Energy Outlook: Three scenarios for European power prices

- 26 January 2022

- Energy

2021 was a year to remember for European power prices. This year is likely to be no different and markets face an unusually high degree of uncertainty as a result. Here we present three power price scenarios

2021: a year to remember

"European power markets ease, but prices remain high"; that's what we wrote last year in our first power market outlook. The typical seasonal easing of power markets during the summer months did not happen. And we were right about prices remaining high. In fact, they skyrocketed.

We indeed had a perfect storm and power prices in European markets, on average, increased eightfold. Gas prices rose fourfold in 2021 and carbon prices threefold. European natural gas inventories were unusually low even before the start of the winter season, and so was power supply from renewables, particularly from wind turbines. Added to all that we had geopolitical tensions which also weighed heavily on prices.

Unfortunately, there is no quick fix for policymakers. Some governments have responded by compensating consumers and small businesses, capping profits for utilities, or by implementing minimum filling levels for gas inventories. But these measures don't give us any viable or immediate solution to the current imbalance in energy markets.

We are likely to remember 2022 too

Nobody knows the path for power prices as the drivers that set them apart are almost impossible to predict:

- A cold or warm winter makes all the difference but scientists can't accurately predict the weather beyond 10 to 14 days.

- The geopolitical situation also holds a firm grip on power markets, in particular the relations between Russia and Ukraine and its repercussions for the Nord Stream 2 pipeline.

- The Omicron variant also adds a lot of uncertainty to the macro-economic outlook.

So, the future of power prices is highly uncertain and in fact, 2022 could be the year of new records. But it could also be the year where we see sharp power price declines. Whatever the outcome, 2022 is likely to be a year to remember, too.

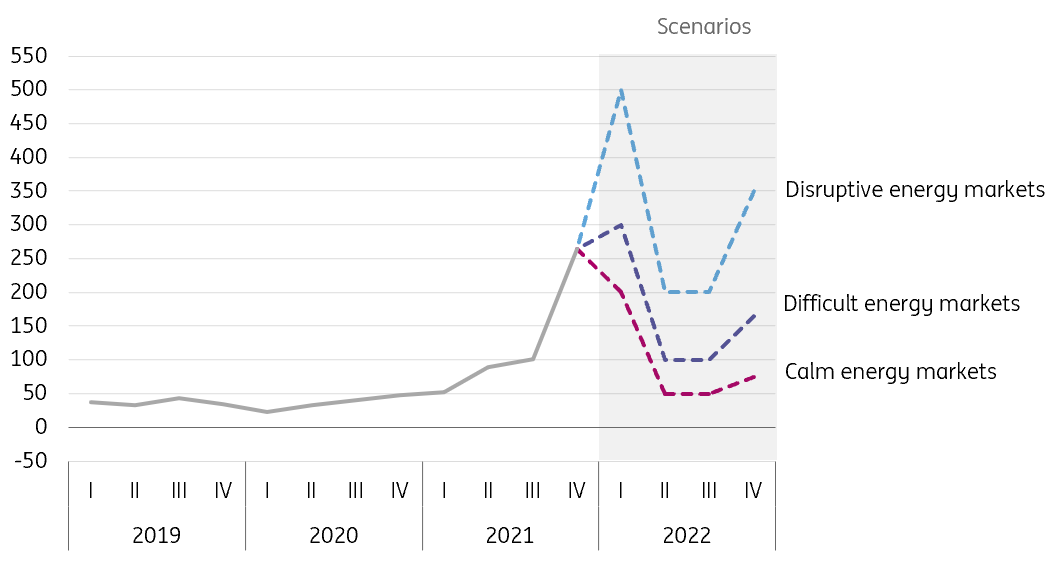

A perfect storm in power markets

Baseload power price in Germany in €/MWh

What happens next to power prices mainly depends on weather conditions, the economic recovery from Covid-19, and geopolitics. Energy supply factors also play a major role. In such an uncertain world, we're setting aside our forecasting tools and applying scenario analysis instead.

