Will eurozone wage growth accelerate despite the economic slowdown?

- 28 April 2022

Wage growth was sluggish in 2021 and now the economy is slowing down. An acceleration is still in the making, but the economic slowdown and weakening profit margins are set to make the wage growth recovery more muted

On the eve of the war, wage growth was ready for take-off

The labour market was performing exceptionally well before the Ukraine war began. In the aftermath of the pandemic, there was no surge in unemployment despite governments winding down fiscal support. In fact, unemployment has continued to trend down thanks to the powerful economic recovery. This resulted in an unemployment rate of 6.8% in February, the lowest rate on record for the eurozone. At the same time, the eurozone also recorded the highest vacancy rate ever.

According to the European Commission’s estimates, the unemployment rate has even dropped below the natural rate of unemployment, the rate below which wage growth is set to rise. That was before the start of the war, however, which will no doubt be a game-changer for economic growth and will probably also affect the labour market. Since we don’t expect unemployment to run up materially again, and with historical tightness in February, the eurozone labour market is set to result in some continued wage pressures in the months ahead.

Unemployment has dropped to a record low, in line with wage acceleration

Surge in inflation pushes up nominal wage demands…

The second reason for us to expect nominal wage growth to accelerate is the spike in inflation. The inflation rate is a key driver of wage growth. After all, it is the purchasing power of wages that counts for employees and therefore inflation provides a benchmark for nominal wage increases. We see that this empirically holds up as inflation leads wage growth by two quarters historically. In the current extreme situation, we don’t expect the relationship to hold up as well as it does in more ‘normal’ times, but we definitely expect it to result in upward pressure on wages.

This is in part driven institutionally of course as Belgium, Spain and France have negotiated wages, to a varying degree, automatically adjusted to past inflation (APC). In some other eurozone countries, only certain wages are subject to APC. Usually, this concerns minimum wages (either negotiated or set by law). The majority of euro countries do not, however, have any form of automatic indexation to past inflation. But in those cases, inflation can still play a formal role in the wage-setting process. In Italy, for example, the inflation forecast of the National Institute of Statistics is the official benchmark for wage agreements at the sectoral level.

In countries where inflation rates do not have a formally determined role in wage-setting, it is, nevertheless, always one of the indicators that labour unions use when deciding on the level of their wage demands. Both backward- and forward-looking inflation rates are apparent in the wage-setting schemes of unions in different European countries.

…but less than in the past

A surge in inflation due to temporary cost increases such as spikes in energy and or food prices turns relatively easy into more persistent high inflation levels in countries where there is APC and in countries where labour unions base their wage demands, among other things, on past inflation. In its economic bulletin of July 2021, the ECB concludes that the share of employees whose wages are subject to APC has decreased somewhat since the GFC. Also, the number of countries where unions predominantly look at past inflation has decreased.

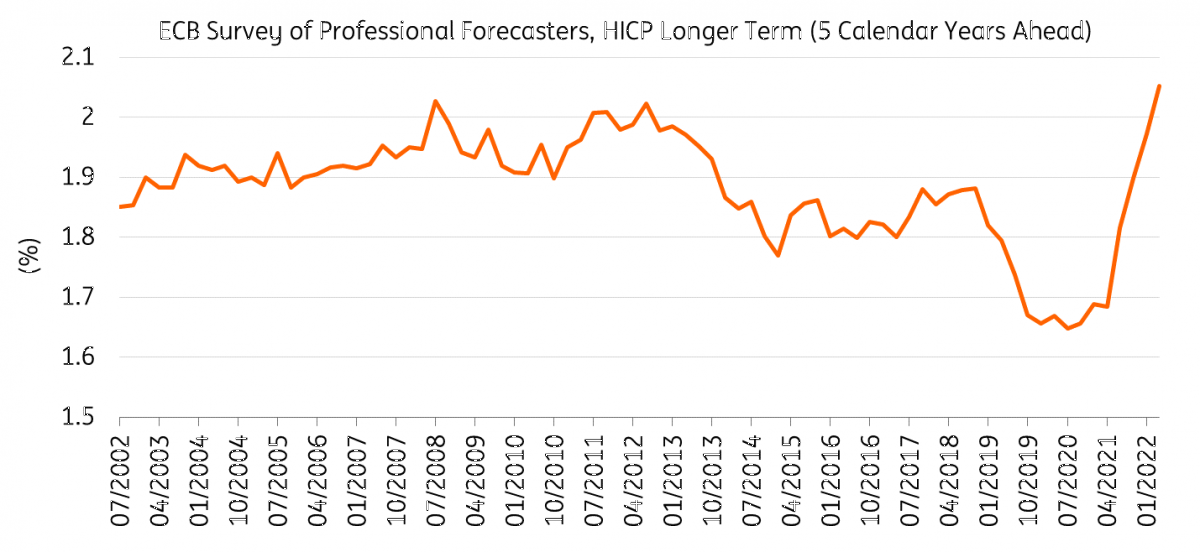

Therefore, the recent surge in inflation will exert less upward pressure on wages than it would have done in the past. But, nevertheless, upward pressure will remain. Even unions that only look at future inflation when setting wage demands will increase their demands this year because expected future inflation has also been increasing across the eurozone in recent months – as this chart shows.

Future inflation expectations have been rising rapidly since mid-2021

Is 2008 anything to go by?

The question is whether the expected economic shock coming from the war in Ukraine is not going to be a game-changer for wage growth expectations. A recession will surely impact wage growth, but historically it does so later than you’d initially expect. History shows that unemployment lags economic growth. Data for previous episodes of economic turnarounds confirm these lags.

When looking back at previous episodes of high inflation followed by recession, we see that 2008 saw a similar runup. While everyone thinks of the Lehman Brothers bankruptcy as the defining moment of the recession, economic activity had already peaked at the end of 2007 while the bankruptcy happened in September 2008. Before the recession started, commodity prices had soared to unprecedented levels and this was subsequently met by a strong surge in inflation. That in turn resulted in increasing wages as inflation was already dropping on the back of recessionary pressures. In fact, even in the last quarter of 2008, when the crisis had deepened significantly, wage growth reached its peak. After that, the deflationary impact of the crisis resulted in wage moderation, which indicates that recessionary forces do lead to moderating wage pressures in the medium-term.

The commodity price surge of 2007 was followed by rising wage growth until after Lehman

Despite slowing growth, expect wage growth to accelerate

Two big effects are playing into wage negotiations in the coming quarters: the surge in inflation and loss of purchasing power on the one hand, and the recessionary impact of the war on the other.

The war in Ukraine will surely be a game-changer for economic growth in 2022. This will subsequently influence the labour market as well. The increasing recessionary tendencies and lower profit margins, due to higher energy and transport costs, will limit the means of businesses to finance high wage increases. On the other hand, adjustments of nominal wages to inflation are nowadays less automatic and more often based on expected inflation instead of past inflation. Since both are increasing, although the latter more moderately, this means that the recent surge in inflation will still push up nominal wage growth expectations.

Given the high uncertainty about the duration and impact of the war on the economy, it is tough to forecast wage growth at the moment. Nevertheless, because of economic and institutional lags, we believe it to be plausible that the effect of the economic slowdown on wage growth will be larger next year than this year. Therefore we expect negotiated wages to rise cautiously over the course of this year and next despite the economic slowdown and huge uncertainty stemming from the war. Not enough to compensate for purchasing power losses, but this second-round effect is enough to set core inflation expectations somewhat higher for the medium-term.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more