Fears of another eurozone crisis are overblown

Despite a challenging outlook for the eurozone, the prospect of another debt crisis seems unlikely. There are few signs of economic divergence, debt levels are sustainable and support for the monetary union has increased significantly in recent years. Still, speculation about a crisis can be a self-fulfilling prophesy and much will depend on politics

The de facto pre-announced European Central Bank rate hikes, the end of net asset purchases and a looming recession have led to widening spreads in the eurozone, pushing borrowing costs in some countries to their highest levels in almost 10 years. Widening spreads and high borrowing costs for governments have brought back fears of a new euro crisis. While the current economics argue against this, there is still a risk that political events could push the eurozone back into an existential crisis. The monetary union has always been a project where politics dominates economics.

The reason for this new concern over another euro crisis is clear: the ECB’s announcement of normalising monetary policy; ie the end of negative interest rates, a potential further series of policy rate hikes and the end of net asset purchases. Remember that Southern European bond yields benefited relatively more from the flow of asset purchases, while Northern European bond yields benefited from the stock effect. With the ECB’s dwindling support, Southern European bond yields have already started to increase. While some spread widening is normal in times of rising interest rates, there is a risk that markets start to doubt the ECB’s commitment to be the lender of last resort in the eurozone, especially if more indebted countries face debt sustainability issues in the wake of rising rates. In other words, markets may question how the ECB can combine Mario Draghi’s 'whatever it takes' promise with raising interest rates and going cold turkey on net bond buying.

The ECB’s dilemma of hiking rates without creating bond market turmoil

The ECB’s answer to the dilemma of hiking interest rates while at the same time ensuring that spreads remain contained is twofold. Reinvestments from the central bank's Pandemic Emergency Purchase Programme will be conducted flexibly, and the ECB is preparing a so-called anti-fragmentation tool.

Regarding PEPP reinvestments, the ECB’s current plan seems to imply that it will use the proceeds from maturing bonds from what the ECB perceives as strong countries to buy bonds of the weaker countries. A third group of countries, “the neutrals”, would act as a buffer if the proceeds from maturing bonds from strong countries do not suffice to quell the tensions in the bond market. All of this means that, for example, maturing German bonds can be reinvested in Italian bonds. We doubt that the German Bundesbank will really be happy to swap German bonds for Italian bonds. But more fundamentally, there will be questions as to whether this flexibility can be applied legally for the whole reinvestment period, or whether this is just a temporary measure. This would essentially mean that during the reinvestment period, the capital key would no longer be respected.

Italy has roughly €200bn of bonds maturing each year and over €100bn of bills. While daunting, we’re ready to assume that, on aggregate, existing holders of peripheral bonds will roll their maturing bonds into new ones, as the ECB will do. The more pressing issue is who will buy the new issuance to finance government deficits. According to the European Commission’s latest forecast, Italy’s general government deficit will amount to €100bn this year, going down to €85bn next year. The majority will be financed by bond issuance, raising the question of what investor class will be willing to increase its exposure to peripheral bonds.

Full reinvestment of core redemptions into peripheral bonds would cover near term deficits

Reinvestments could deliver sizeable help in financing new debt issuance

A change in the PEPP redemption policy would go some way towards bridging that gap. Bloomberg reported that €12bn of the €17bn average monthly PEPP redemptions are in core countries, and thus available to invest in the periphery. At full capacity, and splitting this amount between Italy, Spain, Portugal, and Greece according to the ECB capital key, they could cover 70% of Italy’s financing needs in the second half of 2022, and 86% in full-year 2023. Of course, these amounts are unlikely to be reinvested in their entirety into peripheral bonds, but this goes to show that at full speed, reinvestments could deliver sizeable help in financing new debt issuance. On the other hand, they are wholly insufficient to offset a run on these bond markets should existing investors decide to sell out of their holdings, or decide not to roll maturing bonds into new ones.

Regarding an anti-fragmentation tool, the ECB’s mid-June announcement to speed up the ongoing work suggests that details should be presented soon. This anti-fragmentation tool has led financial markets to infer that the ECB will do “whatever it takes”. But this is not necessarily what the ECB will deliver. In fact, at the start of the euro crisis, the ECB was concerned about widening spreads and disrupted monetary policy transmission. Back then, the ECB introduced the Securities Markets Programme (SMP) - a tool allowing the ECB to purchase government bonds. But these purchases were sterilised. The programme only included very light conditionality as it came in reaction to national governments announcing certain reforms. However, when the euro crisis accelerated, the SMP turned out to be too ineffective, which prompted ECB President Mario Draghi to announce his famous ‘whatever it takes’ pledge, and the ECB to later formalise this in the so-called Outright Monetary Transactions (OMT). OMT was linked to strict conditionality, like a rescue or even bailout package from the European Stability Mechanism (ESM). The OMT was never used as the announcement itself turned out to be sufficient to bring spreads back to more sustainable levels.

Two main challenges for the anti-fragmentation tool

Applying the historical lessons to the current debate, the ECB is facing at least two main challenges in developing its new anti-fragmentation tool: how to determine a fundamentally ‘warranted’ spread between countries and how conditionality should be defined.

