- Opinion by Padhraic Garvey, CFA

Tequila Turn: Mexico to front run the US

- 18 July 2023

- Rates United States

The market discount sees a Mexican central bank rate cut from November. We agree, and we in fact can see rates being cut faster than the market discounts thereafter. There is a lot of comfort built in. This can be gleaned from the appreciation in the peso and falls in market rates. The next step is to prepare for a marked dis-inversion of the curve, ahead of the US

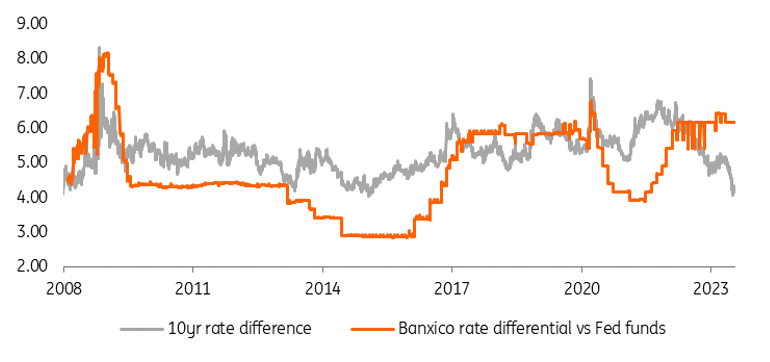

There is a high degree of policy comfort built into the Mexican curve (TIIE), so much so that we are more and more inclined to anticipate initiation of a material easing process in the coming months. The policy rate at 11.25% is some 6% above the Fed funds rate, representing quite a large cushion. It has only been wider on two occasions in the past 15 years – emergency Fed cuts during the Great Financial Crisis and the same at the onset of the pandemic. There is no requirement for this spread to be wider. In fact, we believe it will narrow as the Fed hikes some more, while Banxico holds pat.

A glance at the chart below highlights the elevation of the official overnight rate, and its excess over the interest rate differential to the US. That differential is at or about highs. Technically, Banxico started its pause before the Fed did, and is likely to extend it at its August policy setting meeting, while the Fed suspends its pause by hiking at its July meeting. There is a Mexico turning point theme coming from this, in anticipation of something similar from the Fed down the line. Banxico should be in a position to front run the Fed.

Mexico central bank rate is stretched, and also versus the Fed funds rate...

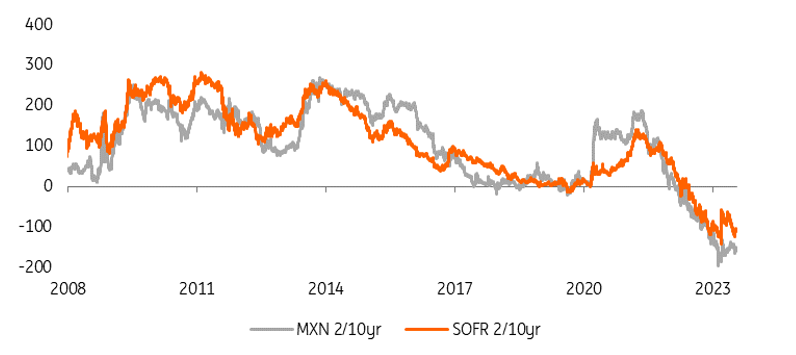

A decent portion of this front running theme is already being seen in market rates. In contrast to the ongoing elevation in the policy rate differential, the 10yr market spread (TIIE vs SOFR) is now at 4.3%, in from a cycle high at 6.75%. The chart below illustrates the contrast, and shows that 10yr spread at the tight end of the range seen over the past decade and a half. Right now, the 10yr market spread looks tight while the policy rate differential looks wide. The tightening in market spreads has correlated with the ongoing appreciation in the peso (MXN), with both reflecting a comfort factor coming from the wide front-end rates differential.

The Mexico 10yr rate spread to the US looks quite tight versus the central banks rate spread

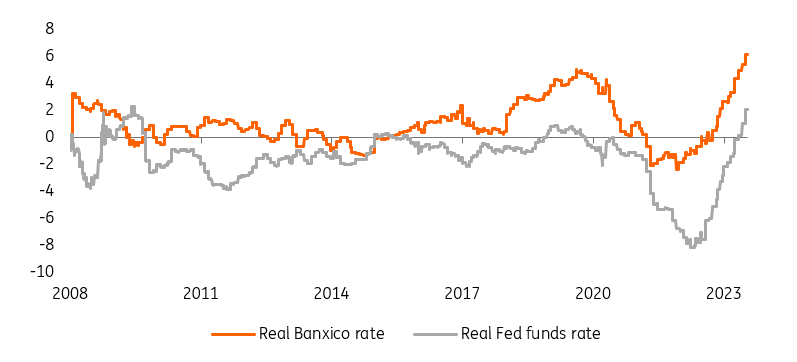

Material and ongoing falls in Mexican inflation pushes in the same direction, with the fall in the headline rate from almost 9% to 5% facilitating the material falls seen in longer tenor market rates. As Mexican inflation falls and the policy rate rises and remains elevated, the result is a significant rise in real rates. The chart below shows the Banxico real rate alongside the Fed funds real rate (based off headline inflation). There is a 4% real rate differential in favour of Mexico. This is quite a comfort blanket. Recent MXN appreciation, in turn, is in part a manifestation of policy comfort built in real rates space.

The Banxico rate is well above inflation, a high implied real rate

One implication of this has been the evolution of quite a pronounced inversion of the 2/10yr curve. The US curve is extremely inversed. But the inversion on the MXN curve is even more pronounced. The big question is when are these curves set to materially dis-invert. The US curve is not quite ready yet, as the Fed continues to hike. But the MXN curve has enough front-end comfort to begin the dis-inversion process sooner. Typically it does not stray too far from the US curve, but this time we think it can.

The Mexican curve is consequently heavily inverted, even deeper than the US one

When we look for directional turning points we like to take note of the positioning of the 5yr on the curve through the 2/5/10yr butterfly. This is essentially where the 5yr rate sits versus an interpolation between the 2yr and the 10yr. Currently the 5yr is exceptionally rich, mostly reflecting a deep inversion on the 2/5yr segment. When the curve dis-inverts, the bulk of it will happen on this segment, correlating with a de-richening of the 5yr to the curve. Right now it looks like the 2/5/10yr has topped out, and there is room for a bigger movement on the MXN curve (than on the USD curve).

Changes in curve trends tend to be quite synchronized between MXN and USD, but as the cycle turns ahead the MXN curve can lead the dis-inversion process. Right now, dis-inversion strategies are a pain trade from a carry a roll perspective. In the next 6 months there’s a 40bp carry and rolldown cost to 2/5yr MXN steepeners and 85bp for 2/10yr MXN steepeners.

Generically from here we like dis-inversion trades. But we’d prefer to set them with more conviction once the Fed has actually peaked. That said, the cushion here is the MXN curve which is really primed to dis-invert with some aggression, likely ahead of and more dramatically than the US curve will.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more