Why banks aren’t embracing the EU’s Green Bond Standard

- 27 May

- Financial Institutions Sustainability

Banks’ green bond issuance remains robust. But issuance under the European Green Bond Standard, a voluntary EU framework requiring full Taxonomy alignment, is limited due to operational complexity. We expect only gradual growth here, with regulatory revisions providing modest support

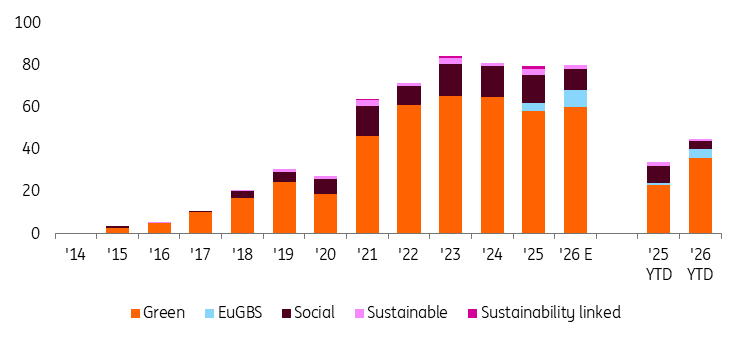

There is little sign that Europe’s simplification drive on ESG regulation is cooling green bond supply. Banks have issued €40bn in green debt instruments year-to-date, up €16bn compared to 2025. Meanwhile, social and sustainability issuance is struggling to push beyond €5bn, running at roughly half last year’s pace.

Despite the pickup in green supply, only 8 banks out of almost 160 sustainable bond issuers have used the EuGBS format since its introduction in 2025.

European Green Bond issuance stands at €4.25bn YTD (11% of total bank green supply). That's up from 2025, when banks issued €4bn of EuGBS bonds (6% of their total green supply).

The limited take-up of issuance under the EuGBS reflects three key constraints.

First, the requirement for full EU Taxonomy alignment raises the compliance bar significantly. Banks issuing under the EuGBS must allocate proceeds to financing economic activities that are aligned with the EU Taxonomy. In practice, this requires compliance with the Taxonomy’s technical screening criteria (TSC) for substantial contribution, do-no-significant-harm (DNSH) and minimum safeguards.

This sets a higher bar than the ICMA Green Bond Principles. While proceeds are typically aligned with the Taxonomy’s substantial contribution criteria, compliance with DNSH requirements and minimum safeguards is usually achieved only on a best-efforts basis.

Second, issuers face constraints from the design of the framework and evolving rules. To date, banks that have issued EuGBs have only used the portfolio approach and not the gradual approach. If the Taxonomy’s TSC and DNSH provisions are amended ahead of maturity, issuers using a portfolio approach must align their green assets with any of the TSC applicable during the seven years prior to the publication of the allocation report.

As such, assets that no longer meet the new TSC can remain part of the green portfolio for up to seven years. The current review of the EU Taxonomy’s technical screening criteria may therefore have prompted some banks to delay issuance under the standard.

Third, the EuGBS introduces additional operational and reporting requirements. While not a major constraint, the EuGBS also places stricter transparency obligations on issuers, including a (pre-issuance) green bond factsheet and (post-issuance) allocation and impact reports, with the former to be reviewed by an independent registered external reviewer.

EuGBs predominantly refinance green mortgage loans

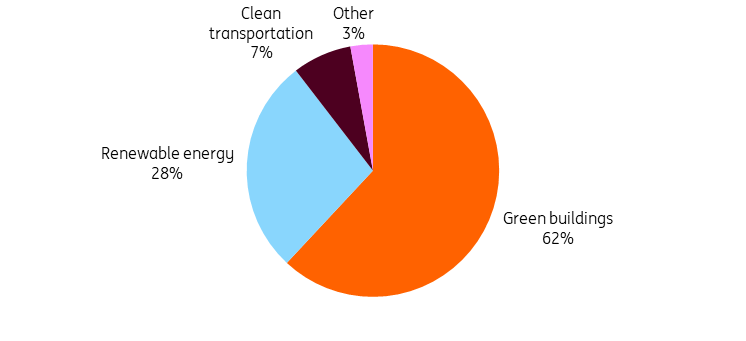

Banks issuing under the EuGBS have so far exclusively dedicated proceeds to refinancing portfolios aligned with the EU Taxonomy’s climate change mitigation objective. EU green bond proceeds are mainly directed towards renewable energy and construction and real estate activities. Within this, acquisition and ownership of buildings is the dominant underlying activity, for several reasons.

