US: The only way is up!

- 2 April 2020

After being crushed through March and April much of the economy will recover once containment measures are eased. However, some parts will continue to struggle and some will be changed forever

Containment continues

President Trump has had to ditch his aim of a relaxing Covid-19 related restrictions by Easter. The escalating number of cases and warnings of potentially hundreds of thousands of deaths has meant guidance on limiting social interaction and avoidance of non-essential travel will remain in place until at least 30 April. Three quarters of the US population is under stricter measures with 32 states currently having stay-at-home orders while numerous cities in the remaining states have ordered non-essential businesses to close.

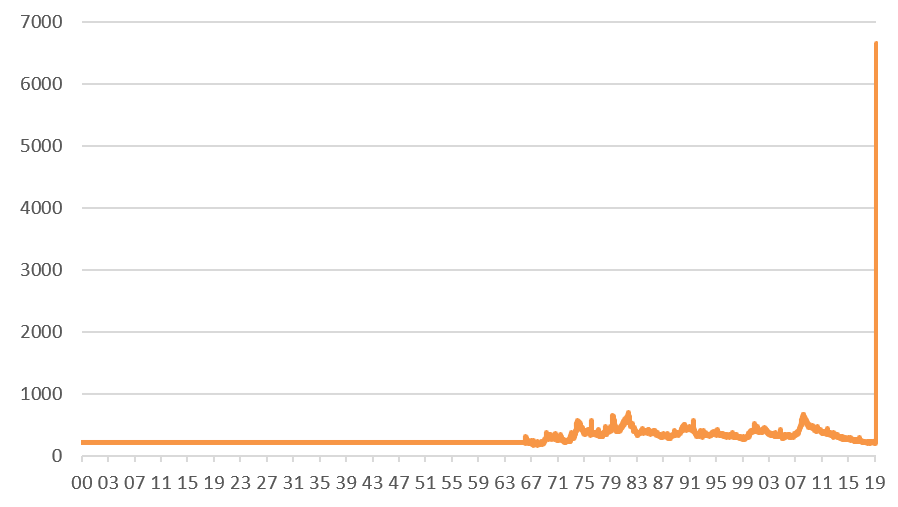

The economic fallout has been 6.6 million people filing a new unemployment claim in the week of 28 March. This followed 3.3 million claims in the previous week, as restaurants, bars and retailers shuttered due to the lockdown. With the number of work from home orders increasing and the fact not all jobs can function in such a manner, unemployment will spread across sectors and likely accelerate.

Treasury Secretary Steven Mnuchin raised the prospect of the unemployment rate hitting 20% while St. Louis Federal Reserve President James Bullard talked of unemployment potentially reaching 30%. Such a scenario would mean the number of people out of work rising from a little under six million in February to around 50 million in a matter of months.

US weekly jobless claims (000s)

A wall of money

These fears led the Federal government to quickly approve a $2 trillion fiscal package. Equivalent to a little under 10% of GDP, it includes measures that offer direct support to both households and businesses while providing another $130 billion for hospitals and $150bn extra for state and local governments to help them deal with the healthcare crisis. There is also $350bn to fund a lending programme for small businesses set up in a way to incentivise keeping workers on the payroll.

Another major thrust is a payment of $1200 for low and middle-income earners plus an extra $500 per child. However, for those that have lost their job, this money is not going to last long. Since the national containment restrictions are being extended, thereby limiting the chances of finding work until at least the end of the month, we suspect there will be calls for additional support - President Trump is already calling for a further $2 trillion package.

The Federal Reserve has also taken unprecedented action, fearing that financial market distress risked exacerbating the downside for the economy. By pumping trillions of dollars of liquidity into the system, initiating “unlimited” quantitative easing, and announcing special purpose vehicles to buy corporate debt, a sense of orders has gradually returned.

