EUR/CHF: The case for parity

- 22 May 2020

- FX Switzerland

A view is growing that the 1.05 level in EUR/CHF is some kind of new FX floor for the Swiss central bank to defend. We see three reasons why this perceived floor may crumble: i) the inflation-adjusted CHF index is not particularly strong, ii) the SNB will struggle to match ECB printing presses this year, and iii) Washington is keeping a close eye on intervention

Intervention picks up, is 1.05 the new 1.20?

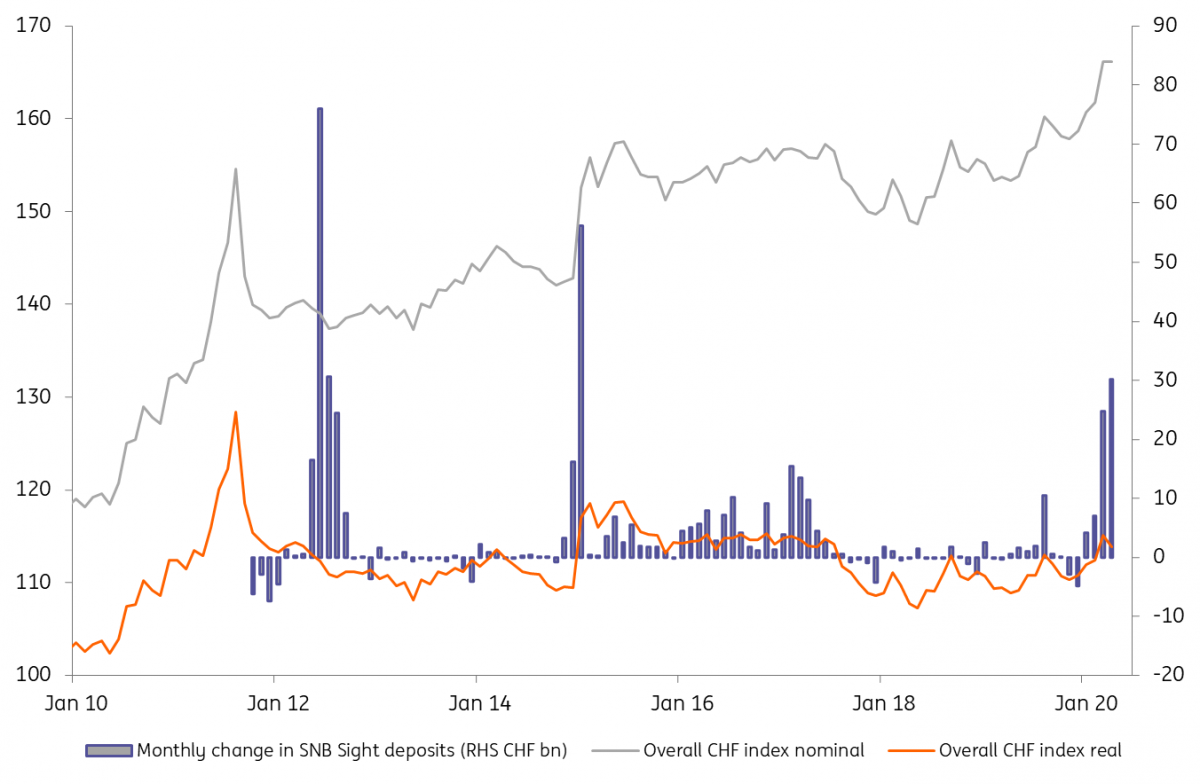

As has been widely reported by the analyst community and acknowledged by the Swiss central bank, FX intervention to limit CHF strength has picked up markedly since Covid-19 went global in March.

Negative rates and FX intervention remain the central bank's core tools of monetary policy and with the policy rate already at -0.75%, the intervention has had to do the heavy lifting. While not being a perfect indicator of the size of FX intervention, the change in total CHF sight deposits suggests the SNB may have spent as much as CHF80bn in trying to limit CHF strength this year. Operationally this means buying EUR/CHF.

Presumed FX intervention from late March onwards has led to much speculation over whether the 1.05 level in EUR/CHF is a new floor akin to the 1.20 level the SNB defended between 2011 and 2015. That would mark a change from the strategy the SNB has seemingly pursued since 2018, which we would more describe as a tolerated appreciation of the CHF.

