- Quick take

- 4 May

- Turkey

Turkey’s April inflation rises more than expected

April's inflation spike confirms a challenging road ahead. The increase in the annual figure was driven mainly by food, housing and transportation

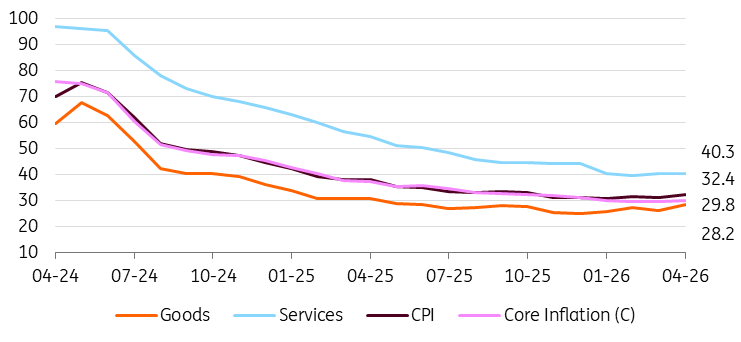

Turkey's monthly inflation in April stood at 4.1%, above the market consensus of 3.2% (and our call of 2.9%), while annual inflation recorded a marked increase to 32.4% from 30.9% a month earlier – above the Central Bank of Turkey's 16% target and forecast range of between 15-21% detailed in its latest inflation report. This shows a significant adverse impact on disinflation, and food, housing, and transportation were the key drivers for the negative surprise in the headline rate. Core inflation (CPI-C) rose by 3.5% month-on-month, leading to a slight increase in the annual rate to 29.8%. Meanwhile, the central bank's managed currency regime, alongside modest nominal lira depreciation in recent months, limited the increase.

Evolution of annual inflation (%)

In April, PPI stood at 3.2% MoM and rose to 28.6% year-on-year, maintaining the uptrend seen in the last three months. In addition to refined petroleum products, food products, crude oil & natural gas, and chemicals were the major drivers of the April PPI increase, likely reflecting the impact of the US-Iran war on some industrial materials and administrative pricing decisions. Global commodity prices – particularly oil prices – in the current geopolitical backdrop will remain the key risk factors for the PPI trend in the near term.

Preliminary seasonally adjusted data, published by TurkStat and closely monitored by the CBT, indicates that the underlying inflation trend in three-month moving average terms recorded across the board increased in the headline, core and services, implying challenges to disinflation in the current environment.

A breakdown of the data shows that:

- The food group made the largest contribution to the headline (0.95ppt), driven by both unprocessed and processed food. Annual inflation inched up to 34.6% vs the CBT’s expectation of 19% for this year.

- The housing group was another contributor (0.90ppt) on the back of administrative price hikes in electricity and natural gas. The key issue worth mentioning in this group is rents, which play an important role in persisting service pricing pressures. Rent inflation dropped to 51.2%, with a further deceleration in the monthly pace compared to the CBT's forecast of a decline to the 30-36% range this year.

- The transportation group followed (0.73ppt) with adjustments in energy prices and transportation services. The sliding-scale tariff mechanism reinstated by the Ministry of Finance has absorbed a significant part of the oil price shock and reduced the impact on the monthly figure.

- Clothing, catering services and household equipment were other items that weighed on monthly inflation. This implies an across-the-board increase in subgroups.

As a result:

- Goods inflation rose to 28.2% YoY, while core goods inflation, recording a slight increase, has remained in the 16-17% range, given the CBT’s tight grip on the exchange rate supporting disinflation in this group.

- Services inflation was flat at 40.3% YoY, remaining elevated and demonstrating the extent of inertia in this area.

Annual inflation in expenditure groups

Overall, April's inflation spike confirmed both the challenging road ahead and an increase in the annual figure. The uncertainty surrounding oil prices, which also affects other commodity prices, presents risks to the inflation outlook, despite the government's efforts to absorb some of the oil price shock through a tax adjustment on petrol prices. The CBT is following the same policy playbook during this geopolitical shock as it did during the local political volatility seen last year, and has prioritised financial stability. While its FX reserves have recovered since the ceasefire in early April, the bank has recently allowed a slightly faster pace of TRY depreciation. The current environment – which poses significant challenges to the Bank given rising energy prices, moderating growth prospects, and dollarisation risks – narrows the room for rate cuts.

In its April MPC statement, the CBT remained cautious and "attentive to upside risks, given that the war has driven an upward shift in inflation expectations as the current backdrop increases the risk of second-round effects." Given this backdrop, we expect that the new inflation report on 11 May will likely reveal a revision of both the target and forecasts.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more