US: All systems go

- 1 April 2021

- United States

Consumer spending is supported by stimulus, investment is buoyed by strong order books, and jobs growth is set to soar as the economy reopens in the second quarter, which is why we're revising our 2021 GDP forecast to 6.9%. However, inflation remains a nagging concern and is likely to prompt earlier policy tightening than the Fed is publicly admitting

Spending set to surge

It has been an up-and-down start to the year as the $600 stimulus payment and successful vaccine rollout lifted sentiment and spending in January, only for a harsh winter storm and generally cold conditions to impact supply chains and keep people tucked-up inside in February. However, the numbers for March are set to bounce sharply, with the latest $1,400 stimulus payment being put to use in an economy that is opening up more fully.

As vaccination numbers rise and hospitalisations fall, individual states will relax rules further. This will create more job opportunities while increasing the range of venues for people to spend money. At the same time, household balance sheets are in a strong position, with only around a quarter of the stimulus spent with the rest used to pay down debts and increase savings. This will create a strong platform for growth this year.

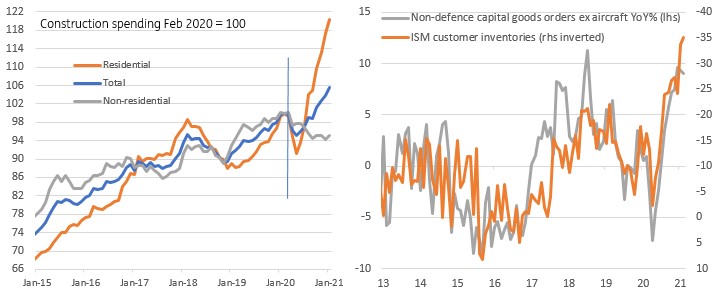

Investment and construction will add to the upside growth risks

We revise up our 2021 GDP forecast to 6.9%.

Corporate investment spending is likely to fuel the recovery further as strong order books and record low customer inventory levels boost the outlook for demand and corporate profits. In the construction sector, robust housing demand amid a dearth of supply will keep house prices elevated and the outlook for residential investment rosy.

Given this situation, we have revised our 2021 GDP forecast to 6.9%.

Building Biden's legacy

A successful recovery from the pandemic is obviously the near-term target, but the Build Back Better infrastructure and green energy investment plan are what President Joe Biden wants as his legacy.

His election manifesto centred on a $3tn+ spending plan that will decarbonise electricity production by 2050. There will be incentives and legislation surrounding energy-efficient buildings and vehicles with additional rail and road infrastructure investment. Money will also be provided to boost 5G and broadband internet access.

These measures will be packaged up with higher taxes for corporates and top earners together with increased property and capital gains tax rates to “reward work, not wealth”.

President Biden is seeking bipartisan support for his infrastructure and green energy investment plan.

President Biden is seeking bipartisan support. However, the proximity to the 2022 mid-term elections adds to the complexity of discussions. It is a key reason why the package is being marketed as a way of competing with China both economically and on technology. After all, there will be a temptation among many Republican legislators to stand resolute, block it, and then blame the Democrats for not compromising. The calculation is that an eventual smaller package fails to live up to voter expectations and hurts the President.

All 435 House seats and a third of the Senate will be up for re-election, and failure to get a deal through could risk being a factor that leads to the Democrats a wafer-thin majority in both the House (222 seats to 213) and Senate (a 50-50 tie with VP Kamala Harris breaking the deadlock) being wiped out.

Such an outcome would leave Biden’s legislative agenda for the second half of his term in tatters. As such, this piece of legislation is critical, and if it is blocked, we're likely to see the package broken up into smaller prices with other routes, such as the budget reconciliation process, used to make sure key plans are passed. While this would involve some watering down of proposals, it can still result in substantial investment and jobs that can help maintain strong economic momentum in coming years.

Inflation could get close to 4% YoY

Turning to inflation, we continue to see upside risks.

In the near term, we could get close to 4% year-on-year as price levels in a vibrant reopened, supply-constrained economy contrast starkly with one in a lockdown last year. These “base” effects will gradually ease, but we see additional upside threats from commodity prices and shipping costs, but mainly from the labour and the housing markets.

Companies are having to pay more for workers and are passing on the costs

While the US has 9.5 million fewer people in work than 12 months ago, companies are struggling to fill vacancies (see chart above, which shows a record proportion of small businesses that cannot fill roles). Part of it is people having to stay at home looking after children, given numerous school districts continue to home-school children. However, expanded unemployment benefits (average of $350 per week state unemployment benefits and a $300 per week Federal payment) means it is difficult to compete with that and get people back to work in many industries.

So, if you want your restaurant, bar, hotel, gym, etc., to reopen, you are going to have to raise your rates of pay substantially, and much of this is will be passed onto consumers.

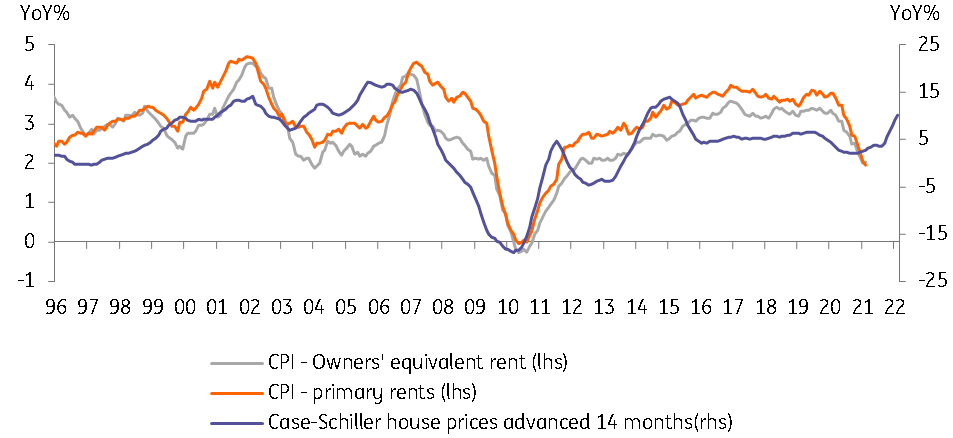

House prices to push inflation higher over the longer term

House prices will be a key factor that keeps US inflation more elevated relative to Europe.

The potentially bigger medium-term issue is house prices rising 15% year-on-year (20% in the northeast of the US). Primary rents and owners’ equivalent rent is 32% of the inflation basket, and it lags turning points in house prices by around 14 months. This is going to be a key factor that keeps US inflation more elevated relative to Europe.

We think the Fed will hike in 2023

Consequently, while the Fed continues to tell us it won’t raise rates until 2024, we think this is going to be an increasingly tough sell given the outlook for growth, jobs and inflation.

We look for two rate hikes in 2023 with the Fed funds target rate up at 2% in 2025.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more