Low affordability to weigh on eurozone housing market in 2024

- 26 March 2024

- Real estate

One of the main reasons for last year's decline in demand for housing loans was the declining affordability of residential real estate. This year, due to the prospect of recovering house prices and limited downside potential for mortgage rates, the expected rise in wages is unlikely to improve purchasing affordability of residential real estate

Unfavourable affordability as one of the key drivers behind last year's housing market correction

Over the past two years, mortgage rates in the eurozone almost tripled. The resulting increase in financing costs has put a substantially heavier financial burden on prospective homebuyers and therefore lowered the affordability of residential real estate. The general rise in the cost of living – which has wiped out much of the nominal increase in wages – exacerbated the situation. Accordingly, many people decided to put their spending plans on hold, leading to a significant drop in demand for housing loans and downward pressure on house prices. While demand for housing loans fell by some 30% in 2023 year-on-year, house prices in the eurozone dropped by 2.2% from the peak reached in the third quarter of 2022 to the third quarter of 2023.

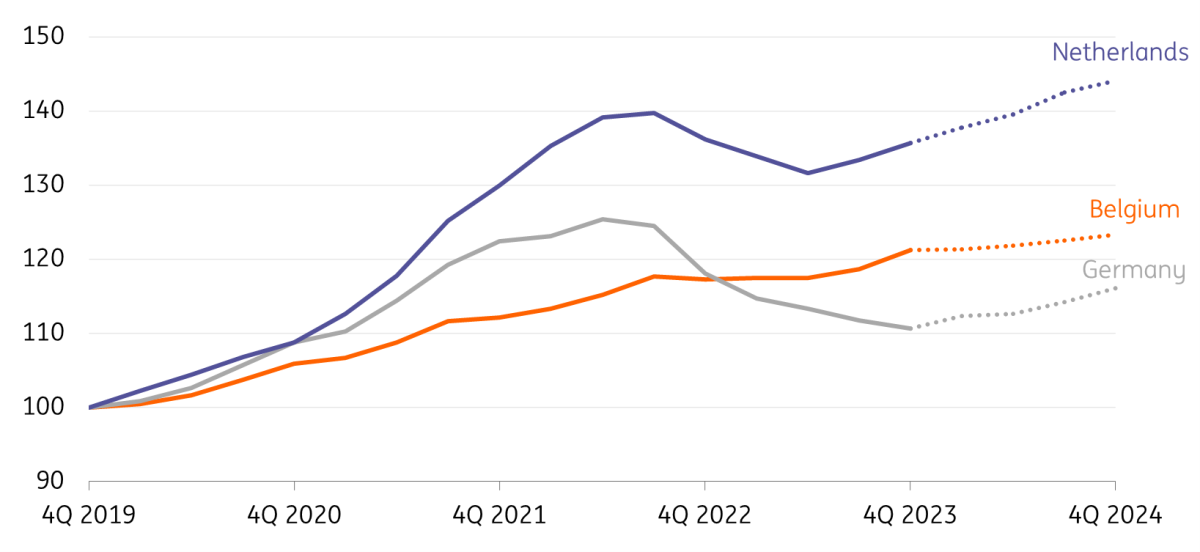

However, there were major differences in house price developments across the eurozone and the latest data from Belgium, Germany, and the Netherlands suggests that this divergent trend continued in the fourth quarter of 2023. In Germany, house prices fell by 2% quarter-on-quarter in the fourth quarter of 2023. This not only corresponds to a price decline of 8.4% for the full year of 2023, but also marks the first annual price decline since 2007. In the Netherlands, house prices fell by 2.9% year-on-year in the full year of 2023, although they started to rise again rapidly in the second half of the year, as illustrated by the 1.7% QoQ increase in the fourth quarter. As a result, house prices were almost back to their mid-2022 peak levels. In Belgium, on the other hand, average house price growth in 2023 was 2.5%. Here, the housing market was supported by the automatic wage indexation, which helped real purchasing power to hold up much better than in other countries, and by an extension of the average maturity at which households borrow.

House price correction to be followed by a modest rebound in prices

Looking ahead, house prices in the eurozone should recover slightly this year. While the structural supply deficit of housing is likely to be exacerbated by high material costs and the lack of skilled workers in the construction sector, a moderate increase in demand will probably put slight upward pressure on prices. However, regional differences will persist. The price decline of some 8% in 2023 is likely to be followed by an only marginal increase in house prices of less than 1% in Germany, leaving house prices well below their pre-interest rate turnaround levels. While we assume steady further growth in house prices of 3% in Belgium, house price growth is expected to accelerate in the Netherlands in 2024. Here, the limited supply of homes combined with increased borrowing capacity is expected to push house prices further upwards.

House price index (rebased to 4Q 2019=100)

Downward potential for mortgage rates limited, despite ECB to cut policy rates

The rise in mortgage interest rates and the corresponding increase in financing costs have been the main drivers of dropping residential real estate affordability. The development of lending rates is closely linked to long-term capital market interest rates. At the end of last year, long-term interest rates in the eurozone (as measured by the eurozone 10yr Interest Rate Swap rate) had fallen by more than 50bp due to financial market participants' expectations that the European Central Bank would cut key interest rates on a large scale this year. Accordingly, mortgage rates declined both in December and January.

10yr Interest Rate Swap rate (eurozone) and mortgage rate (in %)

The drop in mortgage rates was the most pronounced in Germany, with a drop of almost 40bp between November and January, fuelling a significant increase in demand for housing loans. Looking ahead, however, financing costs are not expected to ease significantly any further. As the ECB's future interest rate cuts are already priced in, it would require a surprisingly strong interest rate cut cycle that quickly reverses the rate hikes since July 2022 in order to provide additional downward potential for both capital market and mortgage interest rates.

Higher wages alone are not enough to improve affordability

Nominal wages in the eurozone have risen sharply over the past two years. However, they have not risen sufficiently to compensate for high inflation. Consequently, real wages contracted in every single quarter between the first quarter of 2021 and the second quarter of 2023. From the second half of 2023, the drop in headline inflation favoured a marginal increase in real wages – although this was not enough to offset real wage losses of the preceding two years. In addition to the rise in financing costs, this has amplified the decline in purchasing affordability of residential real estate.

Looking ahead, wage growth in the eurozone is likely to have peaked and should decelerate from here on. Nevertheless, nominal wage growth this year is expected to be stronger than in the past and, more importantly, stronger than inflation. In turn, real wages are likely to increase, thereby returning purchasing power to consumers. In Germany, where the latest wave of strikes demonstrates how strong wage pressure remains, real wages are likely to grow at the fastest pace since 2016. Real wage growth in the Netherlands is also likely to be stronger than in previous years despite a slowdown in nominal wage growth. In Belgium, where wages are linked to inflation, wages will rise more slowly than in other eurozone countries now that inflation has cooled considerably.

While the expected increase in real wages will have a favorable impact on the affordability of residential real estate, the high level of uncertainty and higher savings interest rates are likely to increase precautionary savings, so that any additional income is more likely to end up in savings accounts and not necessarily in real estate investments.

Housing market recovery set to be sluggish in 2024

Whether due to an expected sharp rise in house prices, as in the Netherlands, or due to a rebalancing market characterised by high uncertainty and no further easing of financing costs as in Germany or Belgium, the purchasing affordability of residential real estate is not expected to improve significantly this year. As a result, affordability will remain at historically low levels, which will lead only to a gradual recovery of the eurozone housing market.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more