US Treasury FX Report: It’s political

- 15 January 2020

- FX

With a three-month delay, the US Treasury FX Report has been released. As expected, China's manipulator label was lifted and the attention may now shift to Europe and Germany's large surplus. In Asia, the recent drop in global FX intervention volumes will be challenged by the next dollar downturn

The US Treasury FX Report to Congress has always been a political document and never so much as now, given the US-China trade dispute. The removal of the currency manipulator designation from China confirms the rapprochement in US-China relations. Attention now turns to: i) does Washington go to work on Europe’s trade surplus with the US and ii) will Asian nations really step away from FX intervention if the dollar one day turns decisively lower?

China’s ‘manipulator’ designation removed

The US Treasury released its semi-annual FX report to Congress, which you can read here. This had been due around 15 October, but because of ongoing US-China trade negotiations has been released just a few days before the signing of the 'phase one' trade deal – due to take place in Washington today.

Washington designated China a currency manipulator last August after the People's Bank of China allowed USD/CNY to trade above 7.00 – an act that was deemed a deliberate de-valuation by US authorities. That was at the height of the trade conflict. Even though it did not prompt any additional trade sanctions per se, it signified the low-point in US-China trade relations.

The subsequent delay in the release of the FX report and the decision on Monday to remove the manipulator label also represents a significant rapprochement in US-China trade relations. We have not yet seen exactly what China has offered Washington in terms of new FX practices, but it is expected to be along the lines of what we discussed in October and very similar to the commitments made in the forthcoming USMCA agreement.

That means a commitment to ‘avoid manipulating exchange rates or preventing effective balance of payments adjustment for trade gains’ and more transparent reporting of FX intervention. This latter part is critical and controversial. China may see the demand for FX intervention data as an infringement on its sovereignty. However, Korea acceded to similar demands last year and now publishes FX intervention data every six months – with a three-month lag. Let’s see whether China commits to a similar level of transparency in intervention activity.

Apart from registering the improvement in US-China relations, this report and any Chinese FX commitment suggests that it will be much more difficult to deliver a repeat of the massive FX intervention seen between 2005 and 2014, which effectively prevented more substantial renminbi strength and the effective balance of payments adjustment.

Europe: In Washington’s cross hairs?

A less volatile situation in the trade relationship with China may shift attention to Europe. The Treasury continues to allocate ample parts of its report to assessing the imbalanced trading relationship with key European partners, never failing to stress its unease about the stubbornly weak euro. As of its latest update, the monitoring list (populated by those countries meeting two of the three criteria) includes three eurozone members: Germany, Italy and Ireland.

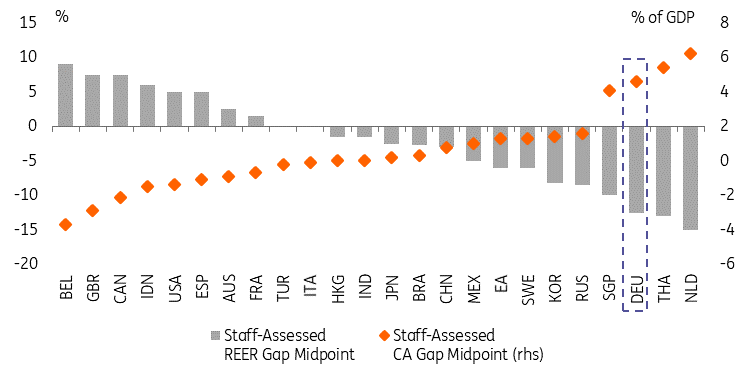

Unsurprisingly, it’s mostly Germany on trial. The Treasury brings two key pieces of data by the IMF as evidence: a) in 2018, Germany’s external position was still found “substantially stronger than implied by fundamentals”; b) Germany’s real effective rate was undervalued by 8-18% (“2019 External Sector Report”, Figure 1).

Figure 1 - IMF highlights Germany's trade advantage

Unlike China, currency weakness in the eurozone is not a consequence of central bank intervention, but largely a function of the macroeconomic policies within the euro area. Accordingly, US officials have been stressing the need for fiscal stimulus in Germany to revive spending and reduce the high savings rate. This would inevitably help to mitigate current account imbalances and, in tandem, likely strengthen the euro.

