THINK Ahead: What if US inflation is much lower than we think?

James Smith’s indispensable guide to what you should be watching out for next week

What if US inflation is much lower than we think?

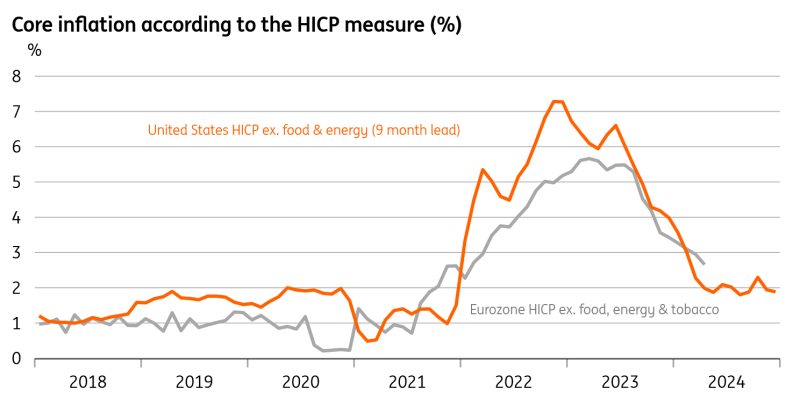

Here’s something that might surprise you: US core inflation is at 2% and has been since last July.

That might sound like a parallel universe. Certainly, it goes against everything we’ve heard about US inflation so far this year.

But here’s the thing, official data published in the US shows that if you calculate inflation in the same way we do here in Europe, then that is exactly what is happening.

Before getting too carried away, I should say that this is not the price gauge the Fed is watching. And markets can’t be blamed for not doing so either.

It’s a reminder, though, that the way we measure inflation matters – a lot. The US famously puts a much greater weight on housing than we do in Europe. And that helps to explain why the more mainstream CPI data puts core inflation up at 3.6%.

Even then, the numbers don’t always add up. James Knightley reckons next week’s PCE deflator – the Fed’s preferred inflation gauge – should look a little less worrisome than those CPI figures a couple of weeks back. Much of the discrepancy can be traced back to car insurance, which you’d think shouldn't be keeping policymakers up at night.

Anyway, if US inflation really is more benign than we’ve come to believe, then that can only be good news for Europe. Take the stat we mentioned right at the start. That “harmonised” measure of US core inflation has been a decent predictor of the eurozone data a few months down the road. Have a look at our chart of the week below.

It’s a relationship that holds when you look at individual categories, too. Things like food and consumer goods are still contributing more to inflation in Europe than in the US – particularly here in the UK - and America’s experience suggests that’s unlikely to be the case for long.

So when central banks here in Europe tell us there is nothing to fear from the recent resurgence in the US data, maybe they’ve got a point. Still, life’s rarely that straightforward. Services inflation is not helping the case for rate cuts here in Britain. And as Bert Colijn explains, a surprise pick-up in eurozone negotiated wage growth is a headache for the ECB, too. We’ll get fresh inflation data for the eurozone next week.

The lesson for markets is two-fold. If US inflation really is less worrisome, then the Fed has nothing to fear from rate cuts. Remember James K is betting on three rate cuts this year from September. That’s more than markets currently expect. And if eurozone inflation really is that similar to the US, then it’s hard to see the ECB going its own way on rate cuts for long. Just like the US, our team expects three cuts in the eurozone over the course of 2024.

