Three scenarios for energy prices and the global economy

- 31 March 2022

- Energy

Our new base case has oil prices staying above $100/barrel throughout 2022, while gas prices stay elevated as the EU competes for LNG supply. That's likely to see the European economies flirt with recession this summer. Our two alternative scenarios show how the macro landscape could change if energy prices rise or fall further than expected

One month into the war in Ukraine and it’s still hard to make any predictions about how long the conflict may last, nor the direction it might take. Any forecasts for the global economy are still very tentative, and macro models that struggled to predict the economic outcomes of the pandemic should again be taken with more than a pinch of salt.

That said, we know the main channels through which the war will affect the global – and above all the European – economy, even if the magnitude is uncertain. And the biggest channel of all is energy prices. This article looks at three scenarios for oil and gas prices and the possible wider implications.

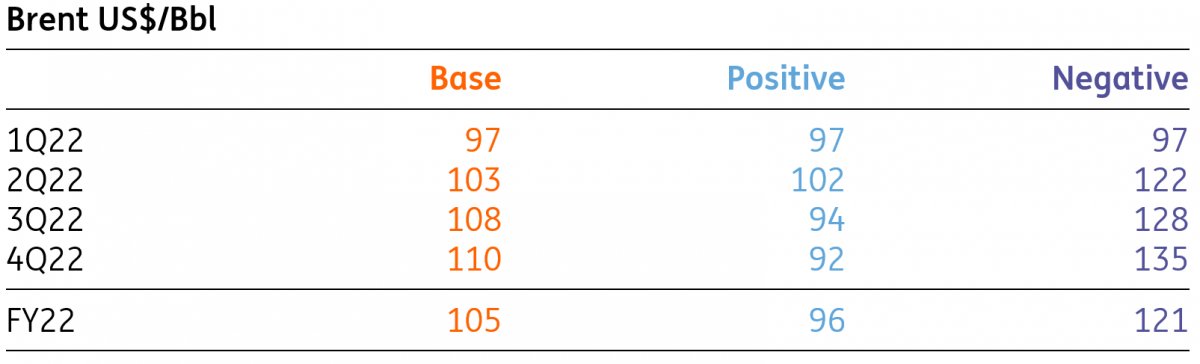

Brent crude oil

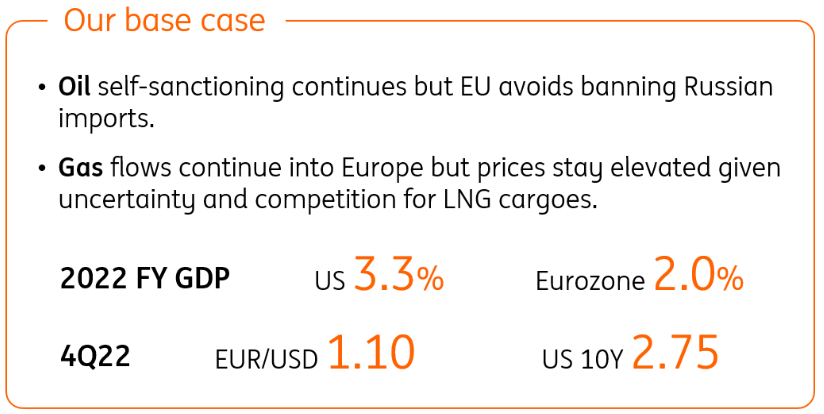

Our base case

For our base case, we’re assuming that the current sanctions remain in place for some time. For oil, that means we continue to see a lot of self-sanctioning – to the tune of two million barrels/day – even if Europe continues to be reluctant to impose import bans. Oil will trade in the $100-110/bbl range for much of 2022.

Russian gas flows continue to flow into Europe, but uncertainty surrounding flows this summer and into next winter keep prices elevated. European prices will also need to remain strong in order to out-compete Asia for spot liquefied natural gas (LNG) cargoes. The EU is targeting 50bcm of LNG imports to help replace Russian gas (which totalled 155bcm in 2021).

For the economic outlook, there are three key implications:

Firstly, inflation stays higher for longer. Energy will soon be contributing almost four percentage points (pp) to Eurozone CPI. Food prices – led higher by key agricultural inputs and fertiliser costs – will add further upward pressure too. And just as supply chains were showing hints of recovery, the war in Ukraine means further disruption – in part because of widespread self-sanctioning of Russian-produced goods but also due to the complete rerouting of logistical supply chains.