One option to define ‘fundamentally warranted’ spreads could be to refer to the official EU convergence criteria. Here, a spread of 200bp vis-à-vis the average bond yield of the three countries with the lowest inflation rate is a requirement to become a member of the monetary union. Bear in mind that this is not the same as the spread with Germany, as Germany is not necessarily one of the three countries with the lowest inflation rate. However, media reports on the anti-fragmentation tool signalled that the assessment of widening spreads was gauged against German bonds, which are the de facto benchmark for the eurozone.

In practice, we see that the ECB decided to intervene when Italian-German spreads approached 250bp. Of course, the speed of the increase in spreads will have played a role as the ECB seems to want to stay ahead of another debt sustainability crisis, but somewhere between 200 and 250bp could be a trigger point for the ECB.

The focus seems to be on the speed of the widening, rather than the level of spreads

Between the (voluntary or not) leaks and public comments made by governing council members, we gather that the ECB wants to avoid making public its intervention rules. In that regard, setting firm spread targets, whether public or not, can be problematic. Instead, the focus seems to be on the speed of the widening, rather than the level of spreads. The effect would be to reduce volatility in sovereign spreads, but not to impose a hard cap. In the likely event that the buying capacity of this new instrument is limited, this is probably the best that can be achieved anyway.

Without knowing its exact buying capacity, it is difficult to say whether the new instrument would be able to prevent a full-blown run on peripheral debt. We suspect it wouldn’t, but this may not be necessary. Flexible PEPP reinvestments could take care of some of the periphery’s net financing needs (see above), while the new fragmentation instrument has the more important task of drawing private investors back into the peripheral bond market. Think of QE as crowding out private investors. The new instrument needs to crowd them in.

As the ECB reduces its exposure as a percentage of the amount of debt available (since it grows each year with government deficits), marginal buyers are likely to be mostly yield-sensitive investors. This means that wider spreads are part of the solution for them to grow their exposure, rather than part of the problem. This is why hard spread caps would be detrimental to the ultimate goal of restoring the market functioning, in addition to being very difficult to achieve.

By reducing volatility, the ECB would make investors more likely to accept lower spreads

Where the ECB’s new instrument has a role to play, in our view, is in reducing the realised volatility in peripheral spreads. Investors compare their returns to potential risk. An investor who knows that the risk of buying peripheral bonds has been reduced by the ECB would, in theory, expect lower yields and tighter spreads.

Regarding conditionality, an ESM bailout or even a lighter rescue package still seems to come with too much stigma for most Southern European countries. Alternatively, the ECB could try to link its anti-fragmentation tool to the national reform programmes and whether or not countries have met the criteria to be eligible for funds from the European Recovery Fund. However, such conditionality would be finite as the European Recovery Fund is not a permanent institution. Alternatively, the ECB could link any bond purchases to a country’s compliance with the Stability and Growth Pact. However, the ECB can hardly do this as long as the escape clause is active, i.e. there is no excessive deficit procedure triggered for breaching the 3% of GDP deficit threshold. This basically means that it could only apply to the 2024 budget at the earliest, when the Stability and Growth Pact rules come back into effect. To further complicate things, we shouldn’t forget that an exercise is underway to reform the Stability and Growth Pact, and there has actually never been a procedure against countries breaching the 60% of GDP debt threshold. Conditionality on the European semester recommendations would be a relatively light solution that is not time-limited like the European Recovery Fund reforms.

Sterilising any bond purchases would make conditionality a less pressing issue but the experience with the SMP is that sterilised purchases are not powerful enough to really fend off a speculative attack.

We expect the ECB to present some initial guidelines on an anti-fragmentation tool at the 21 July meeting. There will be a trade-off: the more rate hikes the ECB plans to implement in the coming months, the weaker the conditionality of such a tool.

The everlasting topic of lender of last resort

The entire discussion on an anti-fragmentation tool actually focuses on the question of the eurozone's lender of last resort. The absence of such a role and the no-bailout clause was actually a crucial element for the founders of the monetary union who hoped that this arrangement would enforce sufficient discipline on countries and governments to use structural reforms as the main adjustment tool. The euro crisis between 2010 and 2012 illustrated the flaws of this concept. In the end, there were bailouts and the ECB took over the role of lender of last resort, with Mario Draghi’s ‘whatever it takes’ speech. The discussion on the new anti-fragmentation tool of the ECB should not blur the broader debate: who will take over the role of lender of last resort and could the monetary union survive without it?