Renewable energy and green buildings are the main Taxonomy activities financed by bank EuGBs

Mortgage loans are a dominant loan category on bank balance sheets for assessing Taxonomy alignment. Under the acquisition & ownership of buildings criteria, the DNSH assessment is limited to climate change adaptation, while retail exposures are exempt from minimum safeguards verification. Residential mortgage portfolios are typically composed of properties below 5000m2, meaning additional criteria regarding air-tightness and thermal integrity testing, or life-cycle Global Warming Potential (GWP) calculations, are also not applicable.

Banks often use assets reported within the scope of the Green Asset Ratio (GAR) for their green asset selection. The Omnibus I package limits Corporate Sustainability Reporting Directive and Taxonomy disclosures to companies with more than 1,000 employees and more than €450m in turnover, reducing the incentive for smaller banks to gather such data in support of green issuance.

The reduced disclosure scope also limits banks’ access to information on the Taxonomy alignment of small corporates. Furthermore, the Taxonomy Simplification Delegated Act introduces a 10% materiality threshold, allowing banks to exclude smaller exposures from the Taxonomy alignment assessment. In practice, this leaves mortgage lending as the primary, and often only, asset class to include in the green portfolio.

Renewable energy projects, the second most important use of proceeds category for green bond issuance, are also often outside the CSRD and GAR disclosures scope. Renewable energy projects are not eligible for the GAR denominator if they are financed through Special Purpose Vehicles.

Use of proceeds of European bank green unsecured bonds

(incl. non-EuGBs)

Banks often have global asset portfolios. It is difficult for non-EU-located assets to comply with the do-no-significant-harm criteria, given that these are often based on EU legislation. This is particularly relevant where the DNSH requirements reference EU standards, such as those governing the technical specifications for water appliances. For new constructions or renovations, for example, these standards are intended to ensure no significant harm is done to the sustainable use and protection of water and marine resources.

Moreover, for global mortgage loan portfolios, green building certification schemes such as BREEAM or LEED are not eligible as a substantial contribution criterion under the EU Taxonomy. This makes it difficult to assess Taxonomy alignment for international real estate assets. For buildings constructed before the end of 2020, it may be possible to use the top 15% analysis, but for buildings constructed thereafter, the nearly zero-energy building (NZEB) -10% reference is not applicable abroad (this is an EU concept).

So, for many banks, it just makes more sense to issue a standard ICMA-aligned use-of-proceeds green bond, where, according to best market practice, they report the percentage of EU Taxonomy alignment of the portfolio.

Banks less constrained by these challenges are, in our view, likely to increasingly shift their green issuance towards the EuGBS. Covered bonds backed by EU mortgage portfolios are well-positioned in this respect. The upcoming revisions to the Taxonomy’s technical screening criteria may also offer a modest boost to EuGBS supply.

