US Senate’s proposed clean energy investment reaffirms climate ambition

The Inflation Reduction Act proposed by the US Senate includes less investment in clean energy and climate change than the stalled Build Back Better bill but would accelerate the country’s energy transition. Featuring tax credits for EVs, solar, wind, hydrogen, and carbon capture, the bill would put the US on a more likely path to net-zero emissions

Last week, the US Senate proposed its $739bn Inflation Reduction Act as a replacement of the $1.75tn Build Back Better bill that only passed the House at the end of last year. In a positive surprise, $369bn of the Inflation Reduction Act is planned to be dedicated to energy security, clean energy, and climate-change-related investments. In this article, we discuss the effects of the proposed investment in facilitating the US’ energy transition (as opposed to assessing the impact of the act on inflation) and conclude that it would put the country on a more likely path to achieve President Biden’s climate goals.

What is in the Senate's proposed Inflation Reduction Act

Clean energy manufacturing tax credits to become broader

Tax credits for clean energy manufacturing was the backbone of the energy and climate section of the Build Back Better proposal, with a sweeping $320bn planned. The generous tax credits had raised hopes and interests for clean energy developers to accelerate project rollouts.

A drop from what was offered in Build Back Better, the Inflation Reduction Act plans to spend some $260bn on providing tax incentives to decarbonise the economy. This includes over $60bn to facilitate clean energy manufacturing through production tax credits (PTCs) and investment tax credits (ITCs) that can be applied to all parts of the value chain.

Yet despite the lower spending amount, the Inflation Reduction Act would still play a powerful role in facilitating clean energy development through the extension of many clean energy tax credits, as well as the creation/increase of credits categories for some emerging, not-yet-commercialised technologies.

More generous hydrogen and CCS credits despite stricter qualification rules

Two important emerging decarbonization technologies, hydrogen production and carbon capture and storage (CCS), both made it to the proposed Inflation Reduction Act under the clean energy tax credits.

Same as Build Back Better, the Inflation Reduction Act would introduce hydrogen PTCs of between $0.6/kg and $3/kg. The difference is that the newly proposed rules would increase the emissions threshold of eligible clean hydrogen production from a 25% reduction of emissions compared to gray hydrogen production (using natural gas) to a 56% emissions reduction from gray hydrogen production. Furthermore, to receive the highest credits, a project needs to emit lower than 0.45kg of CO2 per kg of hydrogen, versus the previous 0.5 kg of CO2 per kg of hydrogen in Build Back Better. Despite the stricter qualification provision, the hydrogen PTCs would largely lower the cost of hydrogen production. Bloomberg New Energy Finance estimates that at this PTC level, clean hydrogen production could already be cost competitive with gray hydrogen production.

The US is the second largest consumer and producer of hydrogen behind China. The US produces roughly 10 million tonnes of hydrogen per year, accounting for 11% of the production globally. The development of hydrogen in the US is going to accelerate in the next decade, with the Infrastructure Investment and Jobs Act dedicating $9.5bn to clean hydrogen development and the clean hydrogen tax credits if the latter passes Congress.

As for CCS, both the Build Back Better bill and the Inflation Reduction Act intend to raise Section 45Q tax credits from $50/tonne to $85/tonne of CO2 captured and stored – (if prevailing wage, hour, and apprenticeship requirements are met). And the value would increase to as high as $180/tonne for direct air capture, a more costly technology which directly removes CO2 from the atmosphere. It is nonetheless worth noting that the Inflation Reduction Act plans to lower capture thresholds for projects to qualify.

Section 45Q credits – even at their current levels – are seen as a major revenue source for CCS project developers and a key driver for CCS deployment in the US. More generous CCS tax credits can further cement the US’ leading position in the technology, while a stricter emissions threshold can prompt developers to explore more advanced CCS technologies.

Current and proposed Section 45Q credit levels for CCS

Biofuels to receive support as well

In addition to a $500m grant package to promote biofuels production and improve related infrastructure, the Inflation Reduction Act plans to extend the current $1/gallon tax credits for biodiesel, renewable diesel, and alternative fuels until 2024. This extension would uphold the continuing diversification of biofuels supply beyond conventional ethanol.

Besides, the Act would establish a new tax credit category for sustainable aviation fuels (SAFs), set at a maximum of $1.75/gallon. SAFs are considered one of the key pathways to help decarbonize the aviation industry, which currently accounts for 2%-3% of global greenhouse gas emissions. This year, the Biden administration announced an ambitious goal to slash aviation emissions in the US by 20% by 2030 though ramping up the production of SAFs. The proposed tax credits would not only reduce the cost of SAF production, but also narrow the now c.$0.7/gallon of price gap between SAFs and renewable diesel (with SAFs being more expensive). This outlook would potentially incentivize renewable diesel facilities – that often times are able to produce SAFs – to shift to producing more SAFs.

Solar and wind tax credits extended

Among other things, the Inflation Reduction Act would extend current incentives for wind and solar projects for at least 10 years. For wind projects, the PTCs have already expired, meaning that projects that commenced construction this year cannot claim any credits. The new proposal would make the expired credits available again. For solar projects, the biggest change is that instead of only the ITCs, they would be eligible to choose PTCs as well. The Act would also create two new sets of tax credits for projects that are ‘technology-neutral’—eligible projects need to be power generation facilities that have net-zero greenhouse gas emissions. All these would help sustain renewable installation, further drive down cost, and accelerate the decarbonization of the power sector in the US.

