US: Jobs rise, but it could soon reverse…

- 6 November 2020

- United States

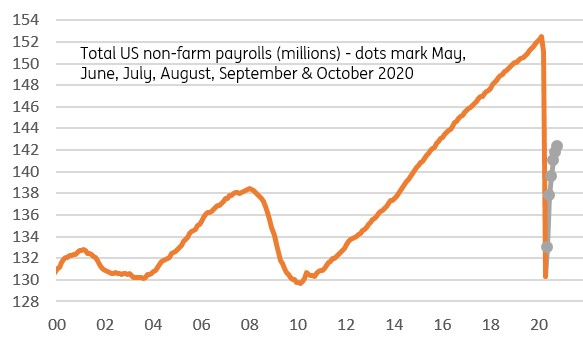

Another 638,000 jobs were created in October, but upward momentum is showing signs of fading with employment still 10 million lower than February. Furthermore, the growing risk of new Covid containment measures means the number of people in work could fall once more

Another upside surprise on jobs

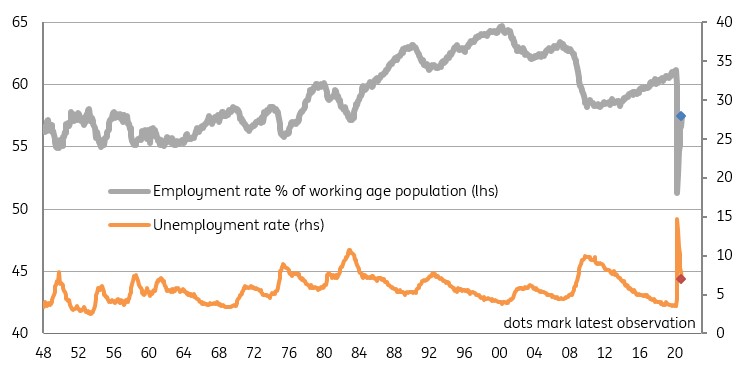

The October jobs report shows US non-farm payrolls rising more strongly than expected, posting a gain of 638k versus the 580k figure expected. There were 15k of upward revisions to the past 2 months while the unemployment rate dropped to 6.9% from 7.9% (consensus 7.6%).

The details show private payrolls rose 906k with broad gains in trade/transport (172k), retail (104k) and business services (208k). Leisure/hospitality continues to improve as well, rising 271k, although government employment fell 268k with around half of that due to the ending of Census contracts. The other half was in local and state government workers, which could be another indicator of their strained finances in the wake of the pandemic whereby tax revenue have been squeezed, expenditure has risen combined with the requirement of running a balanced budget.

Employment remains well short of pre-Covid levels

Even bigger jobs gains in the household survey

Looking at the unemployment figures, we have to remember this is from a separate survey to the payrolls report (which questions employers). The household survey, as its name suggests, questions 60,000 households, and from this they estimate that employment rose 2.243mn – hence the huge drop in the unemployment rate. It is a big discrepancy with the 638k payrolls number, but they do have a habit of diverging considerably at times – some skepticism is understandable given the current question mark hovering over the quality of polling in this country.

Employment and unemployment (% of working age population)

Covid containment threatens further recovery

Overall it is a good outcome re-affirming the economy's strong momentum heading into 4Q. However, we have to remember that there are still 10.1mn fewer people in work than February.

Moreover, with daily Covid cases rising above 100k yesterday there is a real threat that what is happening in Europe right now soon heads this side of the Atlantic. Increased hospitalisations may force state Governors to take the tough decision to shut parts of the economy to try and contain the virus spread. Should bars and restaurants be forced to close again those improvements seen in leisure/hospitality employment will swiftly reverse. Retail would also be vulnerable.

Throw in general anxiety about the virus with consumers stepping back and businesses becoming more cautious on the outlook and we could be in for much weaker jobs numbers in coming months. We hold an increasingly strong bias that the Federal Reserve is going to to end up doing more stimulus rather than scaling back it back.This is especially so if political tensions remain high and get in the way of a swift fiscal response.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more