Here are our three scenarios for 2022:

Unusually high degree of uncertainty for gas and power markets

Three scenarios for European gas and power prices

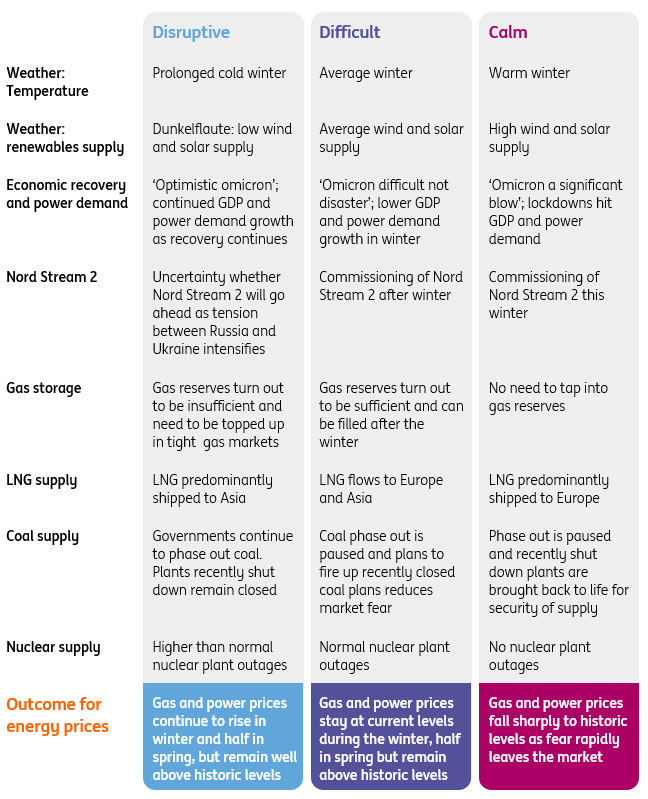

Disruptive energy markets

Weather conditions, an escalation in geopolitical tensions, and limited energy supply all turn for the worse in energy markets. The low levels of gas inventories turn out to be insufficient during a prolonged and cold winter. Nord Stream 2 will not be operational during the winter and LNG supply mainly flows to Asia as prices are even higher in that region.

Omicron turns out to be a significant blow to the economy. Lockdowns ease energy demand to some degree but that cannot compensate for the strong increase in heating demand from the cold winter. The firing up of coal plants that were recently closed but not yet dismantled, cannot either. Unforeseen problems with nuclear power plants further add to the supply problems.

Gas supply is too low to meet demand. In most countries, consumers are protected so they can continue to heat their homes, but energy-intensive businesses are forced to reduce energy demand and thus output. Many have done so already as they operate at a loss given the high energy prices. Power prices set new records in European markets and stay at elevated levels throughout the winter.

Tightness in energy markets results in disruptive spillovers to the real economy. A major political concern will be whether output reduction based on market forces is optimal from a societal point of view.

Energy-intensive producers of fertilisers are likely to scale down production at an early stage in the cycle. But this could induce negative feedback loops on food production in particular because this energy crisis is more or less a global thing. Aluminium producers are also likely to reduce output at an early stage, but this could negatively impact supply chains in manufacturing and construction.

Difficult energy markets

The winter won’t be extremely cold or warm, but normal. Political tensions normalise. The Nord Stream 2 pipeline is not put to the test between Europe and Russia and opens late this winter. But an early announcement could already reduce market fears of shortages. While Omicron is difficult to manage, it does not turn into a disaster for the economy.

Gas supply can just about meet demand as gas inventories turn out to be sufficient and vast amounts of LNG are shipped to Europe. Companies can continue to produce, albeit at high energy costs. Hence, energy markets turn out to be extremely difficult and challenging, but they are not disruptive.

Calm energy markets

A cold and prolonged winter, little supply from renewables (Dunkelflaute), and an escalation of the situation in Ukraine did not materialise. Omicron starts to fade quickly; its less-lethal spread means there's far more natural immunity around the globe and mass vaccinations also enable the economic recovery to continue.

Gas supply exceeds demand and energy prices are in for a rapid decline, leaving no room for negative feedback loops to the economy.

The market currently expects a difficult scenario

Market participants often can’t wait to see what scenario materialises. Large energy-intensive companies in manufacturing and agriculture need to act now to secure their energy supply or hedge power price risks. Power market futures provide insights into how the market expects prices to evolve.

Power traders collectively believe that prices will halve when the European spring arrives, which is in line with the base case scenario. But still, power prices remain well above normal levels for April until September at around €40/MWh.

Power prices are expected to remain high in 2022

Future baseload power prices for 2022 in €/MWh

We could be here for at least another year

Interestingly, future prices stay high throughout 2022, with only a modest decline during the spring and summer.