EV development to be boosted by sustained tax credits

Under the proposal, tax credits for electric vehicles (EVs) would remain at the current level of up to $7,500 for each new vehicle purchased and $4,500 for a second-hand EV. This will continue to spur EV adoption in the country. Nevertheless, these tax credits are granted with the conditions that the minerals used to produce EVs will need to be produced in the US or a country with whom the US is a free trade partner; batteries in EVs should also have a significant share of components that are produced in North America. This will help build a stronger domestic supply chain, but it could take time before a mature supply chain takes shape.

Additionally, as opposed to a Build Back Better rule that EVs would no longer be eligible for credits if a manufacturer had already sold 200,000 cars, the Inflation Reduction Act would set up caps on maximum retail prices below which an EV owner can apply for the credits. This clause would widen the eligibility of EV credits because companies such as Tesla, GM, and Toyota have already hit the 200,000 limit, although some expensive EV models, such as from Tesla, would still be excluded.

Moreover, the Inflation Reduction Act will put a wage limit on customers who can apply for EV credits, a specification to boost EV purchases among middle/lower-class customers.

The newly proposed rules would make electric vehicle credits more available to more people who need it

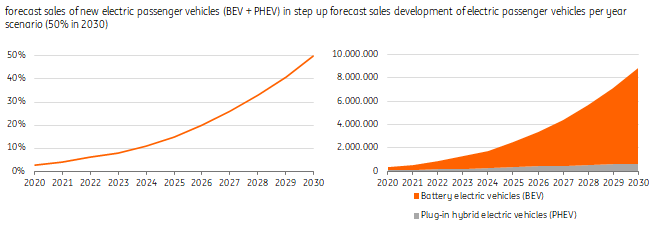

In general, the newly proposed rules would make EV credits more available to more people who need it. Although there is no increase in the total tax credits, the fact that it is in the Inflation Reduction Act emphasizes the importance for EVs to receive continuous support. Therefore, we are maintaining our two scenarios for electrification in the transport sector in the US this decade. In our baseline scenario, the share of electric new passenger vehicles (LDVs) will grow from 4% to 34% by 2030 (including a small share of plug-in hybrids). This means six million new EV sales by 2030, with large underlying differences from state to state, especially between rural and urban areas. In the step-up scenario, which is aligned with the US’ target to increase the share of EV sales in total vehicle sales to 50% by 2030, more generous legislative and regulatory support will be needed to make EV models more affordable, charging infrastructure more extended, and traditional cars relatively more costly.

EV share in sales to reach a third (6m) by 2030 in baseline scenario

Reaching a 50% EV share in car sales by 2030 (8.8m) requires a step up

Separately passed CHIPS and Science Act to boost US semiconductor manufacturing and competitiveness

In late July, Congress passed another bill – the CHIPS and Science Act – and it is now being sent to President Biden to be signed into law. This bill will allocate around $52bn in subsidy and $24bn in manufacturing tax credits to enhance semiconductor production, as well as $200bn to support research and development (R&D) in the industry.

This long-awaited bill will strengthen the US’ capacity and competitiveness in chip production, which would then further aid the development of EVs in the US, as an EV on average requires twice the number of chips as a traditional car.

Nevertheless, car manufacturers will need to choose between Chinese and US semiconductor producers as their supplier – the former would likely keep their advantage in the short to medium term while the latter grows their capacity.

Charging methane leaks: an important punitive measure

Another key provision in the Inflation Reduction Act is to charge, for the first time, methane emissions from along the oil and gas industry’s value chain. With a maximum charge of $1,500/tonne in 2026 for excess methane emissions, this proposed rule can become an important punitive measure to push fossil fuel companies to advance measures to control methane leaking. Indeed, methane is a more powerful greenhouse gas compared to CO2 so its leakage will disproportionally affect global warming. This issue has reattracted attention in the US as a general recovery from the 2020 oil price crash has led to increased oil and production in the country. The US was the world’s third largest methane emitter last year and it is imperative for it to cut methane emissions.

Top ten emitters of methane (2021)

Estimates of US methane emissions from energy sources

US climate targets more achievable than before

Since its inauguration, the Biden administration has set aggressive goals to reduce emissions by 50%-52% by 2030 and reach net zero emissions by 2050. Despite a huge cut from the Build Back Better bill, the Inflation Reaction Act would put the US in a better position to achieve its climate targets. Rhodium Group estimates that the Inflation Reduction Act could alone lower the US emissions from 24%-35% to 31%-44% below 2005 levels by 2030.

It is estimated hat the Inflation Reduction Act could alone lower the US emissions from 24%-35% to 31%-44% below 2005 levels by 2030

Whether the US will really reach the climate targets by 2030 – or even by 2050 – depends on many other factors besides clean energy funding and tax credits. Optimistically, with the expected maturing of clean energy research and development investment, continuing decline of clean energy costs, and the multiplying effect of technology scale-up, slashing nation-wide emissions by half by the end of the decade seem possible. But more measures are also needed to reduce the demand for dirtier economic activities. These include more stringent rules for emissions, a federal tax on emissions, mandates to phase out coal production, or even the establishment of a nationwide carbon price –measures that the US currently lacks.

Either way, the proposed Inflation Reduction Act is a crucial piece of legislation to decarbonize the US economy, especially given the Supreme Court’s recent ruling that the Environmental Protection Agency does not have authority to regulate carbon emissions from power plants. This decision has weakened the executive agency’s power to issue sweeping climate change regulations and has put into question the perspective of other efforts such as the SEC’s proposal to mandate climate-related data disclosure. Now, all eyes will be on Congress to pass the bill.

US greenhouse gas emissions (historical & forecast)

Download

Download articleAuthor

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more