UK: Deteriorating growth backdrop points to steadier rate hikes

- 5 May 2022

- United Kingdom

UK consumer confidence has plunged close to record lows, and a negative second-quarter growth figure looks likely. We expect another Bank of England rate hike in June and August before the committee pauses its tightening cycle

UK growth story is similar to that of Europe...

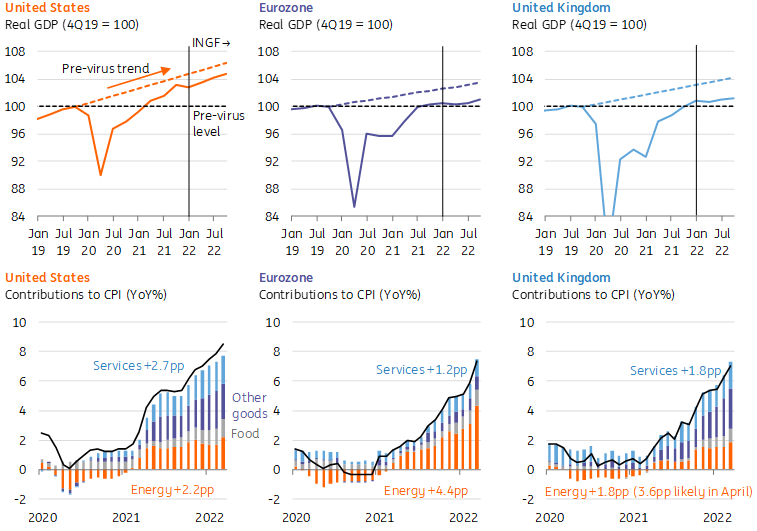

The UK and the Bank of England (BoE) sit somewhere between the US Federal Reserve and the European Central Bank when it comes to tightening policy. As BoE Governor Andrew Bailey emphasised recently, the UK growth story is much closer to that of Europe, not least because of Britain’s reliance on natural gas as a source of electricity – even if very little of it comes from Russia directly.

The outlook for personal finances is perceived to be worse than at any point during the 2008 crisis.

Consumer confidence has plunged, so much so that the headline index is only one point from its all-time lows. The outlook for personal finances is perceived to be worse than at any point during the 2008 crisis. That’s not surprising given the average electricity/gas bill looks set to have increased from £1,200 a year ago to around £2,600 in October (net of a government rebate). Ominously, retail sales have fallen for two consecutive months. That’s likely to help drive a fall in second-quarter GDP, albeit much of the weakness is also owed to an extra bank holiday in June to celebrate the Queen’s jubilee, as well as a decline in health output now that free Covid testing has ended.

How the UK growth and inflation backdrop compares to the US and eurozone

... but Britain's jobs market more closely resembles the US's

But while the growth story looks remarkably similar to the eurozone, the jobs market story bears more resemblance to the US. Wage growth is running ahead of where it was before the pandemic, owing to a fall in participation and unusually high labour shortages. For the first time in recent history, there is now one vacancy per unemployed person. Admittedly, we think nervousness about a wage-price spiral seems overdone, and it’s worth remembering that pay is unlikely to keep pace with prices for most workers over the next couple of quarters.

Indeed, we’ve revised up our inflation forecasts again, and now expect a peak in headline CPI of close to 9% when April’s data comes through. We’d still expect a very gradual downtrend thereafter given that at the same time last year, durable goods prices began to increase at speed (most notably for used cars). Even with those downward-pushing base effects, inflation is unlikely to dip below 7% this year – and indeed will probably stay above 8% for several consecutive months. Clearly it could come in higher still.

Markets are assuming that this inflation pressure means the UK's tightening cycle won't look too dissimilar to the Fed’s this year. The BoE has hiked four times now and before the May meeting investors were pricing further rate hikes at every meeting this year. But the meeting's cautious tone and a dovish set of new forecasts suggest the Bank's tightening cycle will be much less aggressive. We expect another rate hike in June and probably one more in August, before the committee presses the pause button.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Hiking in the dark

- This bundle contains 12 Articles