Chart of the week: US 'harmonised' core inflation is a remarkable lead indicator for the eurozone

THINK ahead for developed markets

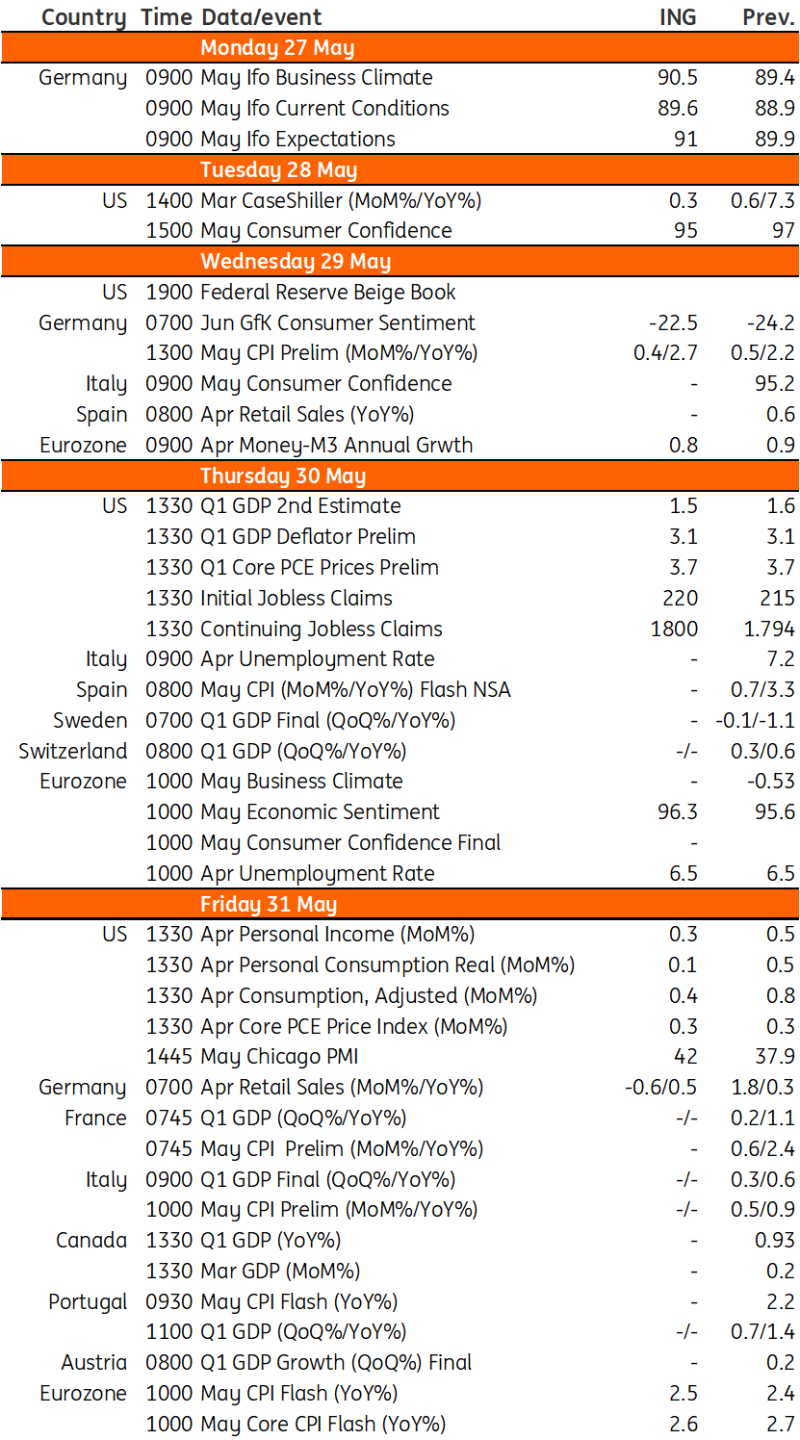

Eurozone unemployment rate (Thu); The eurozone unemployment rate has hovered around 6.5% for some time now. This is actually the lowest it has been since the eurozone started in 1999, which is an important reason to expect the ECB to be in no rush to cut rates aggressively. Recent labour market developments suggest continued labour market strength as businesses indicate that they continue to hire with economic activity picking up. But it will be hard to see unemployment go much lower. Beware of revisions, which happen often to eurozone unemployment but a stable reading for April seems to be in the making. Bert Colijn