The SNB themselves have said that they are not targeting any specific level on EUR/CHF and their intervention style since the trade war broke in 2018 (and sent EUR/CHF tumbling) has been to allow EUR/CHF lower in fits and starts. We would also note that while safe-haven demand has pushed the nominal trade-weighted CHF to new highs, Switzerland’s borderline deflation has kept the real trade-weighted CHF much lower. For reference, this real measure is still trading some 4% below levels seen in summer 2015, suggesting that if the SNB does have a new line in the sand it is probably closer to parity than 1.05.

Nominal outpaces real CHF trade-weighted strength, SNB intervention picks up

Limits to intervention 1: SNB will struggle to match the ECB printing presses

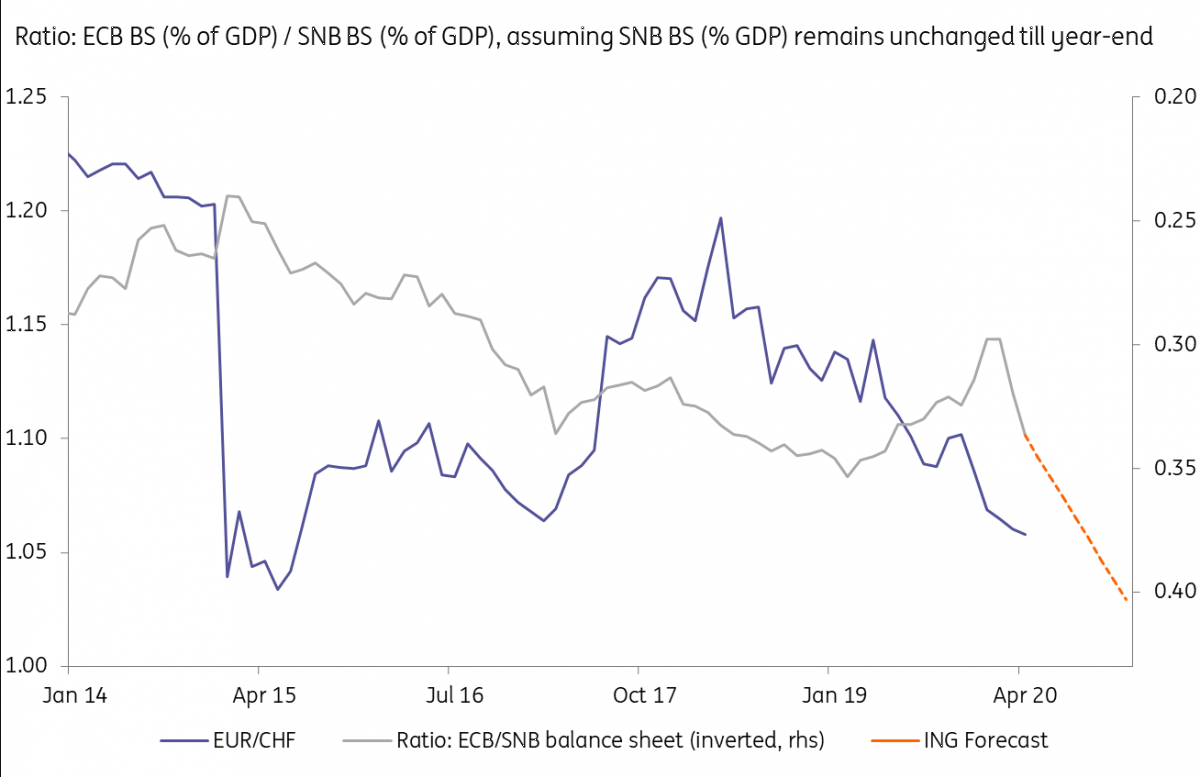

Understandably European fiscal risk premia are seen as a key driver of CHF safe-haven demand. Our team believes these risk premia can be contained this year and see the Italian BTP-German Bund spread ending the year at 170bp from around 210bp today. Does that mean FX intervention from the SNB may no longer be required? Not necessarily.

Based on our calculations, the SNB will have had to spend around CHF180bn between now and year-end to avoid its balance sheet shrinking relative to the ECB’s in GDP terms. (This assumes the ECB’s €750bn PEPP program is topped up by €375bn in June). Why is this balance sheet metric relevant? When abandoning the 1.20 EUR/CHF floor in January 2015 the SNB did so a week before the ECB formally started its QE program and cited ‘monetary policy divergences’ as a reason to discontinue the EUR/CHF floor.

