- Report

July Economic Update: The Art of the Deal

- 5 July 2019

Politics is increasingly driving economics, with escalating US-China trade tensions and subsequent ceasefire being a case in point. We believe a trade deal will finally be signed later this year, but not before the Federal Reserve and European Central Bank have come to the economy’s aid with monetary easing.

July Economic Update: The Art of the Deal

Politics is increasingly driving economics, with escalating US-China trade tensions and subsequent ceasefire being a case in point. We doubt the truce will hold for long and Europe could yet get dragged into the conflict over the next few months. We believe a trade deal will finally be signed later this year, but not before the Federal Reserve has come to the economy’s aid with interest rate cuts. The ECB is expected to offer stimulus of its own, and the nomination of Christine Lagarde as the bank’s new president has added to this dovish view. Moreover, the political dealmaking in Europe, now under new leadership, looks set to be ramped up as Brexit looms large.

Despite the easing of trade tensions, the Federal Reserve is clearly indicating it is prepared to offer early support to the US economy. Activity data is showing signs of softening, inflation is benign and markets are keen for action. As such, we expect precautionary 25 basis point rate cuts in both July and September.

The market continues to look for more - a third move in 4Q19 with an additional fourth cut in 1Q20. We remain more cautious given our belief that President Trump wants to be re-elected and will therefore be prepared to sign a trade deal, probably in 4Q, that doesn’t necessarily meet all of his initial demands. We assume Trump will want the optimal conditions of rising equity markets and decent economic activity going into the campaign proper, and a trade deal together with lower interest rates can deliver that.

Meanwhile, bond markets are enjoying the art of the steal. On one side of the balance sheet, core issuers are obligated to return less money than they have been lent right out to 10 years. On the other side, investors have eyed the 10yr US at 2% and concluded that that is a steal when compared with other (negative yielding) risk-free rates. Absolute yield levels are discounting all kinds of awful scenarios ahead, partly reflective of a perennial disinflation tendency, but also heavily influenced by a remarkable excess of demand over supply (which the ECB will likely augment).

The eurozone economy is still desperately seeking guidance and support. Confidence indicators have started to deteriorate again, and a rate cut is now a question of ‘when’ rather than ‘if’. It’s a close call, but barring a further deterioration in the data before the July meeting, we think the ECB is more likely to wait until September when it will have a new set of staff projections.

Concerns are growing that a new UK prime minister could pursue a ‘no deal’ Brexit, although we still think parliament would force a general election if there were no alternative way to stop it. All of this uncertainty is continuing to weigh on growth and a Bank of England rate hike this year looks unlikely.

Even after the China-US sideline meeting at the G20 in late June, it is still too early to say that the two sides are close to reaching an agreement. Technology is the big issue, but it seems to us little can be done. China needs more infrastructure investment, both for stimulus purposes and for achieving technology independence. The central bank needs to support these projects by adding more liquidity to the market. USD/CNY has been more affected by a weak dollar than the outcome of the G20.

The eight year dollar bull run is showing signs of fatigue – but is not giving up without a fight. We suspect that an escalation in trade tensions will prove the catalyst for a fresh bout of dollar losses – especially in USD/JPY.

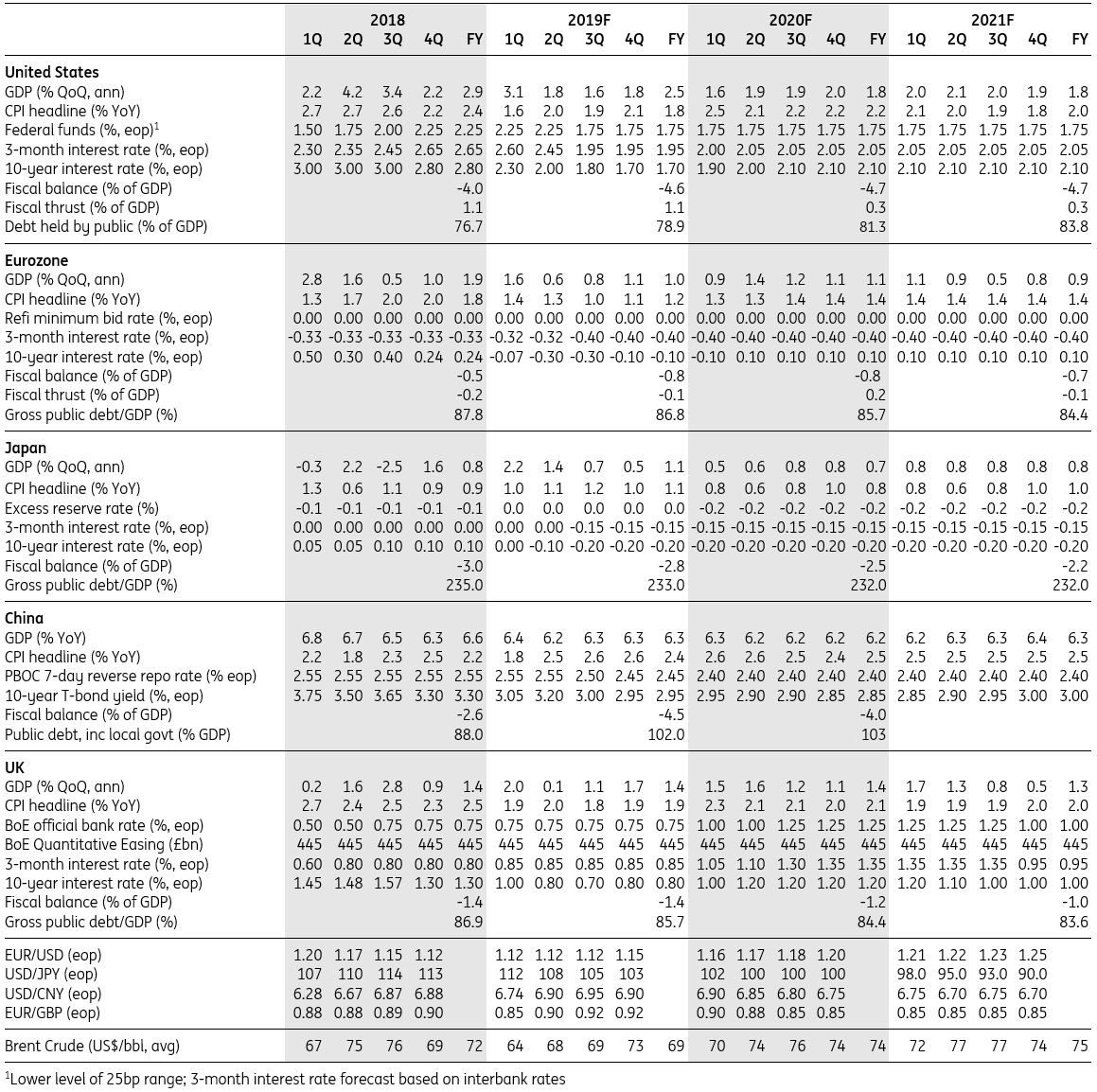

ING global forecasts

Included in the following bundle

What’s happening in Australia and the rest of the world?

- This bundle contains 7 Articles

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more