US Treasury FX report preview: Three and a half manipulators

The Treasury is delaying its currency manipulation report, possibly on the back of new tensions with China - which might be labelled again despite not meeting the criteria. We estimate that Vietnam, Taiwan and Thailand all exceed the thresholds, while Switzerland is dangerously close. However, we don’t exclude some “free passes” being granted

US Treasury manipulation report: another suspicious delay

The US Treasury publishes a report to Congress twice a year in which macroeconomic and exchange rate policies of key trading partners are examined in detail. The aim is to identify countries that artificially manipulate their currencies to gain a competitive advantage to the detriment of the US.

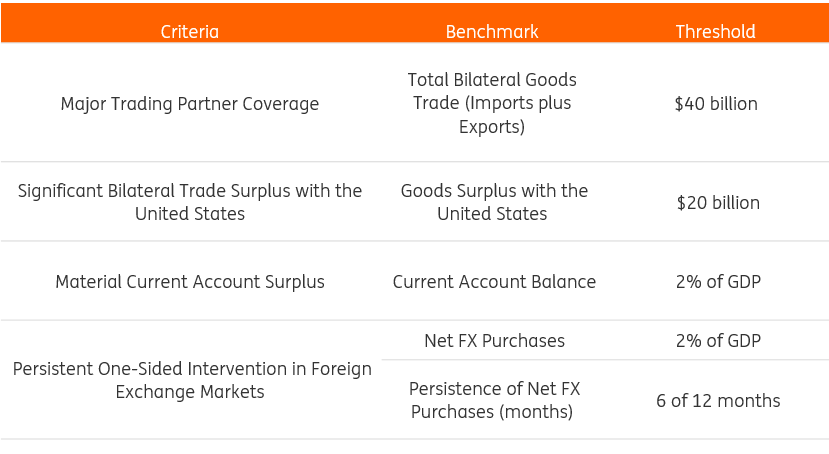

In order to designate a country with the manipulator tag, the Treasury provides that three criteria must be met, along with the related quantitative thresholds (Figure 1). Countries that only meet two criteria are put in a “monitoring list” that merely implies further scrutiny.

Figure 1 - US Treasury criteria

The only country to receive the manipulator tag in the past 20 years was China – despite not meeting the quantitative criteria - in August 2019, as trade tensions with the US escalated and USD/CNY breached the 7.00 mark. The tag was lifted as part of the Phase One trade deal in January 2020.

Here’s our commentary on the January 2020 report

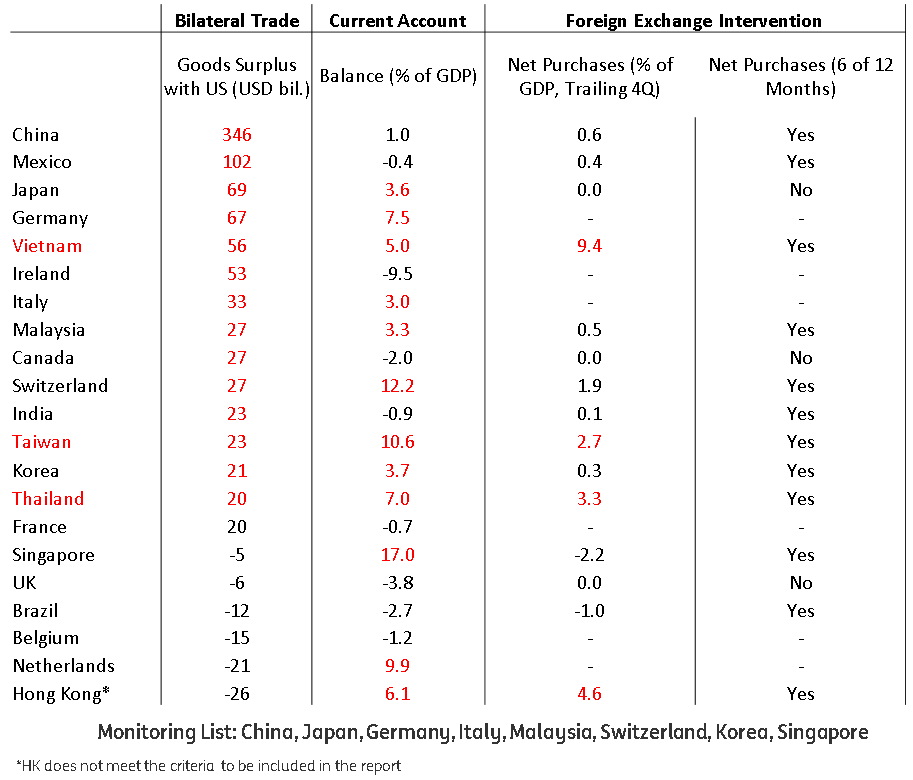

The new US Treasury report was originally expected to be published in May, covering data for the period 1Q-4Q 2019. We estimated the evaluation criteria for each country in the report and found that three countries exceed all thresholds: Vietnam, Thailand and Taiwan. A fourth one, Switzerland, meets all of the criteria but one – the size of intervention – which is however very close to the threshold.

