UK rate cut timing hinges on spring inflation data

The Bank of England will want to see the impact of annual price indexation and the National Living Wage hike in April before cutting rates. We're sticking to our call for an August rate cut

After last year's drama, the BoE will want to see April's inflation data

Financial markets began the year expecting the first Bank of England rate cut in May. That’s since been pushed back to August. Admittedly that says more about the shift in Federal Reserve expectations, but we think investors are right that the second quarter is too early for the first UK rate cut.

That’s partly because of the prospect of tax cuts at the 6 March Spring Budget. All else equal, that would require slightly tighter monetary policy, though in practice the room available for sizeable tax cuts appears pretty limited, barring some major fiscal gymnastics.

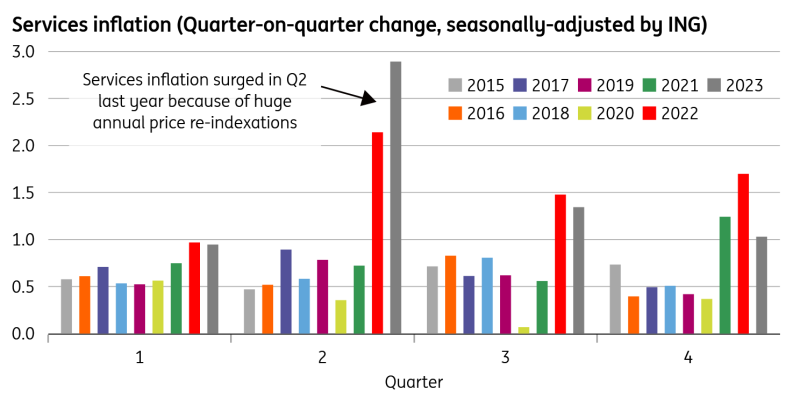

Remember too that the Bank of England is watching services inflation and wage growth above all else, and the second quarter will be hugely consequential for both. April is the peak month for annual indexation of prices and roughly speaking, 40% of the services inflation basket is affected. You'd think this should be fairly predictable, given that many of these price rises are contractually linked to prior rates of overall inflation. But in practice, last year saw services inflation come in well in excess of forecasts in both April and May. We saw large price rises across a range of categories, including rents, where we saw a highly unusual spike in social rents.

The chart below shows that even after seasonal adjustment, the quarterly change in services CPI during the second quarter was huge last year. This year’s indexation should be less severe given the progress made on headline CPI over recent months. But we suspect the Bank won't want to second guess this and will want hard data before cutting interest rates.

The second quarter of 2023 was massive for services inflation

A rate cut is possible in June, but more likely August

April is also when the National Living Wage (NLW) is increased, and this year the percentage increase of 9.8% is fractionally larger than in 2023 (9.7%), so is therefore more significant in real terms. Big picture, the impact on average wages shouldn’t be enormous. Only 5% of workers were paid at the NLW in 2023, and even then, firms seem to be rapidly increasing pay for lower-wage workers anyway. The three-month annualised rate of monthly pay growth for those in the 25% percentile – a reasonable proxy for earners around the national living wage – is already running at 10%.

All in all, the Bank of England reckons this NLW hike could add 0.3ppts to headline weekly earnings growth. That’s not huge, but we imagine policymakers will want to see some hard data on this before they can be sure.

At the minimum, we think the Bank will want to see the April and May inflation figures, the latter of which is released the day before the June policy meeting. Likewise, the wage data released in mid-June will be the first opportunity to gauge the impact of that NLW hike. If these come in well below the Bank’s projections, then that could conceivably unlock a June rate cut. But more likely, we think the BoE will prefer to wait until August when it has new forecasts available, as well as another month of data.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

1 March 2024

ING Monthly: Deciphering the cycle This bundle contains 13 Articles