Slow start for US electric vehicles, but times are changing

The US is lagging behind in the electrification of new cars. And while new government policies could help to close the gap, a full shift to electric vehicles will take many years and require massive investment. The government's aim for EVs to make up 50% of new sales by 2030 seems challenging, but large car makers have even bolder ambitions beyond this decade

US lags China and Europe in electric vehicle uptake

The future of cars is electric. But while the US is home to the world’s largest electric car manufacturer – Tesla – the domestic growth of EV sales has been relatively slow so far. Between 2015 and 2020, the EV fleet (battery electric: BEV and plug-in hybrid: PHEV) grew at an annual rate of just 28% compared to 51% in China and 41% in Europe. Still, electric cars are gaining traction in America, despite its affinity for gas-guzzling trucks and SUVs.

US EV fleet on a slower growth path than its peers

Ambitious regulation puts Europe’s EV share in the lead

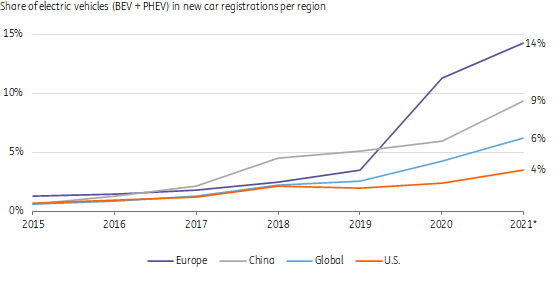

With electric cars (BEV + PHEV) expected to make up 14% of new sales in 2021, Europe is leading this transition, followed by China, at 9%. In the US, the share of EVs is only around 4%. Of these three regions, Europe has the most ambitious regulations. CO2-reduction goals now aim at a complete shift to zero emission vehicles by 2035, with several individual countries targeting an earlier date of 2030. This pushes electrification forwards and has also inspired several manufacturers to announce ambitious commitments to phase out the internal combustion engine (ICE).

The share of EVs in new sales is rising the fastest in Europe

US policy more in favour of electrification, but full commitment still missing

Limited federal policies supporting EVs has been one of the reasons behind the slow uptake in the US. But the current government is ready for change. While the US did not sign up for a complete shift to zero emission cars at the COP26 climate conference this year, the Biden administration is aiming for half of all new passenger vehicle sales to be EVs by 2030. Earlier this year, Biden also announced plans to replace the government’s fleet of roughly 650,000 vehicles with electric models. The recently adopted Infrastructure Bill also gives a push to the development of EV infrastructure. Moreover, on top of the current $7,500 in EV tax credits for car buyers, the proposed Build Back Better spending plans offer an additional $4,500 if an EV is produced by union labour (13% of the EV sales in 1H 2021) and another $500 if the battery is manufactured in the US, driving the total credits up to a maximum of $12.500.

Large differences between states, urban areas are most progressive

At the state level, California, New York and Washington aim to phase out internal combustion engine vehicles by 2035. California has the most aggressive policy and represents the largest EV fleet within the US. Several large US cities have also signed up for the COP26 declaration to work towards zero emission new sales by 2035.

Several state governments are offering incentives to buy EVs on top of the federal tax credits. Today, 47 states and the District of Columbia have rolled out tax credits, rebates, and research grants to boost the production and sales of EVs. For instance, Colorado is providing consumers with a $4,000 tax credit per purchased light-duty EV through 2021. In addition to a wide range of support, California has recently announced that $3.9 billion will be deployed to develop zero emission vehicles. This coincides with the highest fuel taxes in the country.

Car makers position themselves for an EV shift as pressure mounts

Large traditional car manufacturers are ramping up their efforts to electrify cars for the US market. The urgency to cut emissions is increasing and the threat from pure electric players such as Tesla, Rivian and Lucid is growing. The potential entry of Chinese brands such as BYD is also adding to the pressure.

Ford, General Motors (Chevrolet, Cadillac, Buick) and Stellantis (o.a. Jeep, Chrysler, Dodge, RAM) have already made plans to shift away from ICE vehicles and at COP26, Ford and GM pledged to work towards 100% zero emission new car and van sales in leading markets by 2035 “or earlier” and by 2040 at a global level. Other brands with significant market shares, like Nissan and Kia, aim to shift before 2040.

Japanese manufacturers Toyota (incl. Subaru) and Honda top the US car market, but lag in electrification

Japanese brands top the US car market, Ford and Chevrolet lead US light truck market

Corporate fleet owners at the forefront of the transition

Leasing and rental companies show an increasing appetite to invest in the electrification of their fleets. Corporate fleet owners – buying roughly half of the new cars sold - may be at the forefront of this transition as they usually buy new vehicles, vehicles are frequently replaced and they drive more miles (since operational costs of EVs are lower, this makes them attractive). For many consumers, rental cars provide an opportunity to try out driving an EV.