Our estimates

Figure 2 shows our estimates of the US Treasury criteria for the period 1Q-4Q 2019. Data for the goods trade balance with the US is provided by the US census, the current account and official reserves by the IMF and GDP figures by Bloomberg.

The Treasury also uses staff and external estimates that add a degree of discretion, in particular when it comes to gauging FX intervention. We had previously attempted to account for a valuation effect when looking at the variation in FX reserves to measure FX intervention. We have found that the simple change in reserves over the 12 months in consideration provides a closer estimate to the UST figures.

Fig 2 - ING estimates on US Treasury criteria

China: Below the thresholds, but another label may be on the way

China has been the central topic in the recent editions of the Treasury report and the recent resurgence in geopolitical tensions with the US suggests it will take centre stage in the forthcoming edition too. According to our estimates, China only met one of the three criteria in the period under review. But this was also the case in August when the UST designated China a manipulator, suggesting that this won't necessarily protect the country from being labelled again.

The delay in the publication of this edition of the report may be a consequence of some indecision on whether to tag China a manipulator. If this is the case, there is a high chance that the report will not be published before the US-China diplomatic spat takes a clearer direction.

The yuan is currently trading at around 7.11 vs the USD, well above the 7.00 level that triggered the Treasury reaction in August. At the same time, the yuan has partly re-appreciated after hitting 7.17 last week as markets became less concerned about trade tensions.

In August, the impact of the manipulator label was rather limited. This is because the designation simply provides for a period of talks with the country’s monetary authorities and if negotiations fail, actions such as tariffs can be taken: at that time, tariffs were already in place. Now, after the Phase One deal lifted part of the US tariffs on Chinese exports, the market implications may be more significant, as it could be read by investors as a move by the US to convert the diplomatic spat into a new trade war. Should such a move occur in the current environment, where markets retain a rather complacent approach to US-China tensions, the impact could be magnified.

Vietnam, Taiwan and Thailand meet all criteria…

Vietnam was another focus of attention in previous editions as the central bank had been rather active in building FX reserves, heightening the risk of the country receiving the manipulator label. In January, despite a significant increase in FX reserves in 2Q18-2Q19, the Treasury reported that “Vietnamese authorities have credibly conveyed to Treasury that net purchases of foreign exchange were 0.8% of GDP”. Our estimates were at 2.8%.

At that time, Vietnam would have been saved in any event by the current account staying below the 2% of GDP threshold. Data from the Vietnamese central bank (State Bank of Vietnam) shows, however, that the country’s current account spiked in 2H19 (Figure 3). Our estimates show that this brought the current account surplus for 2019 to 5% of GDP, well above the UST threshold (2%).

FX reserves also increased significantly in 2H19, and the variation over the entire year was around 9.4% of GDP. We overestimated the FX intervention in the previous report, but it will surely be hard for Vietnam to prove that less than 2% of the approximate 9% increase in reserves (all in % of GDP terms) should be considered as FX intervention.

Taiwan has also met all three criteria, according to our estimates. The country already presented a large current account surplus to the world but also saw a jump in goods exports to the US (meeting the first quantitative criteria) as well as in FX reserves. We estimate FX intervention at around 2.7% in 2019, with the country having made net purchases for at least six months (like Vietnam and Thailand). In January, the Treasury had shown concerns over the possibility of Taiwan using FX swaps to intervene in the FX market, after an October 2019 analysis by the Council for Foreign Relations suggested a “shadowing” of around USD130 billion in intervention, as the country does not report its derivative positions. Taiwan denied such allegations.

Thailand only met the current account criteria in the January report, but was close to hitting the other two. US census data shows that goods exports in 2019 were just above the USD 20 billion mark and we estimate the variation in FX reserves amounted to 3.3% of GDP.

Fig 3 & 4 - Vietnam reserves, C/A and currency dynamics

… but may get a free pass

In recent times, the US Treasury report has taken on very strong political overtones. The Treasury “bending” the three criteria rule in labelling China (which only met one condition) a currency manipulator was a case in point.

In times when tensions with China are high, it is fair to assume that the decision to designate a country a manipulator will first be filtered through an assessment of any geopolitical implications. The three countries that have hit the thresholds, according to our estimates, are all in a geographical position that connects them with China.

Vietnam is often identified as the key alternative to China as a hub for US companies’ supply chains. A recent media report indicated that Apple shifted 30% of AirPods production from China to Vietnam. If the US continues with plans to loosen its economic ties to China, designating Vietnam a manipulator may be self-defeating. On the currency side, the dong (figure 4) has recently appreciated after the initial pandemic shock, which may suggest less FX intervention is being carried out.

