UK: A mixed recovery story

- 1 April 2021

- United Kingdom

The news on the UK's vaccine rollout and Covid-19 strategy is, for now at least, still fairly promising. That bodes well for a second-quarter growth bounce, but thereafter we suspect the recovery may be a little more muted than in the US. Price pressures are likely to be less of an issue for the Bank of England, suggesting no tightening before 2023

The vaccine rollout continues to go well

Having endured a long and strict lockdown for all of the first quarter, the UK economy is now gradually reopening. And at face value, things still look fairly promising.

The vaccine rollout has now offered all over-50s, or roughly half the population, a first dose. Unfortunately, supply is expected to decrease in April, owing to a delayed shipment of AstraZeneca vaccines from India. However, reports of stockpiled doses suggest the NHS will still manage to administer a significant number of second doses.

Meanwhile, despite all the noise emanating from the EU over export bans, the improving supply picture for governments on both sides of the channel should hopefully mean the rate of first doses picks up again from May. At this stage, it still seems likely that most adults will have received at least a first dose by the end of the second quarter.

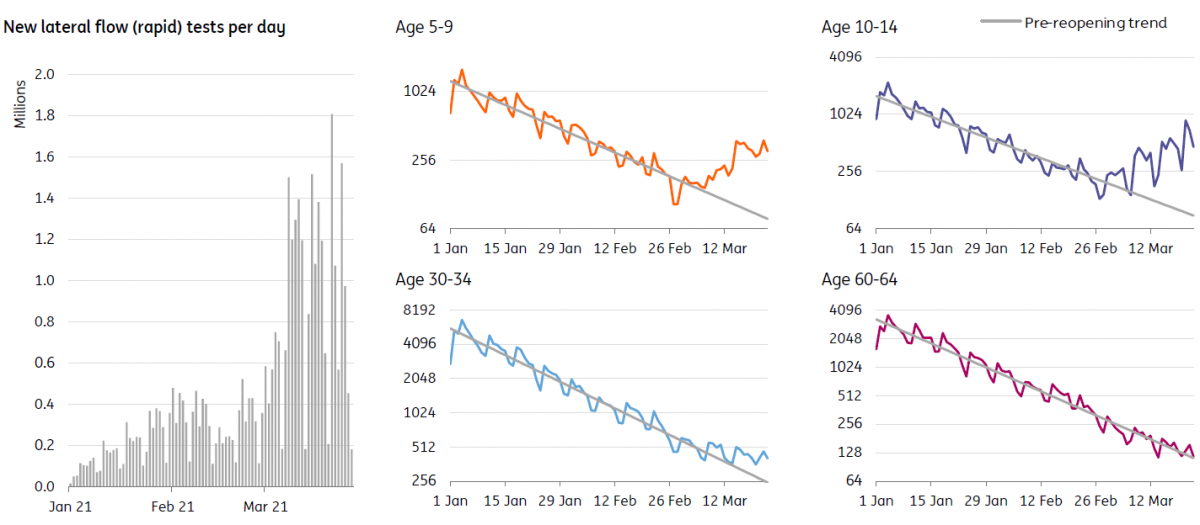

On Covid-19 cases, the picture is still generally good and means the April and May parts of the reopening plan appear on track. We have seen cases rise among school children since the reopening of classrooms earlier in March, though so far, this has not been meteoric, and the number of tests has skyrocketed. At the time of writing, we think there have been roughly 10 million extra rapid tests conducted in England on top of what was already being done, most of which presumably linked to schools.

Despite that, there have been ‘only' around 10,000 extra cases among school-age children across the UK.

Cases are rising among children, but mainly because of greater testing

The risk, unsurprisingly, is that case growth picks up considerably in the intervening period between reopening and wide-scale vaccination. Until larger chunks of the under-50 population is partially vaccinated, there’s still clearly a risk of transmission (and ultimately, mutations), even if the mortality/hospitalisation risk has been considerably reduced.

However, if we assume the next couple of reopening stages remain on track, then we should see a decent second-quarter bounce, probably in the region of 4-5%. This is a little lower than we’d forecast before, though only because the fall in output in the first quarter appears to have been less disappointing than first feared.

UK inflation set to be more muted than the US

Thereafter, there are reasons to think the recovery may be less exciting than that in the US. It’s a consensus view that unemployment will rise as furlough support is removed, though the hope is that the rise in the jobless rate may be limited to 6-6.5% (from 5% now).

Admittedly, we hope the recovery from the peak may be a little faster than we’ve seen in previous recessions. The fact that most of the prior - and anticipated - job losses are so concentrated in consumer services is unusual. These sectors tend to have above-average employee turnover rates and have historically led other sectors out of unemployment spikes. Hopefully, the same should be true this time once the likes of hospitality and other consumer service business are back on their feet. But there will still inevitably be a ’scarring effect’, amplified by the higher cost burden many firms encounter due to Brexit suggesting the outlook for wage growth is relatively benign.

Headline inflation is likely to rise to around 2% later this year, but there are reasons to think this inflation spike may not persist until 2022

That said, headline inflation is likely to rise to around 2% later this year, predominantly driven by energy but not helped by recent supply chain disruptions both globally and locally due to Brexit. Durable goods inflation already spiked in the second half of 2020.

However, there are reasons to think this inflation spike may not persist until 2022. While we expect some supply/demand imbalances in the service sector to trigger price rises, they may not be wide-scale enough to have a large and long-lasting impact on core inflation.

For the Bank of England, this means that there is no rush to remove the current level of stimulus, and tightening is likely to be a 2023 story. That said, we also think the chances of negative interest rates materialising this year have continued to fall.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more