US June jobs boom

- 5 July 2019

A really encouraging jobs report that suggests the broad economy is shrugging off the US-China trade uncertainty. While the Federal Reserve is gearing up for precautionary interest rate cuts, we think the market is expecting too much

| 224k |

Number of US jobs added in June(Consensus was 160k) |

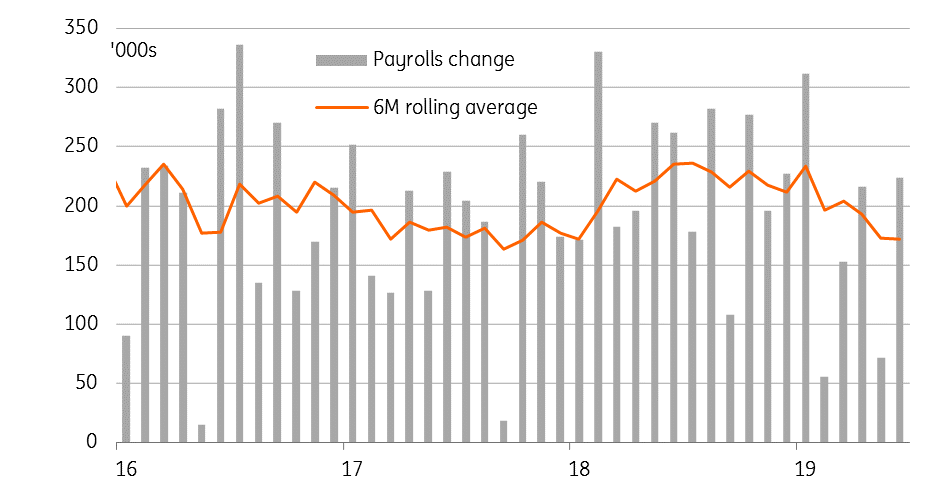

Labour demand remains strong

It is a really strong US payrolls figure for June with 224,000 jobs created versus the 160,000 consensus. In fact, 224,000 is higher than all of the 75 economist estimates provided to Bloomberg! The previous two months of data saw a net downward revision of 11,000, but nothing can take away from the fact this is a surprisingly strong outcome.

Manufacturing payrolls rose 17,000 despite the struggles in the sector relating to an inventory overhang and uncertainty on the trade front. Private payrolls in total rose 191,000 versus the 150,000 expected. Service sector employment rose 154,000 led by business services and education & health, with government employment up 33,000.

Payrolls growth is resilient

But wages and unemployment miss expectations

The unemployment rate moved up to 3.7% from 3.6% (it went to 3.67% from 3.62% for those who are sticklers for accuracy), but this reflects a rise in the participation rate – disaffected former workers being attracted back into the labour force, which should be seen as an encouraging story.

There was some softness on the wage front though. Average hourly earnings rose just 0.2% month-on-month versus 0.3% expected and our own forecast of 0.4%. Annual wage growth remains at 3.1%, which is a little disappointing given the tightness of the jobs market. However, it is well ahead of all the key inflation measures so real household disposable income growth is in great shape, which bodes well for consumer spending in the months ahead.

Payrolls growth will slow, wages can catch up

Taking it all together it is an encouraging report that suggests the broad economy is currently shrugging off the US-China trade uncertainty. We do expect employment growth to slow, but this will be more down to a lack of workers with the right skills to fill vacancies rather than any meaningful downturn in demand – remember the US is in its longest expansion period since 1854 and unemployment remains close to a 50-year low so the pool from which to find new workers is pretty small. However, there should be positive implications for wages as firms seek to recruit and retain staff. The resilience of the US jobs market is a key reason why we believe risks are skewed towards more modest Fed policy loosening relative to market expectations.

What it means for the Federal Reserve

Federal Reserve Chair Jerome Powell testifies to Congress next week and looks set to validate market expectations of precautionary interest rate cuts to head off the threat of a downturn. He may repeat yet again his view that “an ounce of prevention is worth more than a pound of cure”. We look for the Fed to go with a July interest rate cut of 25 basis points followed by a 25bp move in September.

The market is looking for more - pricing in three rate cuts this year with a further 25bp cut in early 2020. However, President Trump will be well aware that pushing too hard for too long on trade risks a weaker economy and plunging asset markets, which would undoubtedly hurt his re-election chances. As such, we would expect him to strike a deal around the turn of the year, claiming the wave of market euphoria a trade deal would generate, coupled with an environment of lower interest rates, as a personal victory that supports his case for the presidency.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

What’s happening in Australia and the rest of the world?

- This bundle contains 7 Articles