Spanish housing market: is a correction looming?

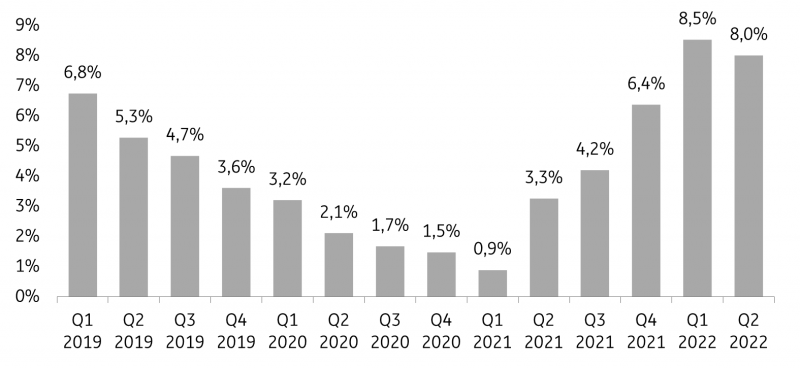

In the second quarter of 2022, Spanish property prices rose again by 8.0% year-on-year. Rising mortgage rates and a weakening economic outlook will dampen price growth from an expected 7% this year to 1% in 2023

Strong price growth continues, although we are past the peak

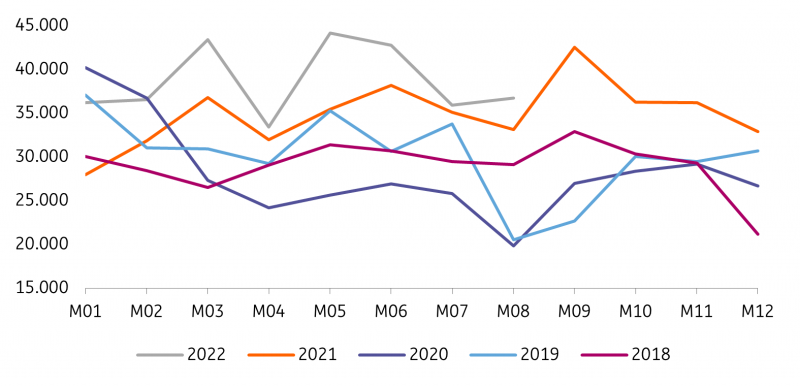

Spanish home prices rose 8.0% in the second quarter compared to the same period last year, a slight cooling compared to the first quarter of 2022, but price growth is still well above its historical average. On a quarterly basis, prices rose 1.9% in the second quarter compared to 2.6% in the first quarter. New and existing home prices showed similar trends, although the former rose slightly more strongly (+8.8% year-on-year) than the latter (+7.9% YoY). Figures from Tinsa, which include a monthly profile and are well correlated with the INE quarterly index, show a weakening trend over the summer. In July, Spanish house prices still rose by 3% month-on-month, but this slowed down to a growth of 0.5% MoM in September.

The start of the Covid-19 pandemic has turbocharged price growth in many countries. Since the start of 2020, prices of existing dwellings in Spain have increased by 11.5%. This is slightly weaker than price growth in Portugal (+26.2%) and France (+15.5%), but stronger than in Italy where prices have risen by 7.2% since the outbreak of the pandemic. These strong price dynamics during the pandemic stretched affordability to the limit. Combined with a cocktail of rising mortgage rates, deteriorating economic prospects and high inflation eroding household purchasing power, the real estate market will continue to cool. We expect price growth to reach 7% in 2022, but slow to 1% next year. This means that nominal price growth will not be able to keep up with inflation. With a current expected inflation rate of 8.7% for this year, real price growth will turn negative at -1.7%. At an expected inflation rate of 4.4%, real price growth in 2023 will also be negative at -3.4%.

