- Report

ECB Crib Sheet

- 22 January 2018

- FX

How markets could react to Thursday's ECB meeting.

Download the print-friendly infographic below

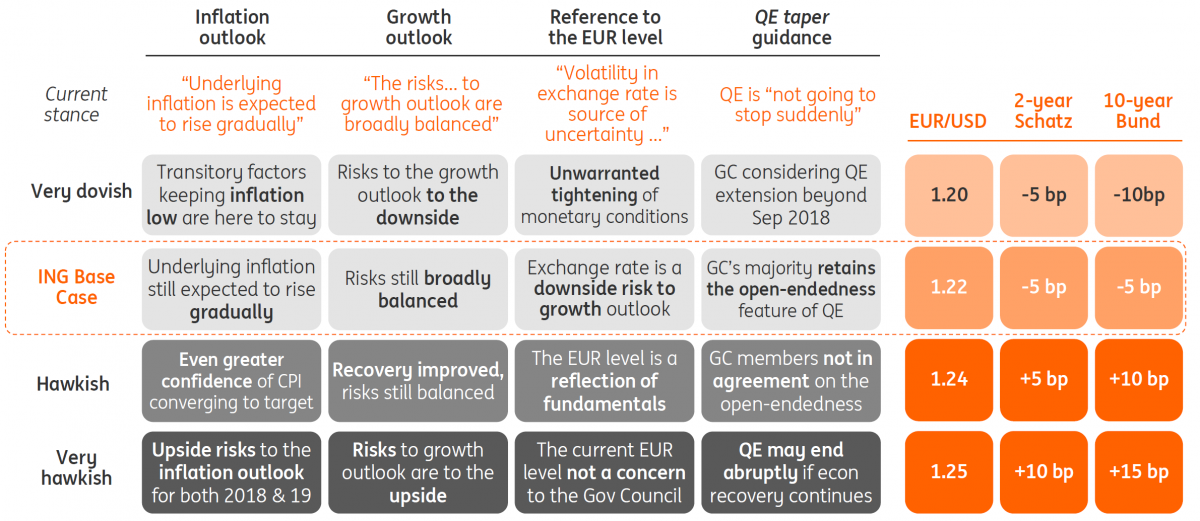

Scenario analysis

Taming the hawks

We expect President Draghi to convey a rather dovish message and tame the market’s hawkish fantasies (at least for now). The President is likely to point at still weak inflationary pressure, emphasising the disinflationary impact from a stronger euro. Indeed, every time hawkish comments dominate the ECB debate, the euro appreciates and immediately provides ammunition for the ECB doves. The key thing to watch: Whether Draghi confirms the October statement that there will be no sudden end to QE.

We expect him to do so as this would be the only way – at least temporarily – to get the genie back in the bottle. It would also show Draghi’s magic of how to guide financial markets with very few words and without any action. Interestingly, the ECB has picked up the narrative from Draghi’s Sintra speech and is increasingly focusing on growth, considering inflation only as a derivative of growth developments.

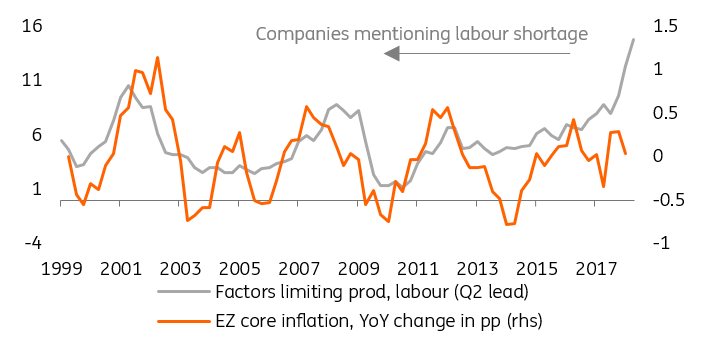

Labour shortages and core inflation

What this means for FX markets

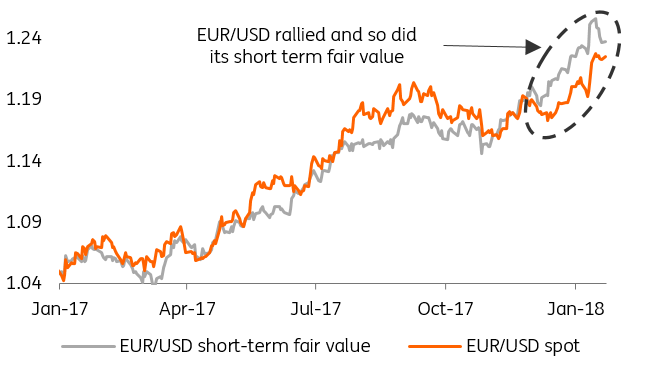

High hurdle to send EUR lower

The likely cautious tone of the ECB meeting should put a limit on the scale of EUR upside rather than driving it lower. This is because

(1) even on the very short term valuation basis, the EUR/USD still remains modestly undervalued;

(2) market’s base case of a cautious ECB tone, following the comments of various ECB board members;

(3) solid EZ economic outlook and the recent data upside surprises have lowered the credibility of the threat for further and material QE extension.

Euro vs. fair value

What this means for bond markets

Hawkish surprise less likely after recent ECB push back

Despite the recent pushback by ECB officials yields are still significantly higher than before the ECB minutes. We believe markets still await a dovish confirmation, which should prompt moderately lower Bund yields, key being the confirmation that there will be no sudden end to bond purchases. The upside in rates on any disappointment in this regard is moderated by valuation models versus swaps suggesting that Bunds are now trading less rich compared to past months.

German swap spreads vs. fair value

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more