They’ll be home by Christmas

- 2 April 2020

- Malaysia Singapore

No, not a prediction, just a reminder not to succumb to unjustified optimism.

Remember - long haul

The First World War started enthusiastically, with thoughts that our boys (on both sides) would "be home by Christmas". And I thought this was a good way to start today's note after earlier in the week I suggested that this might be a time to become less bearish on risk assets.

Despite being a perma-bear, I feel obliged sometimes to try being positive, even when it goes against my natural instinct. That isn't always a successful venture. I'm much more comfortable, and much more accurate when forecasting disaster. I shall be much more restrained in future.

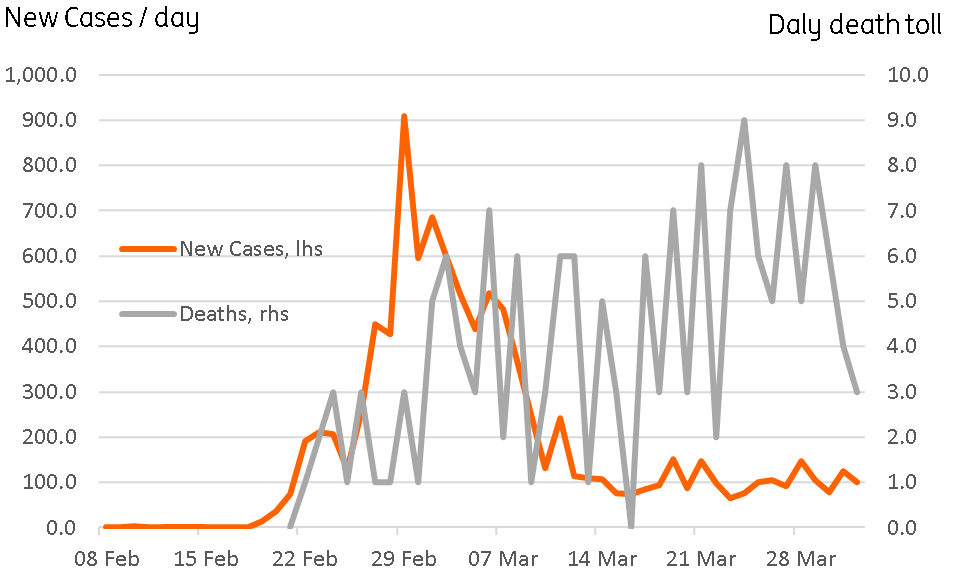

That said, the covid-19 news earlier in the week on Europe's big countries was and remains encouraging though the peak in new cases has been far from smooth, and there are still some pretty horrible days for some countries.

Some European leaders overnight have been extending their countries' lockdown periods (including in Germany and Italy), and when you look at how Korea's case history has proceeded, you might also be reminded of Joseph Heller's Catch-22, where the limit on bombing runs was never quite reached for the unfortunate pilots. A sombre message from the White House yesterday is also in line with this grimmer outlook as the US softens up its public for what might be a long slog.

Korea got on top of its Covid-19 outbreak early. But for almost a month now, new cases have been steady at about 100 a day. Would Seoul ease back on movement restrictions with new cases still running at these levels? Would Rome or Berlin? These lockdown extensions are likely to be pushed incrementally out in small chunks just to prevent morale from crashing too badly. But we might be stuck at home for months. And that means that businesses will remain shut for months, and the economic cost will be far higher than under an optimistic view. That probably means remaining cautious on risk assets, even if the worst of the plunges might be over, we may still not have reached the bottom yet.

One positive note, on all of this, markets are behaving more "normally" than a week or so back. When stocks fall, so do bond yields, and the 10Y US Treasury is now down to about 57bp. We have also seen the 3M Ted spread narrow slightly, which we haven't seen for a bit. So it's not all doom and gloom.

Korean Covid-19 new cases and daily death count

Day ahead

It is not very busy on the economic calendar today, and despite the market's reversion to pessimism overnight, yesterday's US economic data wasn't actually too bad. The March manufacturing ISM index was only slightly down at 49.9 (though some of the sub-components, including new orders and employment, were quite bad), and the ADP survey was much less negative than the consensus at only -27K ahead of tomorrow's US jobs report.

Despite the lack of data, Prakash Sakpal has been busy revising his forecasts lower and today he writes:

"Singapore: We noted yesterday that the relaxation of existing property cooling measures would go some way to supporting sentiment as Covid-19 tightens its grip on the economy (infections touched the 1000 mark yesterday). Support for the policy shift comes from the advance property price data for 1Q20 showing a 1.2% QoQ fall in home prices. Not so much during SARS, but property was the worst-hit part of the economy during the global financial crisis in 2008, with up to 25% price falls.

Thailand: It’s going to be the worst year since the 1998 Asian crisis. Following on the heels of its record low manufacturing PMI, the Business Sentiment Index for March pointed to as much as a 2% GDP contraction in 1Q20. We anticipate over a 7 percentage point fall in activity in the current quarter as a result of the partial shutdown. Our full-year growth forecast is now revised to -4.3% from -0.8%, which would be the steepest GDP fall since the 1998 Asian economic crisis (Thailand was the epicentre of this with over a 7.8% plunge in the country's GDP that year). We also add 50 basis points of rate cuts to our central bank policy forecast and see the THB weakening to 35 against the USD by end-2Q20.

Malaysia: We are also cutting Malaysia’s 2020 growth forecast to -2.9% from +1.8% earlier as the extended lockdown of the country to stem the Covid-19 spread is poised to dent growth deeper into the negative territory in the first two quarters. Hopes are pinned on monetary and fiscal stimulus helping the economy back to slightly positive growth in the final quarter. We maintain our view of a further 50bp Bank Negara policy rate cuts in the current quarter, with a bias towards more cuts than that. We forecast USD/MYR at 4.55 by end-2Q20".

On China, Iris Pang also notes "At the Politburo meeting on Wednesday the government pointed out the need for targeted RRR cut for inclusive finance, including SMEs. Usually, the PBoC will follow such instructions within days. But this time, the PBoC may want to delay doing so as long as it can, as market interest rates fell yesterday after the quarter-end and the central bank does not want the targeted RRR cut to put further downward pressure on rates. If overdone, this could result in a very low interest-rate environment. A 0.5 - 1.0 percentage point targeted RRR cut is more possible over the weekend or even further away this month than it is today or tomorrow."

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 2 April 2020

- This bundle contains 3 Articles