Adaption to US consumer preferences takes time

The total cost of ownership is an important factor in measuring the success of electric vehicles. Battery prices have continued to fall, leading to lower prices and making EVs generally more affordable. But there is more to take into account, particularly the charging infrastructure (see constraints below). Additionally, Americans prefer to purchase bigger vehicles, drive longer distances and enjoy cheaper petrol prices than consumers in Europe. These factors make EVs less competitive in the US market and contribute to a longer transition phase.

Electrification of pick-up trucks helps to fuel the uptake in the US

The introduction of electric light trucks is encouraging given the preferences of US car buyers. Three out of four light vehicle buyers preferred a ‘light truck’ in 2020 (including many vans and SUVs). Outside densely populated urban areas, these are particularly popular vehicles. Hence, for electrification, the availability of electric light trucks is a prerequisite for success. Several electrified SUVs are now available and the first electrified Ford model F150, as well as the upcoming electric vans and light trucks of Rivian, could contribute to the uptake of EVs in the US.

29% of US greenhouse gas emission comes from transportation, which is more than in Europe and worldwide. This is not only because of intensive airline traffic, but also because car ownership is among the highest in the world.

Electric light trucks important for transition of the US fleet

EVs to reach a third of total new sales in 2030 in our baseline scenario

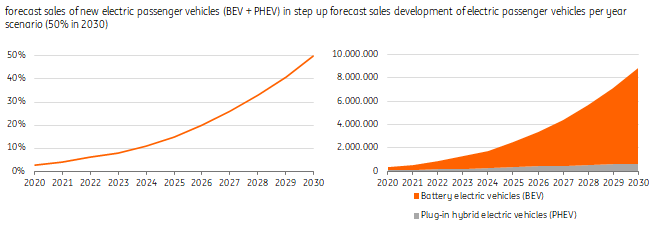

How will the transition play out? Given the political uncertainty affecting the US EV market and other factors (see end of article), we look at two scenarios for electrification this decade. In our baseline scenario, based on BNEF and ICCT, we expect the share of electric new passenger vehicles (LDVs) to grow from 4% to 34% by 2030 (including a small share of plug-in hybrids). This means six million new EV sales by 2030, with large underlying differences from state to state, especially between rural and urban areas.

The total US rolling stock of over 242 million passenger vehicles in 2020 will still grow slightly going forward. In our baseline scenario, the current US EV fleet will expand to 27m by 2030, which comes to 11% of the total fleet. Plug-in hybrid vehicles are on the rise following the hybridisation of existing models, but this will probably stagnate after 2025 when full EVs gradually take over and gain more traction.

EV share in sales to reach a third (6m) by 2030 in baseline scenario

Targeted electric share of 50% in 2030 requires a step up

The US government aims to ramp up EV sales to 50% of total sales by 2030. This is a step up from the baseline scenario and matches the IEA’s sustainable development scenario. Nevertheless, as mentioned, several car makers are backing the ambition and there is interest among consumers. A combination of regulatory support with a wider range of affordable models could lead to an acceleration in EV sales in the second half of the decade.

A 'step up' scenario could result in almost 9m new EV sales by 2030 and a rolling stock of over 36m EVs (15% of the fleet)

Reaching a 50% EV share in car sales by 2030 (8.8m) requires a step up

What are the possible constraints for a faster shift to EVs?

The uptake of EVs this decade faces uncertainties and challenges which could influence the pace of change, despite PHEVs as an intermediate option. The most important are:

- Financial attractiveness – reaching breakeven

- Sourcing and production

- Charging infrastructure and upgrade of the grid

Total cost of ownership EVs not yet on par with ICE

Costs remain an important factor for the uptake of EVs in the years to come. New subsidies mean that EVs might be financially attractive in specific situations, but future grants are uncertain. The cost of full EVs is expected to reach parity with ICE vehicles between 2025 and 2027 in Europe without subsidies, but in the US petrol is significantly cheaper, which could push back the breakeven point. Another risk is that battery prices won't continue to fall as before because of soaring demand for required metals like lithium, and growing scarcity.

US excise taxes on gasoline differ from state to state but are, on average, over four times higher in France and Germany.

Supply challenges may influence EV production growth

Scarcity may also influence the pace of production growth. In 2021, car manufacturers struggled to keep up production because of semiconductor shortages. Going forward, battery sourcing may also become more challenging. Batteries are the engines of EVs, but supply is still highly dependent on a select group of countries. In response, car makers including Ford, Toyota, VW and Stellantis have announced plans to build (through joint ventures) battery plants in the US in order to secure more supplies.