Secondly, Europe will see at least a quarter of negative growth – though the jury’s out on a full recession. Consumer spending growth slows, though a large savings buffer and some post-Covid momentum offer offsetting support. Government measures will also help, although in Europe the response varies considerably by member state, and appetite for another pan-EU fund is likely to remain limited. Instead, the fiscal rules will be put aside at least until 2023 and possibly even longer. That said, European leaders may be willing to agree to some extra common borrowing to finance loans for member states – similar to the ‘SURE’ programme created during Covid-19 to fund furlough schemes.

Europe will see at least a quarter of negative growth – though the jury’s out on a full recession

The US is more insulated than Europe, being a net energy producer (and in fact, higher prices are stimulating activity in the oil/gas sector). Indeed, the strong jobs market and rising wages, coupled with a $36tr increase in household wealth during the pandemic, should provide further mitigating support. The Democrat’s wafer-thin Senate majority means it’s hard to see any substantial spending measures taken before November’s mid-terms.

Finally, this Atlantic divergence in growth prospects translates into stark differences in monetary policy strategies. The Federal Reserve doubles down on tightening and the funds rate hits 3% in early 2023. The European Central Bank (ECB) stays cautious, albeit a late-2022 rate hike (and another shortly after) is our base case. The Bank of England (BoE) hikes once or twice more before pausing, amid rising wariness about growth.

We discuss all three themes in more detail elsewhere in our ING Monthly.

Our base case

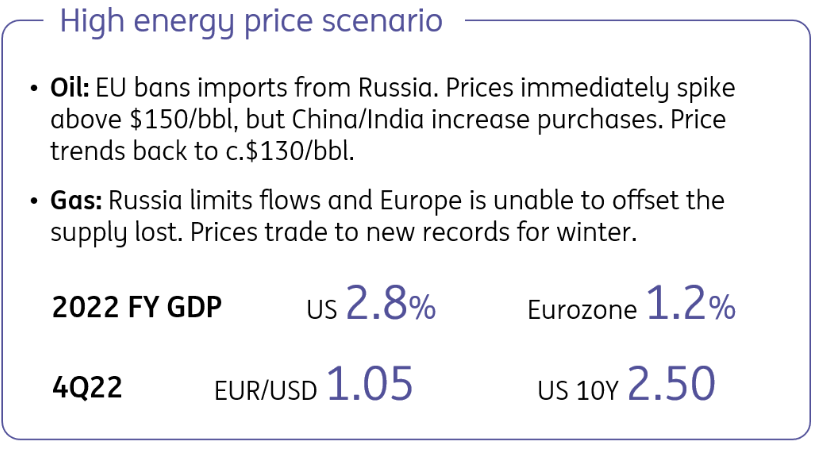

High energy price scenario: oil/gas sanctions introduced in Europe

The EU joins the US in banning Russian oil imports. Prices immediately spike higher, perhaps above $150/bbl, before trending down towards the $130/bbl area. We assume supply falls by four million barrels a day, but China and India increase their share of Russian oil purchases – though any secondary sanctions could see both become less willing to buy.

In response to further sanctions, Russia limits gas flows to Europe in this scenario, and Europe is unable to offset the supply loss. Gas prices trade to new records for next winter (TTF prices spiked to €345/MWh in early March and we are now trading back around €100/MWh).

Fuel switching (for example, to coal) takes place, as does demand destruction in industry. That’s most likely in areas like fertiliser, steel, and other chemicals production, which face a perfect storm of being energy-intensive, and often heavily exposed to critical inputs (notably metals) from Russia. Add in the more expensive fuel costs for shipping networks, and the overall cost impact on goods producers is substantial. Inflation is even higher in 2022 than in our base case and could reach double-digit levels in many countries.

Unemployment inevitably rises as large chunks of the heavy industrial process become deeply unprofitable and firms cut output dramatically. Despite having scope under EU state aid rules to support businesses, fiscal stimulus can only go so far.

