USD/JPY: Largest quarterly intervention since 2004

- 29 May

- FX

The Japanese Ministry of Finance has today released FX intervention figures for the period of 28 April to 27 May. It confirms that the Bank of Japan sold JPY11.735tr (around $74bn). This will mark the largest quarterly FX intervention since 2004. It's an impressive figure, but unless oil or US rates turn dramatically lower, USD/JPY will stay bid

Sizable intervention

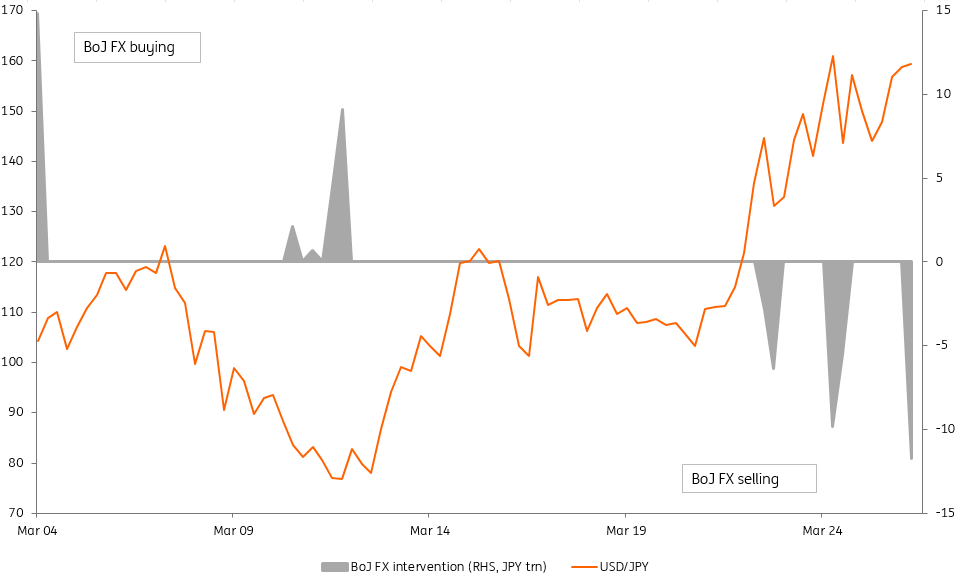

Figures released by Japan’s MoF earlier today confirm that the BoJ undertook JPY11.735tr of FX intervention in the 28 April to 27 May window. That intervention likely started on 30 April, driving USD/JPY from above 160 to below 156 and was followed up potentially over the next four trading sessions.

The size confirmed today is large. In fact, looking at the quarterly intervention figures, one has to go back to 2004 to see any activity as large in a single quarter.

Back in early 2004, the BoJ was intervening almost daily in an effort to keep USD/JPY above 100 at a time of a prevailing dollar bear trend – this after the Federal Reserve had cut its policy rate to 1.00% after the dot-com bubble burst.

Since then, FX intervention has been more modest and less frequent.

In fact, there is some speculation that Japanese policymakers feel constrained by the IMF’s FX regime classification system. More frequent intervention – beyond three ‘instances’ in a six-month period – could see Japan’’s FX regime re-classified as ‘floating’ instead of ‘free floating’ – which would be more in line with regimes in Brazil and Chile than Japan’s G7 peers.

BoJ FX intervention versus USD/JPY

Policymakers will struggle to turn the tide

With USD/JPY already trading back near 160, it is hard to make the case that this year’s Japanese FX intervention has been effective. Back in 2024, FX intervention was a success because the speculative market was heavily short yen and US rates were turning lower ahead of a Fed easing cycle starting that September.

Today, the speculative market is far less short yen and if anything, the Fed could be swinging behind a hike for its next move rather than a cut. Our call is that the BoJ will likely be called into action again over coming months as USD/JPY pushes through 160 again. This also has implications for US Treasuries, as Japanese authorities appear to sell Treasuries to finance FX intervention. Japanese holdings of US Treasuries fell around $100bn in 2024 – roughly consistent with FX intervention amounts that year. Remember as well that FX selling operations are finite and limited by the size of FX reserves. Japan has large reserves at over USD1tr, but will not want to lose 20-30% of them.

Unless the BoJ can somehow get ‘ahead of the curve’ and drive real interest rates higher, it is hard to see the USD/JPY situation changing over coming months. ING is looking for a BoJ rate hike on 16 June (now priced with a 78% probability), but the BoJ will have to deliver a very hawkish hike to reverse the recent shift in real interest rate differentials against the yen. That would somehow require the BoJ to manage expectations of a policy rate (now 0.75%) heading above 1.50% next year – which might be difficult in the current political environment.

Until then, we expect USD/JPY to stay bid near 160 over coming months and possibly push into the 162/163 area. Our call for 155 by year-end very much relies on US consumption stalling and the Fed reconsidering rate cuts. That is increasingly looking like a story for later in the year and the near term focus will be on the growing Fed hawkishness.

Real interest rates keep USD/JPY supported

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more