The rationale for the 2011 floor in the first place was in response to a period of ‘exceptional over-valuation of the CHF and an extremely high level of uncertainty in financial markets’. As above, the real CHF trade-weighted index is now 12% below levels seen in summer 2011, and thanks to the quick action of many central banks (especially the Fed and the ECB), levels of financial market volatility have fallen considerably since March. Conditions for a new floor arguably have not been met.

Additionally, increasing its balance sheet to 165% of GDP (from around 130% end March) to match ECB expansion is not without political concerns. While the SNB has said that it can operate with negative equity capital (provisions and equity capital stood at CHF129bn in March after a Q120 loss of CHF32bn was put through its balance sheet), later this year the SNB should be negotiating with the Federal department of finance (FDF) over its contribution to the annual 2021-25 budgets of the confederation and cantons.

After a good year of asset performance in 2019, the SNB will be contributing CHF4bn to those budgets this year. The further enormous growth in its balance sheet this year – and the SNB’s large (20%) weighting to equities - could make a dangerous cocktail for future years and test the SNB’s relationship with the government.

Pressure will build on EUR/CHF unless SNB undertakes massive intervention

Limits to intervention 2: Washington is watching

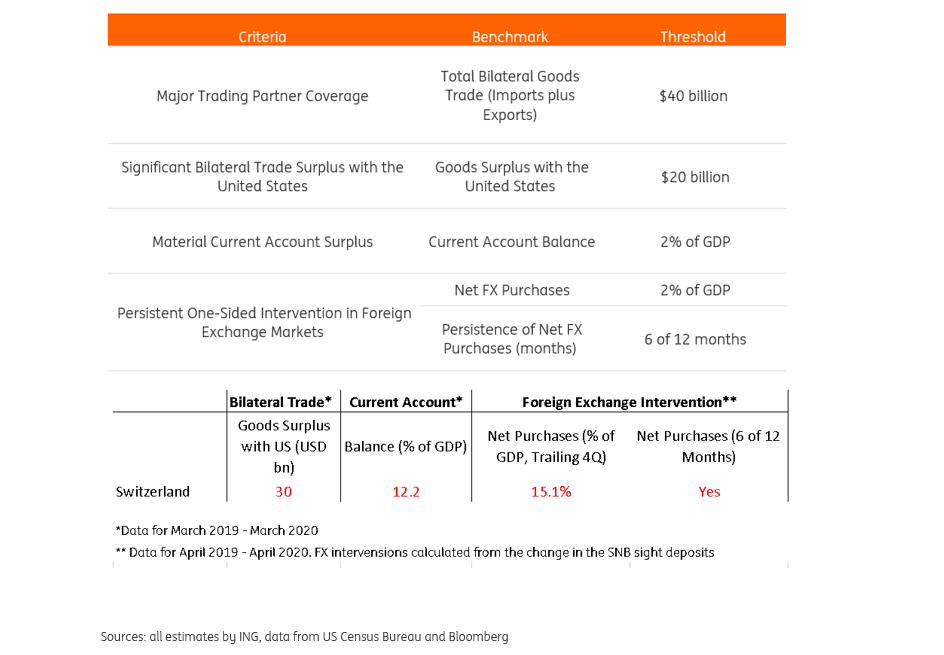

To be honest it is not clear that the SNB takes any notice of Washington at all. The reference here is to the US Treasury last year putting Switzerland back on its ‘watch list’ as a potential currency manipulator.

Washington’s spring assessment of currency manipulation, looking at 1Q19 to 4Q19 data is unlikely to name Switzerland a manipulator in that the SNB’s FX intervention was too small last year. But the explosive growth in FX intervention over the last eight weeks suggests that Switzerland would tick all the boxes in the US Treasury’s autumn assessment.

While the US Treasury undoubtedly has bigger fish to fry than Switzerland, the threat of retaliatory trade action from Washington may also offer some constraints to seemingly unlimited SNB FX intervention. The SNB absorbing 20% of the newly printed euros may also create some friction with the ECB.

Switzerland will fall foul of Washington's currency manipulator criteria

Parity: A case of when not if

We do not think 1.05 is a new line in the sand, primarily because we do not think the SNB has the tolerance to match the ECB printing presses. But over time EUR/CHF will be drifting down to parity.

Whether that is this summer or next year remains to be seen. But certainly now is not the time to start turning bullish on EUR/CHF. In fact, we have only briefly been upbeat on EUR/CHF once since the 2008/09 financial crisis, during the 2017 European re-rating story – a story quickly snuffed out as the 2018 trade war unfolded.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more