US battery storage needs innovation for long-term growth

- 29 April

- Energy Sustainability United States

US battery storage growth in 2026 looks strong, but supply chain risks could limit expansion. Rising demand for non‑Chinese components would push prices higher, while greater investment in technology and cost reduction is needed for the eventual subsidy phase-out

Battery energy storage systems (BESS) are set to gain strong momentum in the US, as outlined in our Renewables Outlook for 2026. However, growth projections for 2026 vary widely, ranging from 48GWh (BloombergNEF) to 70GWh (Solar Energy Industries Association, or SEIA). Our view is closer to that of Wood Mackenzie, which expects installations to grow from 54GWh to 56GWh.

Where actual growth lands will depend largely on how well the industry manages supply chain risks – more specifically, shaking off its heavy reliance on China.

In the long term, however, structural cost reduction will be critical as tax credits phase out. We believe that is best achieved through technological innovation.

Supply chain gaps leave BESS projects vulnerable

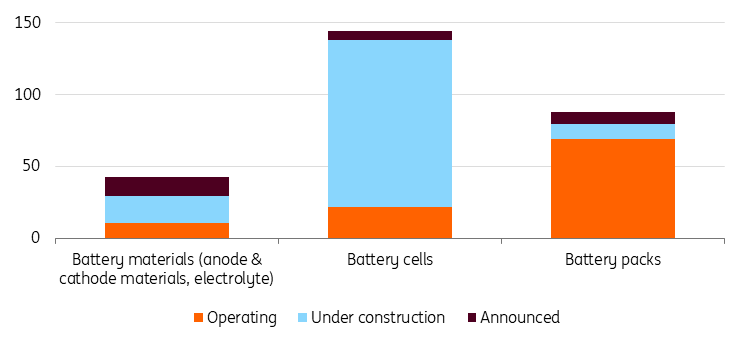

Similar to solar, US BESS manufacturing is heavily concentrated in downstream assembly, with limited coverage of upstream components. SEIA estimates that while the US has 79GWh of nameplate battery pack manufacturing capacity as of early 2026, battery cell capacity stood at just 22GWh, highlighting a significant upstream gap.

Moreover, these figures include producers that make both stationary BESS and EV batteries, so the nameplate capacity dedicated to BESS alone is smaller. Plus, production can run well below nameplate capacity due to upstream bottlenecks. These two factors suggest that US BESS manufacturing has low self-sufficiency. Wood Mackenzie estimates that US battery cell manufacturing capacity could only meet 6% of domestic demand in 2025, though that share could increase to 40% by 2030. The scale of the projected ramp‑up is evident: 116GWh of battery cell capacity is currently under construction in the country.

Tax credits are the lifeline for US BESS to trump cheap Chinese imports

Manufacturing and clean electricity tax credits are crucial to the growth of domestic BESS manufacturing. Without either, US producers would struggle to compete with low-cost Chinese imports.

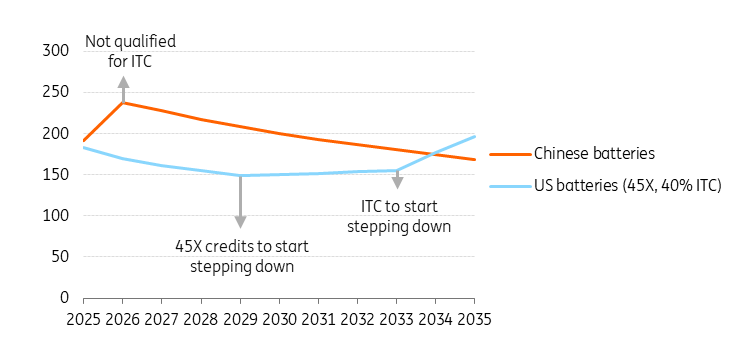

Even under the current tariff regime, US four-hour turnkey battery systems using batteries that benefit from the 45X tax credits are still 31% more expensive than systems using imported Chinese batteries. The gap will further widen when the tax credits start to phase out.

Cost of US 4-hour turnkey battery storage systems

$/kWh, usable (real 2025)

It is only when the 45X tax credits are combined with 48E/48Y clean electricity tax credits in four-hour energy storage projects that US projects using US-made batteries can enjoy a cost advantage.

Cost of US 4-hour BESS projects

$/kWh, usable (real 2025)

This means US battery manufacturers will need to double down on technological advancement and innovation. Based on current technology projections, tax credit phase-outs in the next decade will more than offset the cost advantage among US producers.

But before manufacturing capacity increases meaningfully across all supply chain components, the US BESS industry will remain exposed to tariffs and foreign entity of concern (FEOC) restrictions that target China. Below, we analyse these risks and how they can be managed.

China is still king in US solar imports, but with a weakening role

It is difficult to quickly dismantle China’s dominance, which accounts for nearly 90% of global lithium-ion battery manufacturing capacity. It will take time for the US to ramp up domestic manufacturing, and in turn, it will still need to rely on imports in the near term.