Infrastructure the most crucial factor to enable sales growth

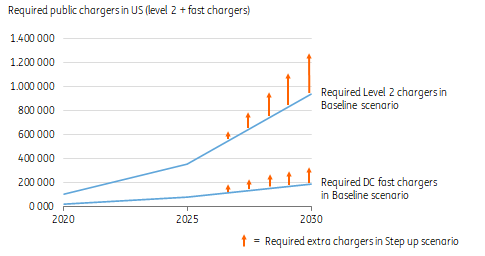

Perhaps the most important factor for the uptake of EVs going forward is the development of charging infrastructure. More electric cars will require a much higher charger intensity, as car drivers need to be confident of sufficient charging capacity on the road. According to ICCT, the number of public level 2 chargers (<19,2 kW) would surge to 883,000 and the number of DC fast chargers (40-800 kW) to 177,000 in a scenario similar to our baseline (graph). In a 'step up' scenario, the number would be even higher. The Infrastructure Bill offers the opportunity to push the total number of chargers up to 500,000, but this is still far from enough.

Network of EV chargers needs to increase even more in a 'step up' scenario

Energy consumption will soar, requiring grid upgrades

The electricity grid will be put to the test by the bold expansion of charging infrastructure. According to some estimates, energy capacity will have to roughly double by 2050 if two thirds of the light duty vehicle fleet are electrified (including usage for other purposes). This means that utilities will need to invest billions to upgrade the grid (substations, transformers, grid feeders),with electric cars becoming part of the energy system.

Share of chargers per EV in the US starts at a lower level than elsewhere

US car manufacturers Ford, GM and Stellantis back Biden's ambition

In 2021, major US car manufacturers announced important initiatives to transform their businesses towards an EV-focused future, though this transition could take many years. Before Biden's executive order targeting EV sales of 50% by 2030, Ford, GM and Stellantis announced in a joint statement their shared aspiration to derive 40-50% of their sales from EVs by 2030. However, the companies also noted that this ambitious voluntary target could only be achieved with timely and comprehensive government policies. Below are some of the announcements from major car manufacturers this year:

- Ford outlined its EV ambitions back in May, with a target of 40% of the OEM’s global vehicle sales volumes to be all-electric by 2030, backed up by the ramped-up electrification-related cumulative capex of $30bn+ by 2025. This includes investments in own battery technology and forming joint ventures, such as BlueOvalSK, with SK Innovation. Ford already has a number of EV models in the pipeline and on sale, including Mustang Mach-E SUV, the F-150 Lightning pickup truck and E-Transit commercial van.

-

General Motors announced EV revenue targets in October of $10b by 2023, growing to approximately $90b per annum by 2030. The company aims for more than 50% of its North American and China manufacturing footprint to be capable of EV production by 2030. Overall, GM announced plans to invest $35b by 2035 in all-electric and autonomous vehicles and launch more than 30 new EVs globally. GM’s electrification strategy will be based around the Ultium modular platform that the company developed to launch a range of EVs using common scalable components. The Ultium-based EVs will include high-volume entries, including a Chevrolet priced around $30,000, Buick crossovers, trucks from Chevrolet, GMC and HUMMER EV as well as the Cadillac EVs such as the upcoming LYRIQ and CELESTIQ. Chevrolet’s Silverado EV pickup is expected to be launched in early January 2022.

BrightDrop, GM’s new business which is developing a connected and electrified “ecosystems” of delivery products and services for the commercial segment, is expected to generate $5b in revenue by the middle of this decade and is aiming for revenues of $10b by the end of this decade, while achieving a 20% operating margin by that point. GM has announced the completion of the first EV600 full-size electric vans, just in time for the holiday season. BrightDrop will also add a second purpose-built commercial EV product – a medium-size EV410 electric LCV in 2023, with Verizon to be the first high-profile customer and Merchants Fleet having orders for both EV600s and EV410s.

-

Stellantis: in July, during its dedicated EV Day, Stellantis presented a comprehensive electrification strategy, targeting “over 40%” of sales in the US from low emission vehicles by 2030 (from 4% expected in 2021), which was in keeping with the voluntary 40-50% target mentioned subsequently in August.

While these transformation plans are indeed momentous, there are existing and emerging pure-EV players which are capturing the imagination of the investor community as evidenced by their formidable market capitalisations. Tesla, an early US mover in this space, has already crossed and passed the $1 trillion threshold, while market arrivals such as Rivian, listed recently, is assigned a market cap of over $100b, at one point exceeding that of Volkswagen, while Lucid currently exceeds that of Ford Motors. Both of these recent arrivals are in the very early stages of their commercial operations but are clearly perceived by equity markets as capable of carving out their niches in the rapidly expanding global EV market.

Download

Download article

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more