY, and domestic new orders added 1.0% YoY. The annual growth in new orders in May was mainly driven by the motor vehicles section, partially affected by a lower comparison base. New orders performed well on a yearly basis in the fabricated metal products sector. The average number of employees in industry decreased by 2.0% YoY in May 2025, the same pace as in the preceding month. The average nominal wage growth softened to 5.1% YoY in May from 7.5% previously.

New orders provide some hope

Construction: allez, allez, allez!

Construction output gained 11.6% YoY in May and 2.3% MoM. The indicative value of building permits issued dropped by 39.6%. However, this figure comes from a volatile time series. That said, 5.2% fewer dwellings were started compared to the previous year, while completions rose by 4.9%

Such a pace is likely insufficient to balance out the distortions in the residential market, where supply chronically lags behind demand. The average number of employees in construction lost 0.7% YoY in May, and the average nominal wage growth slowed to 5.4% annually.

Overall, the industrial sector may be finding its footing, supported by a strengthening annual performance in working-day-adjusted terms and an uptick in new orders. Meanwhile, construction continues its impressive run, driven by residential demand that significantly outpaces supply. The annual wage dynamics somewhat softened in both sectors, yet remain supportive of household income in both nominal and real terms.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more