That said, governments may come under pressure to reintroduce (or revive existing) short-time work schemes to support incomes. And in general, European leaders are forced to intervene more heavily to shield consumers from unaffordable price rises, though this is unlikely to be enough to prevent a consumer-led recession across Europe (including in the UK). Despite pressures, the EU is still reluctant to a new pan-European grant-based fund with pan-European borrowing.

European leaders are forced to intervene more heavily to shield consumers from unaffordable price rises, though this is unlikely to be enough to prevent a consumer-led recession

Interestingly, European wage growth is still likely to accelerate in 2022, given the role of inflation in negotiations – we saw something similar in 2008. But inevitably pressure falls thereafter. In the US, stubbornly high inflation slowly lures more workers back to the jobs market, reducing recent labour shortages. Both nominal and real wage growth is lower than in our base case.

That has important implications for profit margins. While costs rise sharply across the board, falling real incomes mean that – unlike during much of the pandemic – firms increasingly lack pricing power to pass these on. The result is greater margin pressure, adding to the wider recessionary environment.

The gulf between the US (Fed) and Europe (ECB, BoE) becomes very magnified in the short term. The Fed hikes 50bp repeatedly, taking policy rates well beyond neutral through the second half of 2022. This prompts a material correction in equities, while credit spreads increase. With household spending constrained, this is enough to tip the US into a recession by early 2023. This prompts the Fed to re-lower policy rates much earlier than currently anticipated. Quantitative tightening is paused.

The ECB continues or even increases the pace of asset purchases and a 2022 rate hike is off the cards.

High energy price scenario

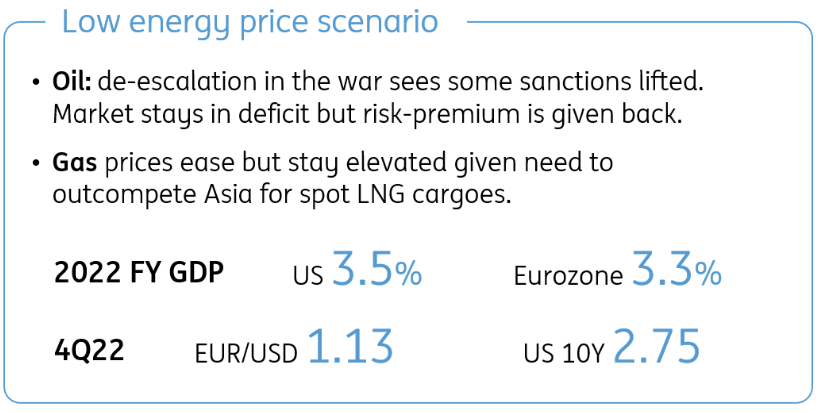

Lower energy price scenario: a peace agreement sees sanctions unwound

In this more positive scenario, led by some form of substantial de-escalation in the war, some sanctions are lifted. We still continue to see some near-term oil self-sanctioning (two million barrels/day in the second quarter), before easing as the year goes on to one million. The market is still in deficit, but much of the risk premium in prices is given back.

Gas prices would likely ease somewhat (back to pre-war levels), but Europe will still need to compete against Asia for spot LNG in order to replenish inventories. We think the best case scenario is that the EU manages to replace 55% of Russian gas this year, via more LNG and increased Dutch/Norwegian supply.

The downward move in prices extends to other commodities too. The impact of the war so far means further supply chain strains in the short term, but the situation improves gradually through 2022. Wait times at ports fall further, and investments in extra production capacity over the past 18 months begin to bear fruit. That means that some durable goods prices actually begin to fall later this year – used car prices are the obvious example.

This is the soft-landing many policymakers have been dreaming of for over a year

The upshot is that European economies avoid a recession, even if growth remains slower through the summer. Inflation falls back more quickly into late-2022 and in 2023, removing the pressure on disposable incomes. Indeed, the labour shortages currently being experienced in Europe persist, which continues to drive some modest wage growth but probably more in 2023 than in 2022.

For central banks, this is the economic soft-landing many policymakers have been dreaming of for over a year. The Fed no longer needs to hike quite as aggressively (the terminal rate can be a little lower), thus potentially negating the need to cut again from late 2023. The ECB steps up its gradual policy normalisation and hikes interest rates twice before the end of 2022, leaving the door open for additional rate hikes in 2023.

Low energy price scenario

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

ING Monthly: There’s nothing normal about the global economy

- This bundle contains 17 Articles