In the face of a lack of appetite for fiscal spending in Germany, the question is what the US can do. Our trade team has recently expressed the view (see: “Trade: a very bleak recovery in 2020”) that a persistent tough stance on trade by President Trump should mostly be channelled through words rather than action. However, they also highlight the non-negligible risk of a further escalation in global trade tensions, with the EU being among the victims this time round.

Pressure from US tariffs pushed the Chinese government to step up fiscal stimulus and President Trump may hope to replicate such results in Germany through similar means. With the Presidential election on the horizon, it may look like a bold move to hit the EU with protectionist measures, but it must also be noted that the electoral debate has not seen trade as a particularly central topic so far.

Vietnam is safe, Switzerland in the spotlight

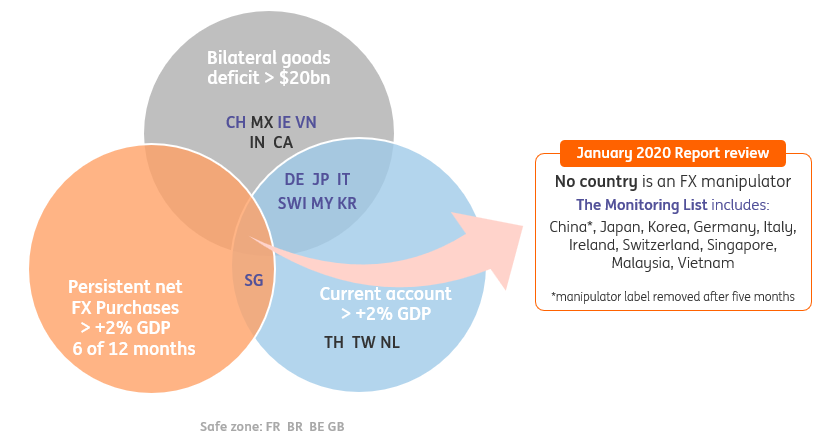

Figure 2 provides an overview of the key findings of the Treasury report (which refers to data spanning from June 2018 to June 2019).

Figure 2 - FX Report overview: no country is an FX manipulator

In past publications on this subject, we have highlighted the risk of Vietnam receiving the currency manipulator label. Updated current account data helped to avert this outcome before the report was published yesterday, but we were surprised to see the country undershooting the FX intervention threshold. In our estimates (calculated as the valuation-adjusted variation in FX reserves), net purchases amounted to 2.6% of GDP, while the Treasury only reports 0.8%. Interestingly, the document specifies that this number did not result from Treasury’s staff calculations or public disclosure (like for the other countries), but states: “The Vietnamese authorities have credibly conveyed to Treasury” the amount of FX purchases.

Also interestingly, the report seems to downplay the issue of transhipment through Vietnam from China to avoid US tariffs, and the government seems satisfied with the ongoing efforts of the Vietnamese government to counter trade fraud. Such an accommodative stance towards Vietnam perhaps suggests the US government has little appetite to further disrupt the Asian supply chains of US companies.

Looking at the other countries in the report, Switzerland is an interesting one. Meeting both the “bilateral trade” and “current account” criteria, currency interventions by the Swiss National Bank – more likely, after the recent Swiss franc rally – may warrant the manipulator label. Some clarifications are, however, necessary.

- First, the FX purchases currently amount to $3 billion, or 0.5% of GDP: meeting the 2% threshold would imply a considerable $12 billion of net purchases in a year.

- Second, the Treasury requires that net purchases occur for at least six of the 12 months covered in the report: a one-off intervention may not imply further buying for five more months.

- Third, a possible manipulator label would not happen until October 2020, when the report covering June 2019 – June 2020 is released and when the global trade situation may well be radically different.

Untested symmetry

No countries, except Singapore, have engaged in enough FX interventions to meet the qualitative and quantitative thresholds set by the Treasury. This denotes a global downtrend of central bank activism in the exchange rate market.

One of the key points we took from the report was a remark from the US Treasury questioning whether the recent decline in global FX intervention would be symmetrical. It has not been a surprise that FX intervention has declined during a period of dollar strength – i.e. orderly FX weakness has been welcomed in a world of secular stagnation.

The question is what happens to FX intervention if and when a genuine dollar bear trend develops. In theory, this tougher stance from the US Treasury is an investment in the future – making FX intervention (typically from Asian FX nations) more transparent and more difficult. Only time will tell if that is the case.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more