- Quick take

Czech industry comes out of the woods

- 6 February 2026

Industrial output is nearing pre-pandemic peaks, with strength building across sectors. New orders suggest better times ahead, with large deals brightening the outlook. Cheaper energy, also driven by government-subsidised electricity prices for businesses, is starting to kick in

The outlook brightens

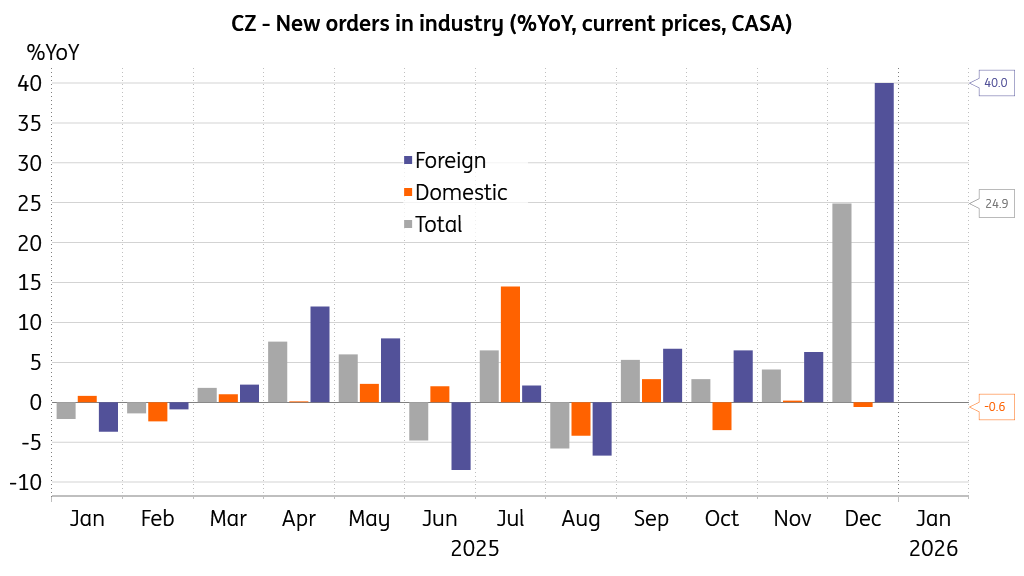

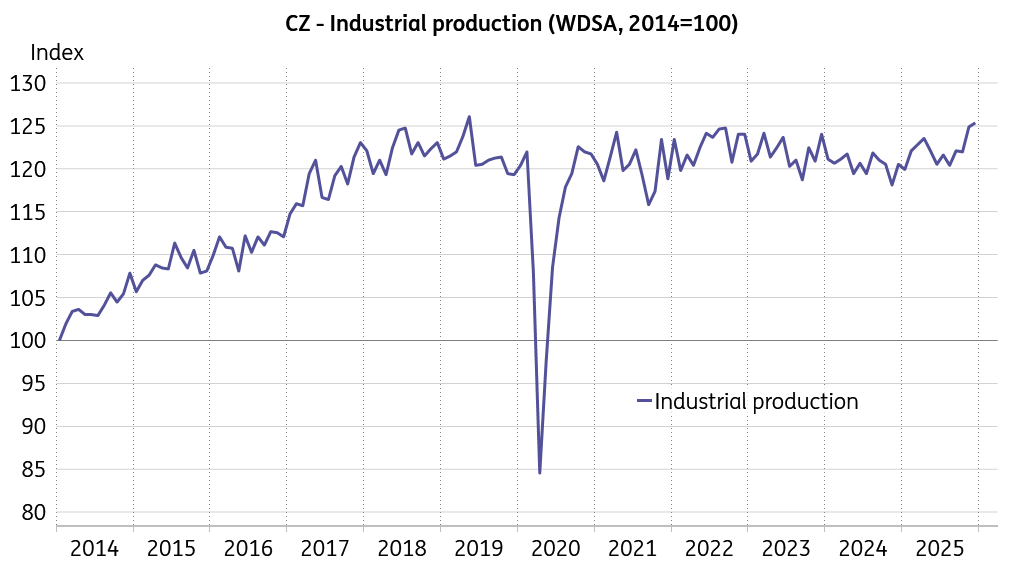

Czech real industrial production added 3.8% year-on-year in December, adjusted for the number of working days, and was 0.4% higher than the preceding month. The nominal value of new orders jumped 24.9% from a year earlier. The end of the year was marked by advances across most industrial sectors, with metalworking, the manufacture of electrical equipment, and machinery among the most vigorous drivers.

New orders improve tangibly

New orders from abroad increased by 40.0% YoY in December, while domestic new orders shed 0.6% in annual terms. When compared to the previous month, the nominal value of new orders gained 18.5%, driven by closing long-term orders in the transport segment. After deducting these extraordinary deals, the value of new orders in industry would have increased by 6% in December. The average number of employees in industry decreased by 1.2% YoY in December, while the gross monthly wage growth picked up to 8% YoY from 5.1% previously. Construction gained 5.3% YoY in December and 1.7% from the previous month. Output in building construction added 2.3% YoY, and civil engineering grew by 10.9% YoY. Employment was 2.4% higher than a year ago, while average wage growth softened to 5.6% annually.

Breaking the chains in hostile conditions

The reading suggests that Czech industry is attempting to break the chains of stagnation after stabilising over the past two quarters. We take the stance that any production is largely a transformation of energy, so subsidised electricity prices are a game-changer for boosting competitiveness. The EU member states are beginning to discuss the corrosive effects of the current Emission Allowances Trading System (ETS1), which mostly harms European firms while leaving overseas producers largely untouched. Indeed, all excessively strict and growth-harmful regulations are fully applied to domestic firms, while there is no capability to enforce them abroad.

Surpassing the previous peak soon

We will see whether these business-friendly steps taken by governments will be enough for European industry to survive, or whether, after some relief, the European Commission will wake up and unleash another regulatory barrage. In this respect, we already wonder how the EU Carbon Border Adjustment Mechanism (CBAM) will be implemented and followed with respect to domestic and foreign entities. Will it turn into another negative supply shock for European firms? Indeed, we are all tense about how much further the old continent’s industrial Sisyphus can push this boulder uphill.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more