China accounted for the lion’s share of US lithium-ion battery (both EVs and non-EVs) imports in 2025, at around 60%. Although import tariffs on Chinese batteries are higher than elsewhere, the difference has not been as material as seen in solar equipment. And because of safety control, batteries are harder to be transhipped via a third country. Rising tariffs have therefore led to a decreasing share of Chinese imports without much transshipment from proxy countries.

Here's what we'll be watching in terms of tariffs and trade looking ahead:

- Further tariff hike on batteries: It is worth watching whether tariffs on Chinese lithium-ion batteries, currently at 25% under Section 301 (to prevent unfair practices), will be raised further. This year, the US initiated an investigation under Section 301 after the Supreme Court struck down reciprocal tariffs imposed, citing the International Emergency Economic Powers Act (IEEPA).

- Further tariff hike on graphite: Graphite is a key metal in lithium-ion battery production. Natural graphite imports from China currently face a 25% tariff; any further hikes under Section 301 would mean higher supply chain costs for battery developers.

Because of limited battery transshipment from China and decent battery pack capacity in countries like South Korea and Japan, US BESS developers have some ability to shift away from Chinese imports. In fact, battery pack imports from South Korea and Japan rose in 2025 and could increase further this year.

The bigger constraint, however, is battery cells, where alternatives to China remain far more limited. We discuss this in more detail below.

FEOC rules to have far-reaching impact on BESS supply chain

BESS developers will be subject to FEOC rules for longer, as BESS tax credits extend into the next decade, while solar and wind face near‑term eligibility deadlines. This means BESS developers will need to more structurally transition away from reliance on China.

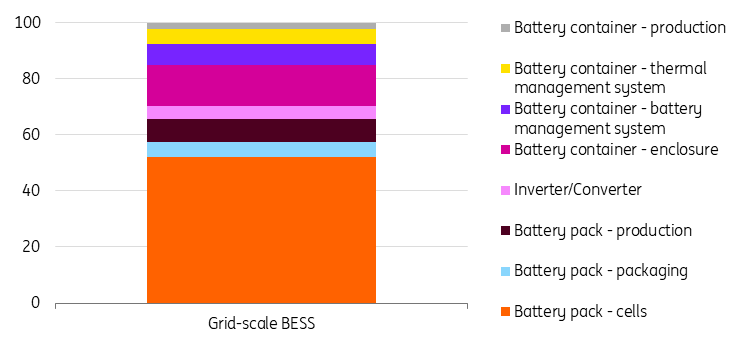

In February, the Treasury Department released draft guidance clarifying how FEOC requirements can be met from a supply chain perspective. The Treasury is expected to issue further guidance on definitions of foreign prohibited entities (PFEs). Below is a summary of the BESS material assistance cost structure, while our detailed FEOC analysis can be found here.

Treasury’s material assistance cost ratios to determine FEOC compliance

%

If a developer now uses imported Chinese battery packs, it will need to replace them with US-made or non-Chinese imports. However, using US-produced battery packs does not eliminate FEOC risk. Developers must still verify that suppliers are free of Chinese influence across ownership, IP licensing, supply chain material assistance, etc.

Among these, battery cells are the most critical component, as they represent about half of the total cost used in the FEOC material assistance test for grid‑scale BESS.

This poses a significant challenge. China controls more than 80% of global battery cell production, while US cell capacity remains limited. On top of that, BloombergNEF estimates that roughly half of the current US operating BESS cell capacity may have high FEOC exposure risk due to corporate structure and IP partnership. That could further constrain near-term compliant supply.

Nevertheless, conditions can improve. Only 17% of planned US cell capacity is expected to face high FEOC exposure (excluding supply chain considerations), suggesting a meaningful expansion of compliant supply over time.

In the near term, rising demand for FEOC‑compliant components is likely to push prices higher. Many developers may prioritise FEOC compliance over domestic content eligibility. Longer term, progress will hinge on the pace of vertically integrated battery manufacturing growth in the US and among non‑Chinese partners.

Car manufacturers’ repurposing EV batteries can boost BESS capacity

As EV tax credits are phased out under the One Big Beautiful Bill Act (OBBBA) and demand for battery storage from data centres accelerates, manufacturers are shifting their focus from EV batteries to BESS.

Ford, for example, has ended its EV battery joint venture with SK On and is repurposing its Kentucky plant to produce stationary LFP batteries, positioning the site as a BESS hub and exploring licensed CATL technology. GM is redirecting excess and used EV batteries to partners such as Redwood Materials and SunPower, supplying BESS for customers, including AI data centres. Stellantis’s joint venture with Samsung SDI has made a similar shift in production priorities.

These strategic moves have reshaped industry expectations, prompting SEIA to double its forecast for US BESS capacity by 2030.

Conclusion

US BESS growth in 2026 looks strong, but efforts to avoid Chinese components could limit expansion. This underscores the need to scale domestic manufacturing across the value chain and, more importantly, to accelerate technology‑driven cost reductions to improve US competitiveness.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

How US trade and industrial policy is rewiring clean energy supply chains

- This bundle contains 2 Articles