So 2021 will turn out to be an important turning point in energy markets if these future prices turn out to be an accurate forecast. Until 2021, gas supply was abundant and power prices were relatively stable over longer periods of time, except for increased short-term volatility from intermittent sources such as wind and solar energy.

The market became very tight in 2021 and this could be a new normal, for a few reasons;

- Governments are phasing out some of the key pillars of the energy systems from the past, notably coal in countries such as the UK, Netherlands and Germany, nuclear energy in Germany, Belgium and France, and gas production in the Netherlands.

- Investment in the oil and gas industry has been stubbornly low over the past few years.

- Demand for gas has been rising, particularly in Asia.

- Russia has met its long-term commitments to deliver gas but has been reluctant to provide additional supplies in tight markets.

- Some gas storage facilities in Europe were closed, such as the biggest UK gas storage facility, with no new backup facilities in place such as hydrogen storage.

In short, old fossil fuel energy systems have been taken down faster than demand has declined and new renewable energy systems have been built. These structural trends are not easily solved and hence the market currently expects prices to remain high in the coming years.

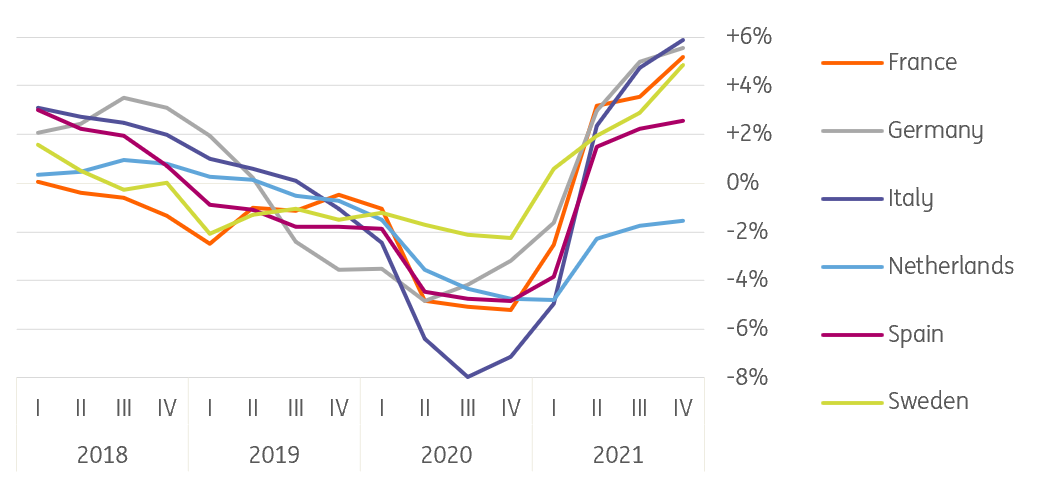

Omicron and negative feedback loops from high prices determine the course of power demand

Electricity demand showed a robust recovery in the second and third quarters of 2021 when lockdowns ended and shops reopened. Growth has continued since, especially in countries that were hit hard, like Italy and France. On a 12-month basis, Italy’s power consumption at the end of 2021 came in 5.9% stronger than a year ago. Germany and France registered 5.6% and 5.2% growth, respectively.

The future trajectory of electricity demand depends on the strength of the economic recovery and whether or not we will have more lockdowns in 2022. Extremely high power prices are likely to lower electricity demand, especially when they persist in scenarios one and two.

Strong recovery in power demand growth from 2020 lows

Year-on-year growth in power demand, four-quarter moving average

Smaller utilities suffer, but the larger ones do relatively well

These are hard times for the smaller utilities, with almost 40 of them going bankrupt in Europe in the past few months.

Elevated power and gas prices created an acute crisis for the weakest players, especially in the UK. Those worst hit were energy suppliers without any power generation assets. With a business model based on contracting new customers on low tariffs in order to gain market share, a large number of retailers faced a price squeeze in 2021.

The larger utilities are doing relatively well and can now benefit from new clients. In the UK alone, Shell Energy, EDF, British Gas and E.ON gained approximately 630,000, 580,000, 530,000 and 250,000 clients, respectively, as the UK regulator assigned the failed customers to larger utilities.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Energy Outlook 2022: Powering ahead

- This bundle contains 5 Articles