- Opinion By Peter Virovacz

Moody’s latest decision on Hungary gives false sense of security

- 4 September 2023

- Hungary

Moody’s decision to affirm Hungary’s Baa2 rating with a stable outlook came as a positive surprise. However, we are not entirely comfortable with their argument, particularly the balanced risk assessment, which could lead decision-makers to become complacent

On 1 September, Moody's affirmed Hungary's rating at Baa2 with a stable outlook. The stable outlook indicates that the risks are balanced, but we disagree, as we believe the risks are tilted to the downside, hence our earlier expectation of a downgrade to the outlook. In our view, the recent decision provides a false sense of security and may lead policymakers to become complacent at a time when growth prospects are deteriorating, and fiscal problems are mounting. These risks have led us to be more downbeat overall.

The rating agency highlighted in its statement that it expects Hungarian GDP to stagnate this year. Given the economic performance in the first half of 2023, this would require GDP to grow by at least 1.9% quarter-on-quarter in both the third and fourth quarters, which we consider highly unlikely. The last time we saw such a solid performance was in late 2021 and early 2022. But back then, growth was fuelled by positive real wage growth, supportive monetary policy, very accommodative fiscal policy and, of course, some Covid rebound dynamics. Before the Covid-rebound period, such a sequence of strong growth had never happened.

Although we expect the economy to perform better in the second half of the year, we are concerned that the hole dug in the first half of the year is too deep to climb out of quickly. In this regard, we have downgraded our full-year GDP forecast from 0.2% to -0.5% year-on-year, as we now see a recession in 2023.

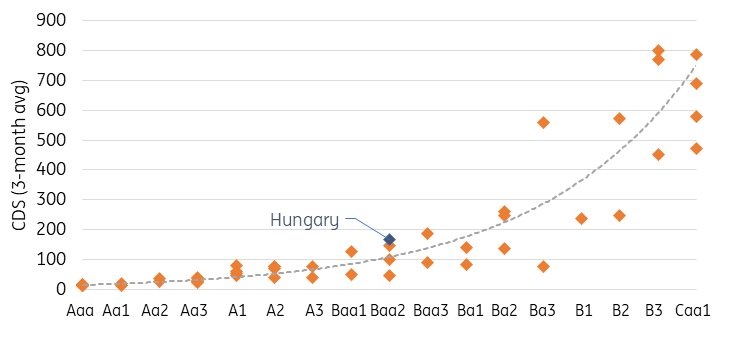

CDS and sovereign credit rating (Moody’s)

As for the nominal growth outlook, the GDP deflator is around 8% based on the first-half data, while the government had planned for 15% for the year combined with a 1.5% real GDP growth. Although the GDP deflator will definitely rise in the second half of the year (based on seasonal patterns), we believe that the risk of not reaching 15% is non-negligible. On top of that, as we mentioned earlier, real wage growth will be negative this year, in our view.

And nominal growth matters a lot when it comes to fiscal measures where the nominal GDP is the denominator, like in the deficit-to-GDP and in the debt-to-GDP ratios. The latter reached 75% at the end of the second quarter, which is 5.3 percentage points higher than the government's 2023 target in the latest Convergence Programme. With further weakness in the nominal GDP, the goal to reduce the debt-to-GDP ratio is getting harder, especially with the recent slippage in the deficit. In addition, the Hungarian government has not given up on the acquisition of Budapest Airport, which would be financed by FX bond issuance in our view, and hence would add to the debt burden of the country.

Speaking of the budget shortfall, Moody's expects a 0.3ppt increase in this year's deficit target to 4.2% and a 0.6ppt increase in the 2024 target to 3.5% but does not hold the government accountable or flag this as negative. In the wake of the reinstallation of the Excessive Deficit Procedure, admitting that the government will miss the 2024 sub-3% deficit target and being negligent looks interesting. Moreover, like us, they include the scenario of an agreement with the EU but do not highlight this as a very significant risk factor.

Moreover, we respectfully disagree with the positive elements listed by Moody's. It cited Hungary's "strong embeddedness in manufacturing" as a positive factor, which seems very odd to us at a time when the global economy is in a manufacturing recession. It also noted that the improvement in the trade and current account balances was due to a much lower dependence on Russian energy sources, which we see as a false interpretation of data. First, Russian energy dependence has not fallen significantly based on import statistics. Second, the improvement in external balances has occurred because domestic demand has collapsed, reducing the need for imports (including energy and non-energy goods), while energy prices are very much lower than last year. And finally, Russian contractor Rosatom started works on the first phase of construction of the new Paks Nuclear Power Plant (Paks II) units in Hungary, which hardly can be seen as a reduction of energy dependency.

Taking all these factors into account, we believe that Moody's has underestimated the negative risk impact of economic activity, fiscal policy and geopolitical issues, thereby providing a false sense of security at a time of heightened uncertainty about the country’s short-term general outlook.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more