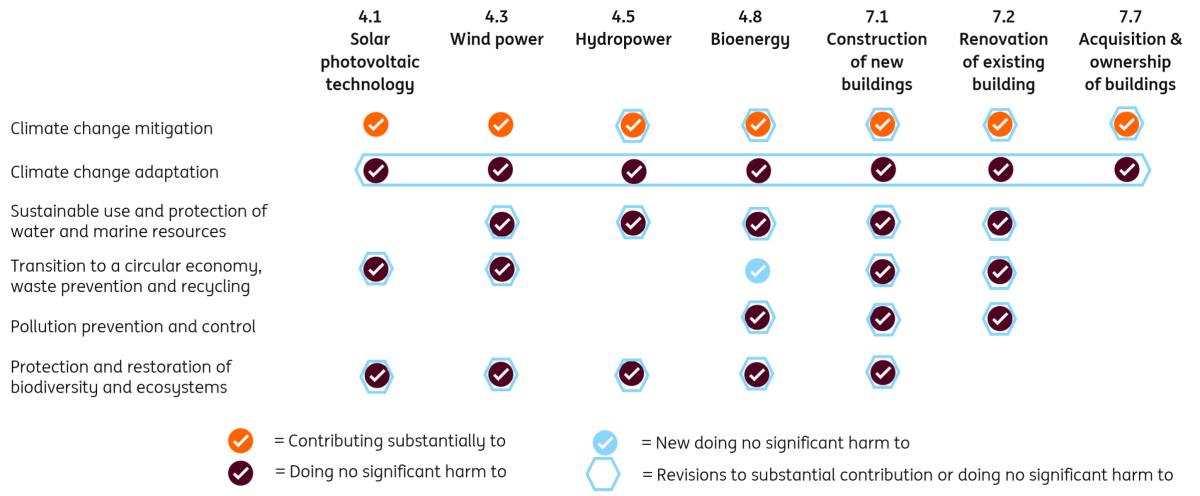

Revisions to the technical screening criteria

On 17 March 2026, the European Commission published draft revisions to the EU Taxonomy’s technical screening criteria for public feedback by 14 April. Most of the relevant substantial contribution and DNSH criteria for renewable energy and building activities are under revision.

Substantial contribution and DNSH criteria under review

The majority of the EuGBs that have been issued to date expire within seven years. As such, the proposed TSC amendments should not have much impact on the eligibility of green loan portfolios currently refinanced by these bonds.

For banks, the most important substantial contribution criteria for buildings constructed before 2027 will also remain broadly unchanged and are even expanded to include buildings with a primary energy demand reduction of at least 60%.

Combined with the streamlining of the DNSH criteria, this should support the expansion of Taxonomy-aligned green portfolios.

