WASDE update: A largely bearish affair

- 12 April 2024

- Commodities, Food & Agri

Grain markets sold off yesterday after what was seen as a fairly disappointing WASDE release from the USDA. The market had expected the USDA to revise lower some South American output numbers, but these revisions were largely absent

South American corn crop revisions largely absent

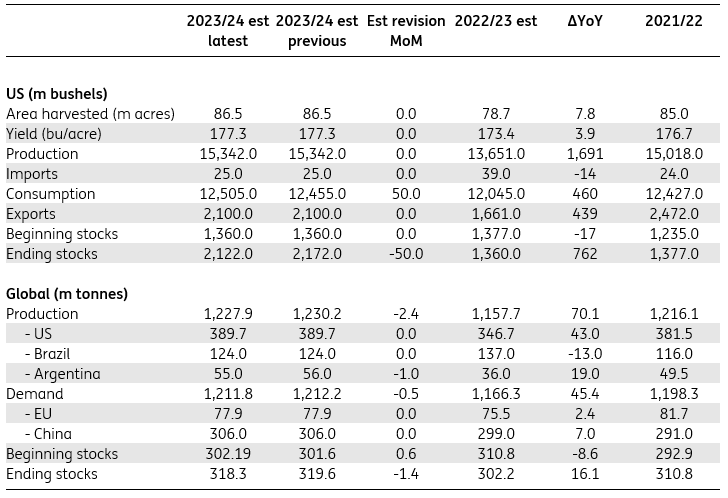

There were few changes to the USDA’s US corn balance, with 2023/24 ending stocks lowered marginally from 2.17bn bushels to 2.12bn bushels. This revision was driven by a 50m bushel revision higher in domestic consumption and specifically for ethanol, feed, and residual use. This leaves US corn stocks slightly above market expectations of around 2.1bn bushels.

As for the global corn market, the USDA lowered ending stock estimates by 1.4mt to 318.3mt due to slightly lower supplies from South Africa (-1.5mt), Argentina (-1mt), Mexico (-0.7mt), and Moldova. The market was expecting a revision lower in Brazilian corn output due to drier weather conditions but this did not happen. As a result, even though stocks were lowered they still came in above market expectations of a little under 317mt. Global corn consumption saw some marginal revisions lower.

Overall, the corn numbers were bearish with the market expecting a downgrade in Brazilian production. The USDA is still pegging Brazilian output at 124mt, well above the 111mt that CONAB, Brazil’s agricultural agency, is forecasting.

Corn supply/demand balance

Brazilian soybean output surprisingly left unchanged

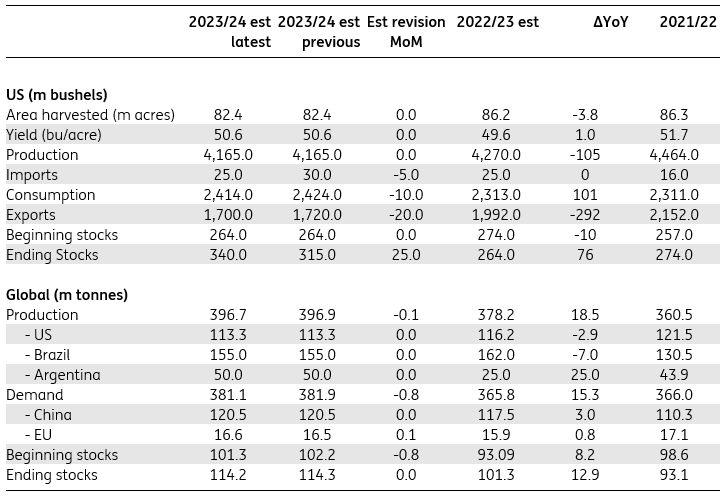

The USDA increased its 2023/24 US ending stock estimates for soybean, from 315m bushels to 340m bushels due to a fall in consumption and exports. The market was expecting a stocks number closer to 319m bushels. Despite this more bearish than expected number, soybean did not sell off as aggressively as corn and wheat, as one may have expected.

The global balance sheet would have disappointed as well. The market was expecting the USDA to also revise lower Brazilian soybean output, but this was left unchanged at 155mt. This means that global ending stocks were left largely unchanged at 114.2mt, and above market expectations.

Similar to corn, there is also growing divergence between Brazilian soybean production estimates. While the USDA has stuck to its estimate for 155mt in 2023/24, CONAB has lowered its output estimate to 146.5mt.

Soybean supply/demand balance

Global wheat balance largely unchanged

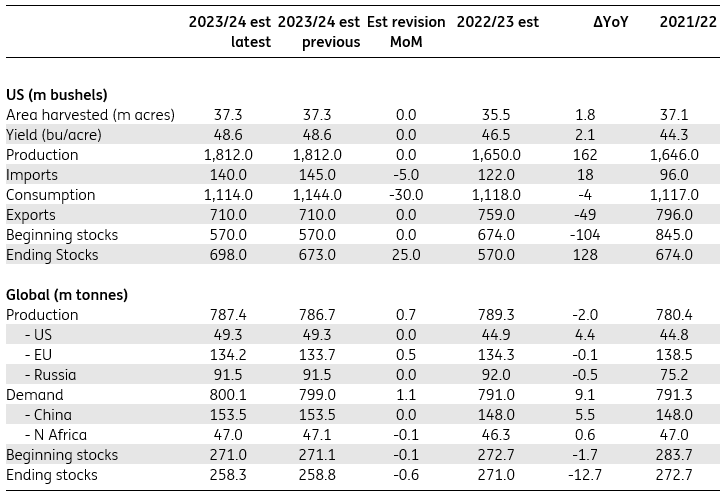

The USDA increased its 2023/24 US wheat ending stocks estimate from 673m bushels to 698m bushels following a drop in domestic use. This also meant that stocks came in above market expectations of around 691m bushels.

The global balance saw ending stock estimates marginally cut from 258.8mt to 258.3mt for 2023/24, below market expectations. Clearly the reaction we saw in wheat prices was driven more by changes in the US balance rather than the global balance.

Wheat supply/demand balance

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more