UK: Will May’s deal pass after all?

- 8 March 2019

- United Kingdom

The UK Prime Minister faces an uphill struggle to get her deal approved by Parliament. That means an extension to the Article 50 negotiating period now looks inevitable, but if this delay is kept relatively short, the threat of ‘no deal’ will remain. This would further reduce the chance of a rate hike this year

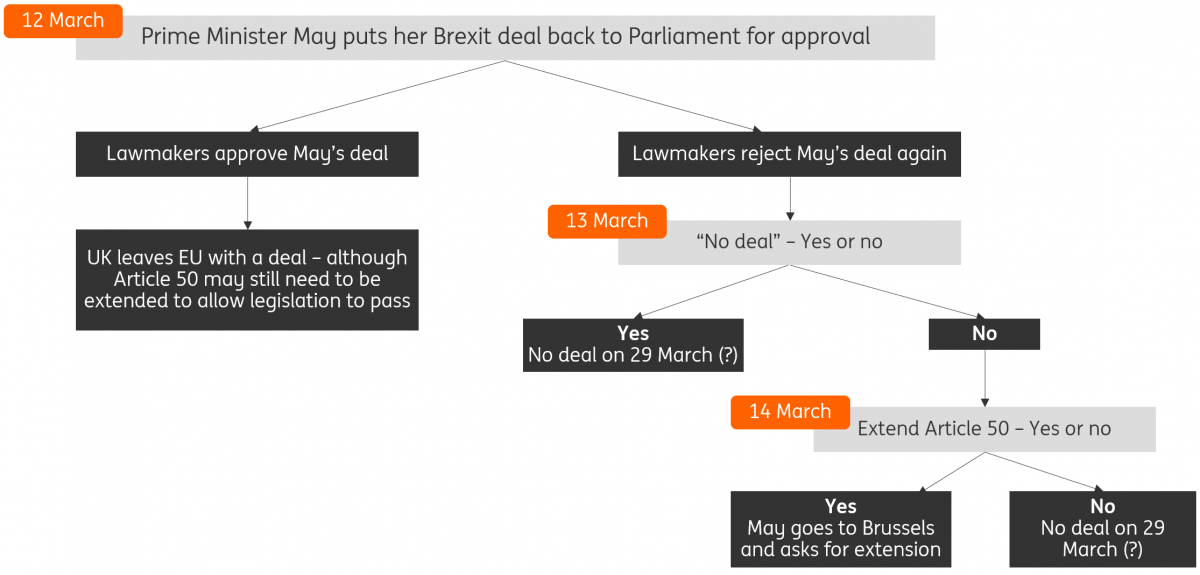

The next week in Westminster may well prove to be the most important in the Brexit process so far, which is saying something. In a series of votes, we’ll discover whether Parliament has changed its mind on Prime Minister Theresa May’s deal, and if not, whether lawmakers would prefer ‘no deal’ instead. If the answer to both of those questions is “no” – which seems likely – then MPs will finally get a vote on whether the UK should return to Brussels and ask for extra time. So how will things pan out?

How the big week in Westminster is shaping up

There have been signs that the Brexiteers are looking for a ‘ladder to climb down’

Cast your mind back to mid-January when May’s deal was heavily defeated by Parliament. 118 Conservatives, alongside 10 Democratic Unionist (DUP) lawmakers rejected the deal, and until recently it has looked highly unlikely that the Prime Minister would be able to win over such a high number of dissenters.

But over the past week or so, the calculation facing the Brexiteers has subtly changed. Where before the choice was essentially between May’s deal and ‘no deal’, it is now highly likely that a rejection of the deal will be followed by a delay to Brexit via an extension to the Article 50 period. In principle, a long delay could see a shift towards other Brexit alternatives like a second referendum, or a softer future relationship, both of which are much less appealing in the eyes of many pro-Brexit MPs than the current deal.

With the looming threat of a delay, the calculation facing Brexiteers is changing

There is also talk that rebel lawmakers may try to force the government to stage a series of ‘indicative votes’ on or around 19 March, to try to establish if a majority does indeed exist for any of these alternative Brexit paths. Reports over the past few days suggest the Government is using this to warn pro-Brexit MPs that this may be their last chance to stop a softer Brexit outcome.

So will any of this be enough to convince MPs to change their minds on May’s deal? Certainly there have been hints that some Conservatives may be looking for a ladder to climb down. Jacob Rees-Mogg, head of the Brexit-supporting European Research Group, appears to have watered down his demands surrounding the Irish backstop.

On that basis, the Prime Minister will be hoping that some changes to the deal may bring enough of her own lawmakers onside. Some hardline pro-Brexit MPs will probably never support the deal, but the hope is that some Labour MPs may be prepared to make the switch – particularly those that represent staunch Leave-supporting seats and are wary about there being a second referendum (which ‘in theory’ is now official Labour policy).

May still faces an uphill battle to get her deal approved

Having said all that, we still think May will struggle to get her deal through over the next week, although the scale of the defeat may be smaller. The Telegraph reports that ministers think they could still lose by 60-100 votes.

After all, the Brexiteers’ demands, while perhaps slightly watered down, remain miles away from what the EU might realistically accept. Secondly, when it comes to the threat of a Brexit delay, a lot will depend on how long this is perceived to last. A shorter Article 50 extension, which appears to be the favoured option at the moment and is unlikely to see too much change in the negotiations, may come as less of a concern to pro-Brexit lawmakers than a longer delay.

Finally, even if there are some ‘indicative votes’ in Parliament on different Brexit options, there is no guarantee any particular one will gain enough support.

True, when push comes to shove, many believe a narrow majority of MPs might be prepared to back some form of softer Brexit. But timing matters, and come 19 March (if these votes do indeed take place), the UK Parliament is likely to have already requested a Brexit delay.

This could take some of the immediate heat out of the situation, reducing the incentive for MPs to reveal their true Brexit preferences just yet. For May, this means that the Brexiteers may be relatively unfazed by her ‘indicative votes’ threat.

An Article 50 extension looks inevitable – but how long will it last?

The upshot then is May’s deal is likely to be voted down on 12 March, and MPs are likely to request an Article 50 extension on 14 March. The big question is how long a Brexit delay might last. Let’s briefly consider the impact of each in turn:

A shorter two to three month delay looks more likely at this stage, given that this would help to avoid some of the logistical challenges presented by the European elections. But within such a short period of time, there is a clear risk that not much would change and for businesses, this would keep the ‘no deal’ risk alive.

A shorter extension to Article 50 would be more economically damaging than a longer delay

While it’s possible the Article 50 period could be extended again, the near-term uncertainty will continue to take its toll on investment. Consumers are also likely to remain wary. That would see the chances of a 2019 Bank of England rate hike recede, although if a deal is finally agreed, we suspect policymakers might not hang around for too long when it comes to further tightening.

A longer extension would provide more reprieve for businesses, which may unlock some hiring and capital spending - although having come to the cliff edge once, it’s possible firms will use the extra time to insulate themselves from another ‘no deal’ scenario.

That said, given the more favourable wage growth story, consumers may become a little more confident, and this could tempt the Bank of England into hiking rates over the summer. But this relies on the economy regaining momentum through the second quarter. If it doesn’t, then it’s equally possible that a long extension to Article 50 could result in a prolonged pause at the Bank of England.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

March Economic Update: In like a lion, out like a lamb?

- This bundle contains 9 Articles