Plumbing the depths

However, we have to remember that the Fed response is about mitigating risks, and the fiscal package is about tiding vulnerable families and businesses over until the virus containment measures end and the economy can recover. They cannot compensate for the steep decline in demand through March and April. Consumer spending outside of grocery and online retail has collapsed while business investment has ground to a halt. Trade has also slowed dramatically while the oil and gas industry is additionally being battered by Saudi Arabia and Russian tensions that is further worsening an already huge supply glut.

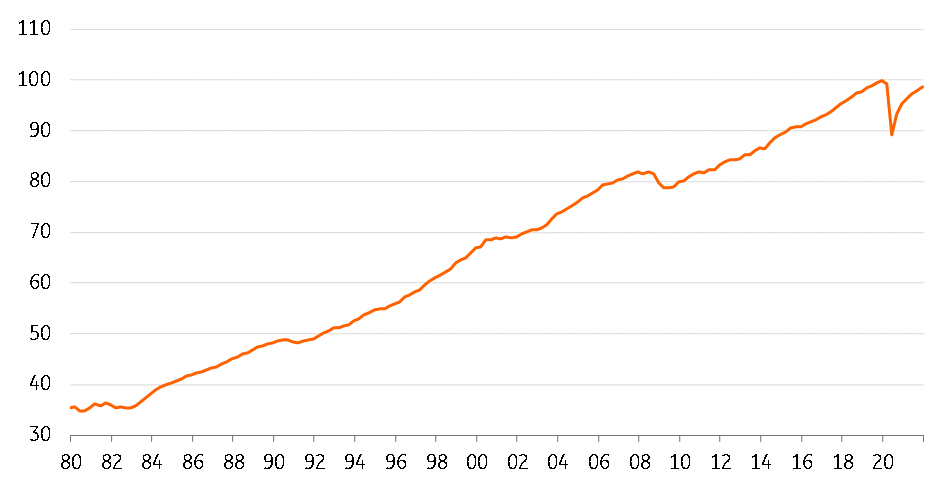

We remain hopeful that the virus threat will subside and we can start to see some relaxation of restrictions in May. However, it won’t be an immediate return to “business as usual” with a rolling process of re-opening likely that still involves some form of social distancing. Our best guess is that economic output will fall around 10% quarter-on-quarter through the current quarter. We have pegged the annualised contraction at 40%.

The prospect of a gradual roll back means that job opportunities for the millions of workers laid-off, particularly in the leisure & hospitality, retail and transport sectors will remain somewhat limited and unemployment will be slow to fall. We also have to be cognizant of the risk that numerous companies don’t make it through this crisis and many that do will need to restructure. For example, "bricks and mortar" retailers were already under intense pressure from online specialists with the number of bankruptcies on the rise, which will in turn hurt commercial real estate. Should business failures lead to higher non-performing loans this will adversely impact banks and could hurt credit availability, which further limits the scope for a vigorous economic revival. Working from home directives may have lasting implications involving less commuting and fewer physical meetings, hurting the travel and hospitality industries.

Given this backdrop, we tentatively suggest that the economy contracts more than 12% peak to trough, compared to the 4% contraction experienced during the Global Financial Crisis, with the lost output not fully recovered until mid-2022.

Level of real economic activity (4Q19=100) with ING forecasts

Inflation and interest rates remain anchored

Inflation will be dragged sharply lower in the near term due to the plunge in energy prices with recession intensifying the threat of deflation (although food prices could be an outlier). In this environment bond yields are set to stay low, despite the fiscal deficit breaking above 15% of GDP and government debt surging above 100% of GDP. They will be even more anchored if the Federal Reserve decides to morph its unlimited quantitative easing programme into a more formal yield curve targeting policy.

One thing that is on the rise is President Trump’s approval rating - now at all-time highs. Should he manage to navigate the crisis well and the economy rebounds strongly later this year he stands an excellent chance of being re-elected. This will be a worry for China and Europe who will remain in his crosshairs as he seeks to cement his position as a President who brings jobs back to America.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Covid-19: The scenarios, the lockdown, the reaction, the recovery

- This bundle contains 18 Articles