Why this is not the return of the euro crisis

External shock vs country-specific shock

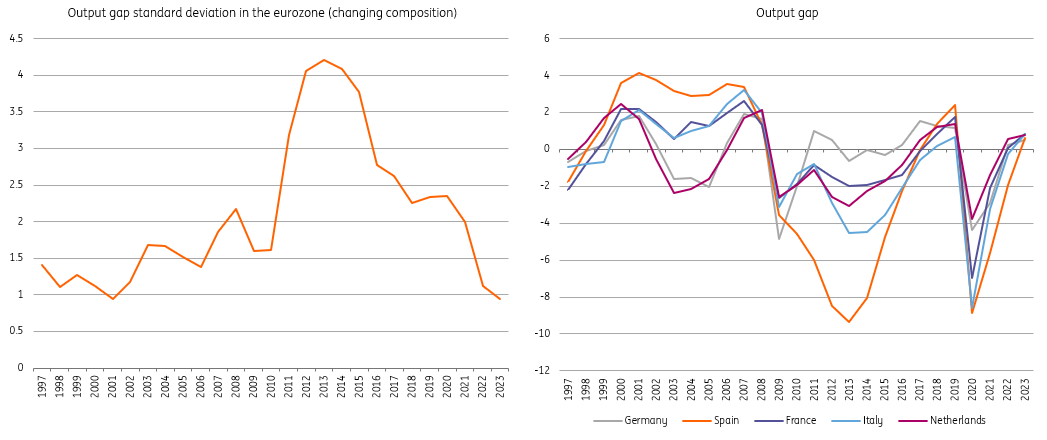

The euro crisis in 2010 started with a common shock - the financial crisis, but soon developed into country-specific shocks. Convergence in the eurozone went into reverse as housing markets imploded in many peripheral countries, leading to divergence both economically and in public finances. At the current juncture, eurozone countries are facing two exogenous shocks and at least one core eurozone country is actually being hit relatively more severely than other countries. There are very few signs of economic divergence.

Economic divergence is small as large countries see output gaps move in tandem

Debt sustainability

Even if economic divergence seems less of an issue now than at the time of the euro crisis, at face value, the public finance picture is less reassuring. The Covid-19 shock, while symmetric in nature, had a nonhomogeneous impact on economic activity in member countries, hitting some countries more heavily than others because of their economic structure and response to the crisis. Southern European countries recorded sharper increases in their deficits and debt compared to most of their core peers. However, unlike a decade ago, structural public accounts remained solid throughout the crisis, with the extra expenditure incurred to limit the shock to the economy being mostly temporary in nature. The political response in the most exposed countries such as Italy and Greece was for a relatively quick return to primary surpluses, telling us that times are different.

Having said that, the prospect of an accelerated normalisation in the ECB’s monetary policy has reawakened old ghosts, putting renewed pressure on spreads and bringing back to the fore doubts about debt sustainability.

For countries burdened by high public debt, sustainability remains an issue, but not one that is currently ringing alarm bells.

In the short run, the combination of long average maturities of debt, decent growth and high unanticipated inflation are all helping to counteract the incremental impact on debt coming from the sharp increase in government interest rates and from residual primary deficits, even in the most indebted countries.

Longer-term, as higher interest rates apply to a growing share of debt and unanticipated inflation is re-absorbed, decelerating real GDP growth would cause debt to snowball again, and primary surpluses would be required to secure a downward trajectory in the debt/GDP ratios. Interestingly, with non-extreme interest rate levels, and decent, but unspectacular growth, the required primary surpluses would be at levels which have already proven to be politically bearable in the recent past. Needless to say, improving long-term real economic growth would be crucial for debt sustainability in the years ahead. This is why the European Recovery and Resilience facility was created, with an allocation of funds more generous for Southern European countries. The battle for debt sustainability will be won more convincingly if the combination of reform and investment, upon which the disbursement of the EU Recovery Fund is conditional, is properly implemented. The six-year time span covered by the plan, for once, provides a comforting medium-term view.

Support for the monetary union has increased significantly in recent years

Another factor which reduces the chances of another debt crisis is that societal support for the euro has increased steadily over recent years. Concerns about the monetary union were widespread during the euro crisis and while scepticism remains widespread, a quiet majority has become happier with it. In Belgium, 85% of respondents are now positive about the euro, while in Italy, more than 70% of those surveyed are positive.

This also translates to politics where the large eurosceptic wave in elections has failed to materialise. While eurosceptic parties still hold a large number of seats in parliaments across the continent and in Brussels, they have not risen to power. Importantly, a pure euro exit platform has mostly been shunned by parties trying to win elections, as this seems to be an unpopular policy among the electorate.

The significant steps taken by politicians and the ECB to fight the coronavirus crisis are a sign that policymakers are more comfortable in acting swiftly in times of crisis. However, if any anti-fragmentation tool comes with strict conditions attached, eurosceptic parties could quickly gain momentum again.

In the end, it’s all about politics, stupid

A better institutional set-up, pan-eurozone financial support and relatively healthier public finances at the start of the pandemic have kept the risk of a new euro crisis relatively low. Despite recent memories of widening bond yield spreads in 2010-2012, the risk of a further escalation looks manageable. However, past experience shows that market speculation can quickly turn into a full-blown crisis and liquidity problems can quickly turn into solvency issues. Worryingly, at the current juncture, the ECB is no longer fighting deflation but inflation. This cannot be done successfully without creating new tension in the bond markets. Therefore, the question of who is the lender of last resort in the eurozone needs to be answered quickly and convincingly. And it is the politicians who must decide. As always, the fate of the monetary union lies in their hands.

Download

Download article

7 July 2022

ING Monthly: Europe’s recovery is cancelled This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more