Proposed revisions to the Taxonomy criteria for buildings

Substantial contribution criteria

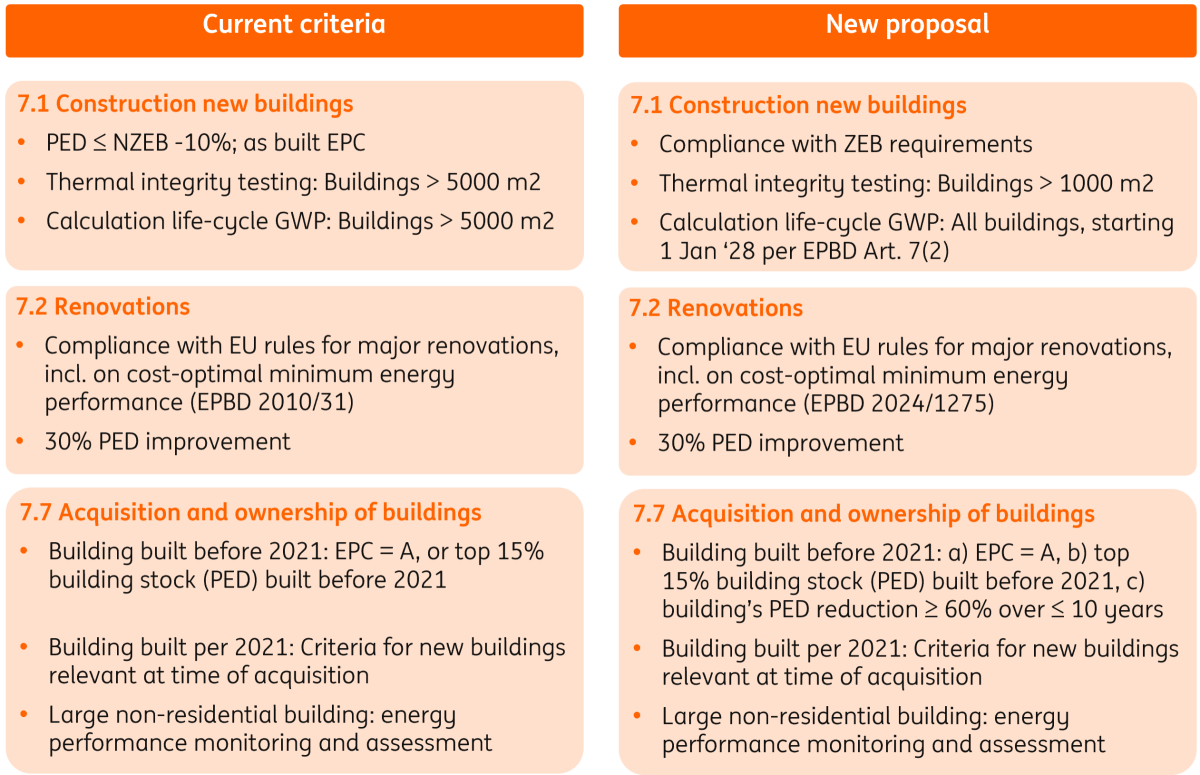

For newly constructed buildings, the substantial contribution criteria to climate change mitigation will be aligned more closely with the revised European Energy Performance of Buildings Directive (EPBD 2024/1275), which must be transposed into national law by 29 May 2026. As the Taxonomy’s revised technical screening criteria are set to enter into force on 1 January 2027, Taxonomy alignment will already be assessed against EPBD-based metrics before these become fully mandatory under the EPBD.

Under the TSC proposals, newly constructed buildings must meet zero-emission building (ZEB) requirements. This replaces the current criterion that primary energy demand (PED) must be at least 10% below nearly zero-energy building (NZEB) levels. This brings the Taxonomy requirements in line with the EBPD, under which all new buildings must be ZEB from 1 January 2030, with the maximum energy demand threshold for ZEB set at levels at least 10% below the NZEB benchmark of 28 May 2024.

In the absence of robust quality controls during construction, air-tightness and thermal integrity testing will apply to new buildings larger than 1000m2 (down from 5000m2). Life-cycle global warming potential (GWP) calculations will extend to all buildings (from ≥5000m2 buildings). EPBD 2024/1275 will be the reference for these calculations from 1 January 2028. Under the EPBD, life-cycle GWP calculations become mandatory from 2028 for new buildings above 1000m2, and from 2030 for all new buildings.

The substantial contribution criteria for renovations remain broadly unchanged except that EPBD 2024/1275 becomes the reference for major renovation rules, including cost-optimal minimum energy performance requirements. The alternative 30% reduction requirement in primary energy demand remains intact.

For buildings constructed before the end of 2020, the acquisition and ownership criteria continue to include the EPC label A and the top 15% primary energy demand threshold. These criteria are expanded to include buildings with a primary energy demand reduction of at least 60% over 10 years or less, enabling more frequent recognition of whole loan volumes for renovated buildings compared to the 30% PED reduction rule.

For buildings constructed after 31 December 2020, Taxonomy alignment is assessed against the criteria for new buildings applicable at the time of acquisition. This will be the NZEB-10% criterion until the proposed revisions enter into force on 1 January 2027, and the ZEB criterion thereafter.

Changes to the technical screening criteria for substantial contribution for buildings

Do no significant harm criteria

The do no significant harm criteria are also simplified, with those centred on adaptation for climate change being most relevant, as they apply to all construction and real estate activities. Current requirements include a climate risk and vulnerability assessment (CRVA) to identify physical climate risks, alongside adaptation solutions where these are material. The proposed changes streamline this into four steps: screening, climate risk assessment, adaptation planning and implementation.

References to “material physical climate risks” are replaced with “significant climate-related hazards”, while the CRVA is simplified to a climate risk assessment based on observed and projected data (for activities with a lifespan of less than 10 years only if available and actionable).

The language around adaptation plans is softened, requiring identified significant risks and potential solutions to be assessed and explained based on available technologies, costs and benefits, without increasing adverse impacts “to the best knowledge available”.

At the same time, the DNSH criteria for transition to a circular economy are becoming slightly stricter, with recycling requirements for non-hazardous construction and demolition waste raised to 85% from 70%. These DNSH criteria apply to both the construction of new buildings and the renovation of existing ones.

Taxonomy complexities to keep EuGBS issuance in check

Issuance under the EuGBS is likely to remain limited in the near term, reflecting the additional complexities of achieving Taxonomy alignment compared with standard use-of-proceeds issuance. While the proposed revisions to the technical screening criteria and the simplification of DNSH requirements are supportive, they are unlikely to materially shift issuance dynamics. A gradual increase in EuGBS adoption is more likely, led by banks with sufficiently large EU-based and Taxonomy-aligned asset pools.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more