Eurozone CPI/Core CPI (Fri): Ahead of the ECB meeting in early June, this is the most anticipated piece of data still to come out. Wage growth came in higher than expected which the ECB quickly dismissed as being related to one-offs. Still, if inflation surprises to the upside, the ECB will be less comfortable cutting as these things add up. There is not much reason to expect any ugly surprises here though. Headline inflation may tick up on the back of higher energy prices, but core inflation developments look relatively stable at the moment. Bert Colijn

THINK ahead for Central and Eastern Europe

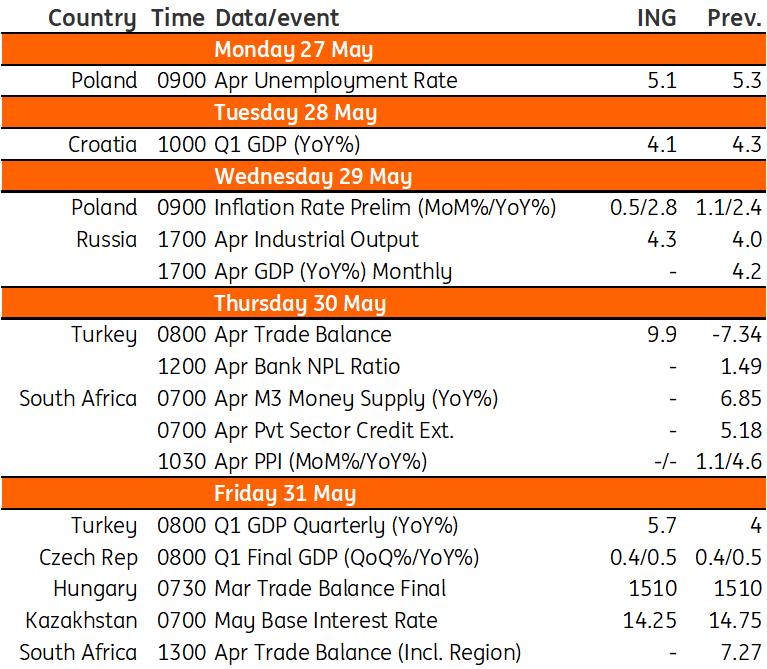

Poland CPI Inflation (Wed): In Poland, the StatOffice will release the flash estimate of May CPI inflation. Our preliminary forecast points to a further increase in inflation to 2.9% year-on-year from 2.4% YoY in April, continuing the upward trend. A further upswing in price dynamics was, in our view, mainly driven by annual increases in food and fuel prices. Rising inflation is among the factors that will prevent the MPC from cutting rates this year. Adam Antoniak

Czech Republic 1Q GDP Final (Fri): The final number for first quarter real GDP is expected to confirm the previous estimate of a 0.4% quarterly increase. That said, the elevated export numbers in the current account for March increase the likelihood of a possible upward revision of the recorded economic performance. The Statistical Office has announced that it will publish an extensive revision of the national accounts from 1990 onwards on 28 June, so major changes in the historical data are possible. Overall, strong retail sales and robust export performance signal a solid cyclical recovery underway. David Havrlant

Turkey 1Q GDP (Fri): 1Q GDP will likely be relatively strong due to fiscal effects and the minimum wage hike. Accordingly, we expect growth to be 5.7% YoY. However, following the surge in loan demand in the run-up to the local elections held at the end of March, the Central Bank of Turkey imposed restrictions on TRY-denominated loans. Recent data shows that these restrictions led to a sharp slowdown in credit growth. Accordingly, the GDP growth is expected to lose momentum in 2Q and 3Q due to the erosion in purchasing power, with continuing pricing pressures and tightening financial conditions after the CBT's actions in March. Muhammet Mercan

Key events in developed markets

Key events in EMEA next week

Download

Download article

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more