In the case of Taiwan, reasons to give a “free pass” are mostly political. As China attempts to tighten its control over Hong Kong, Taiwan represents an important ally of the US as the island has shown increasing aversion towards the One-China policy. From an economic standpoint, TSMC (world leader in semiconductors, based in Taiwan) has announced a plan to build a chip plant in the US, which is also seen as a move to reduce US dependency on Asia. The manipulator tag may create unwanted frictions in the company’s plans.

Thailand may be the least likely to get a free pass as the country has a smaller role from a political point of view. However, the Thai central bank has recently eased back on currency intervention and the Thai baht has been the second best performing Asian currency since the start of May (+2.5% vs USD). Incidentally, the large current account surplus has likely contracted quite significantly in the past few months as a result of the pandemic.

As a general consideration, we suspect that the UST will be reluctant to designate any of the three countries a manipulator while sparing China the same label. At least as long as the current administration intends to use the manipulation report as a geopolitical tool.

Rest of the world: Switzerland is dangerously close, HK might join monitoring list

Some eurozone countries have long been on the monitoring list, but the lack of FX intervention by the European Central Bank makes it impossible to meet the third criterion. Germany and Italy are set to remain on the monitoring list in the next report, but Ireland should be removed as it failed to meet at least two criteria for two consecutive reports.

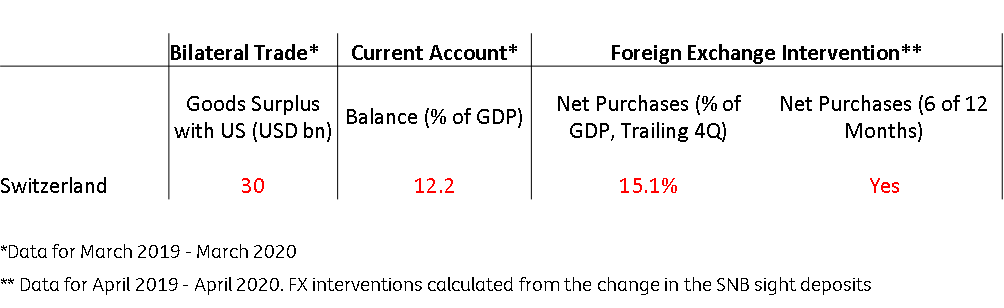

Switzerland, instead, is dangerously close to hitting all thresholds. The large current account surplus is not news and goods exports to the US increased to USD 27bn (in 2019). However, the Treasury tends to “trust” the amount of FX intervention published by the Swiss central bank (SNB) in its annual report (page 14): in 2019, CHF 13.2bn of FX purchases were reported. For consistency purposes, we have only used GDP data in USD and therefore converted the amount of FX purchases in USD, using the average exchange rate in 2019 (almost at parity, 1.007). The result is FX intervention amounting 1.9% of GDP.

With the threshold set at 2%, and some discretion on what GDP and exchange rate to use, we cannot fully exclude that Switzerland will already meet the thresholds in the forthcoming report. What may also play a role is how Switzerland engaged in very large FX intervention in the first few months of 2020 to counter the Swiss franc's appreciation. We estimated (in the article: “EUR/CHF: The case for parity”) those interventions to have been approximately 15% of GDP through April 2020 (figure 5), which makes it virtually impossible for Switzerland to avoid hitting the 2% threshold in the Autumn report, which will cover the period 2Q19-2Q20. This may build some additional speculative interest in CHF longs to bet on a softer stance by the SNB, which may let CHF appreciate more freely.

Fig 5 - Switzerland is well above the thresholds in 2020

Elsewhere, Malaysia and South Korea met the first two criteria but we did not find enough evidence that the two countries exceeded the thresholds for FX intervention. They should simply remain on the monitoring list. Singapore will also remain on this list because while it no longer meets the FX intervention criteria, it will need to do so for another report before being removed. Japan is also set to remain on the list though there is no chance of it being labelled a manipulator, as the Bank of Japan is not currently engaging in FX interventions.

Hong Kong has not been included in the latest report as it did not meet the very first requirement: total trade in goods with the US exceeding USD 40 bn. In 2019, this was still the case, as the US census reported it to be at USD 35 bn. If the UST decides to include HK in the report anyway, the country may well be put onto the monitoring list due to its large current account surplus and large currency intervention. However, it must be noted that HK has a deficit (a very large one too: USD 26 bn) in goods trade with the US, so there is no possibility it will hit all three thresholds.

The decision to put HK on the monitoring list has no tangible implications, but may well resonate loudly in the markets after President Trump announced plans to remove Hong Kong's preferential trade status.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

3 June 2020

The Covid-19 crisis: Finally, some good news This bundle contains 9 Articles