- Quick take

- 25 March

- Czech Republic

Czech National Bank can wait it out; the right thing to do

Given the turmoil in the Middle East and its repercussions for energy prices, supply chains, confidence, and uncertainty, we reduce our Czech growth outlook to 2.5% for 2026 and 2027. Our forecast for price dynamics became punchier, yet inflation averages still remain within the tolerance band. Rates on hold is the right CNB answer for as long as it gets

Oil price shock: punchier inflation amid weaker growth

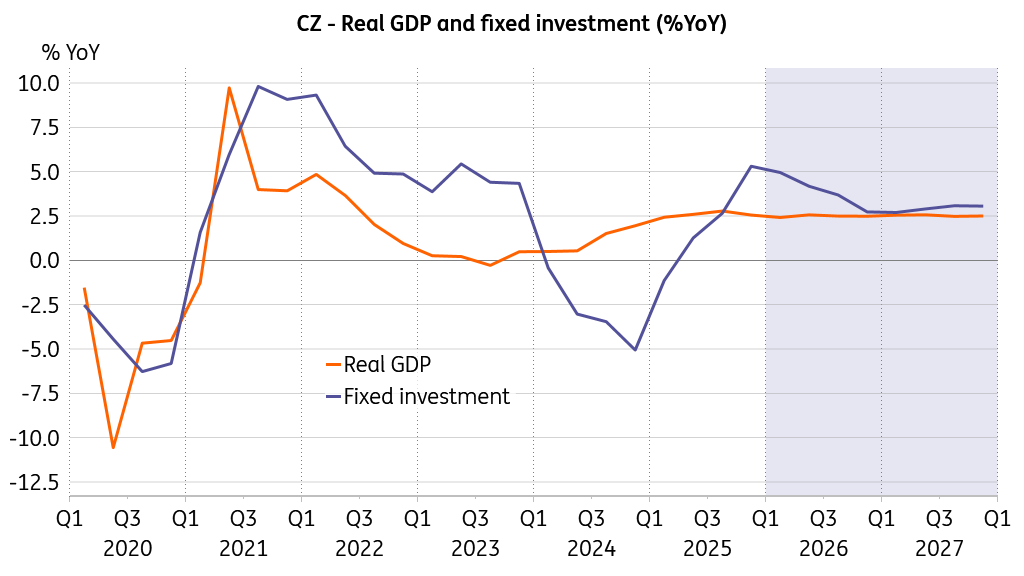

The new Czech forecast assumes Brent Crude averaging around US$100/bbl in March and April and then gradually receding to US$80/bbl in September. On the back of this assumption and expecting the turmoil in the Middle East to imply difficulties for supply chains, basic materials, confidence, and Czech exporters, we reduce our Czech real GDP growth outlook to 2.5% for this year and the next, with quite some potential for further downward revision.

Investment will back down to uncertainty

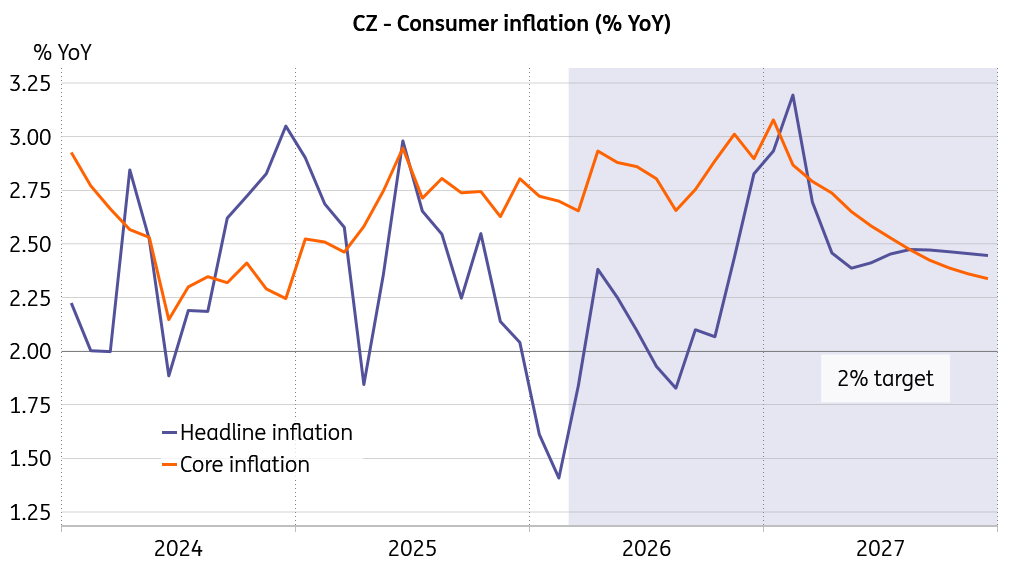

Headline inflation is now seen to average 2.1% this year and 2.6% in the next, as some non-linearities, such as higher regulated prices in 2027 start to kick in. We expect core inflation to average 2.8% this year and 2.6% the next. For now, subdued annual growth in food prices, falling producer prices in agriculture, and declining regulated prices provide a good entry point to the energy price shock and some cushion to withstand it reasonably well. That said, food prices are the right candidate for upward surprises, should potential shortages of fertilisers and other chemicals result in disappointing crop yields across the globe.

Inflation set to remain within the boundries

With the still-decent economic performance and the inflation averages within the CNB tolerance band around the target, we still take the position that – in monetary terms – doing nothing for as long as it gets is the right answer. So, no change in policy rates remains our base case scenario for now, as the initial conditions allow it. Sure, with both headline and core inflation around the 3% threshold early next year, some board members may opt for challenging inflation with higher rates, but the outlook for economic performance will matter. And yes, should we see oil at US$150/bbl anytime soon and the conflict escalates or drags on for much longer, we would tackle another animal once again.

Food price dynamics is an upward risk

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more