Fig. 1. House price index, % YoY

INE, ING Research

Price growth starting to cool everywhere except in the metropolitan areas

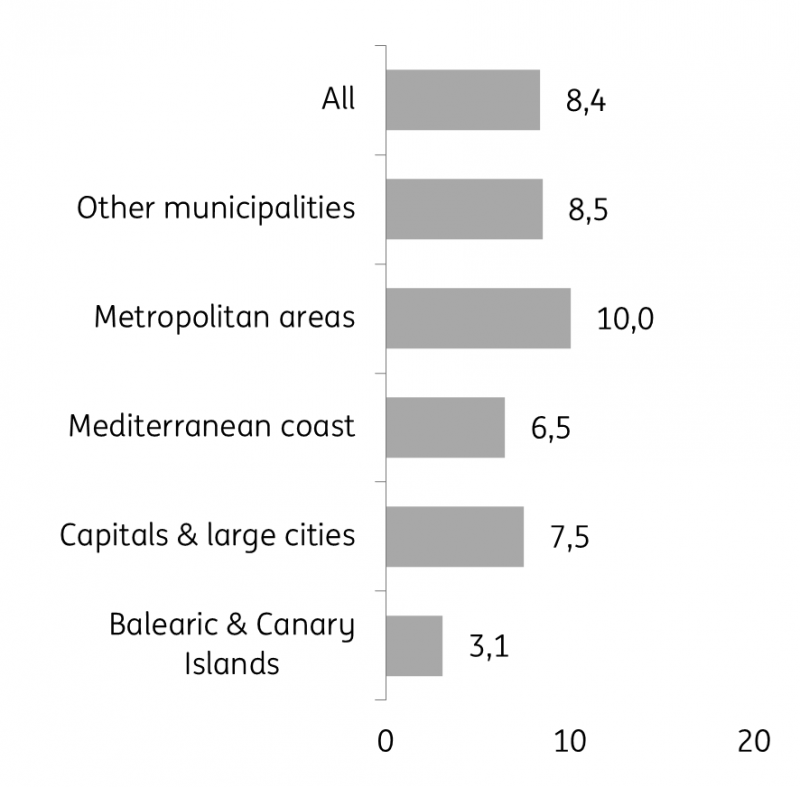

Although house prices have risen sharply in almost all of Spain, there are varying dynamics across regions and cities. The latest Tinsa figures for September show that price growth is beginning to cool off everywhere except in the metropolitan areas. Price dynamics have slowed down the most on the Mediterranean coast and in the Balearic and Canary Islands. Price growth of 6.5% on the Mediterranean coast and 3.5% in the Balearic and Canary Islands was well below the national average. On the Islands, in particular, price growth has come to a complete halt this year, even declining slightly over the summer. The cooling off does, however, come after strong price growth at the start of the pandemic. By comparison, in metropolitan areas, price growth continues unabated for now. Although house prices in the rest of Spain fell by an average of 0.4% compared to August, in metropolitan areas they still rose by 1.2% in one month, bringing the total annual growth rate in September to 10.0%.

Fig 2. House price index, % YoY, Sept ‘22

Tinsa, ING Research

Higher mortgage rates inhibit future price growth

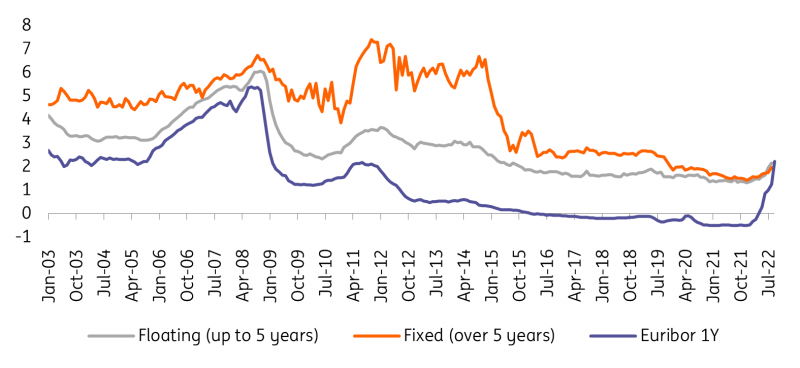

Mortgage rates have already risen sharply since the beginning of the year, and it’s unlikely that we have reached the peak yet. Mortgage rates closely follow the evolution of the 1-year Euribor, with a small lag. The 1-year Euribor has started to rise sharply. While the Euribor was still negative at -0.5 on 1 January, it rose to 2.7 in October. Although the 1-year Euribor already anticipated interest rate hikes by the European Central Bank (ECB) to combat inflation, further rate hikes could put some upward pressure on the Euribor again in the coming months. Nevertheless, we expect the Euribor to peak toward the end of the year. If the eurozone falls into recession, the ECB's willingness to raise interest rates further will also decrease.

Mortgage rates, which have also risen sharply this year, are likely to follow suit. The gap between Euribor and mortgage rates has narrowed significantly recently, suggesting that mortgage rates have yet to catch up. However, the biggest upside risk lies with floating rates. Although the gap between fixed and floating rates has narrowed significantly recently, floating rates tend to be well above fixed rates. Consequently, increases in floating rates will be more outspoken, while they will be more moderate for fixed rates. We expect mortgage rates to rise to around 3.4-3.6% for fixed rates and 3.9-4.1% for variable rates early next year before stabilising at their higher levels. These higher mortgage rates, which reduce households' borrowing capacity, will dampen housing demand and price growth.

Fig. 3. Fixed and floating rate of new loans for house purchase & Euribor 1Y

BDE, ING Research

Growing popularity of fixed interest rates continues

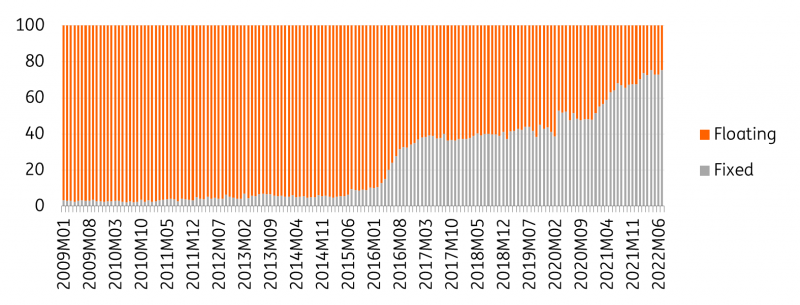

In the past, almost all mortgage loans had variable rates, but the number of new fixed-rate mortgages has been rising sharply since 2015. According to INE data, before 2015, the share of new fixed-rate loans was less than 5%, while accounting for more than half of all loans since 2021. Many Spanish homeowners have taken advantage of the low-interest rate environment in recent years to lock in their loan costs. The prospect of further interest rate hikes by the ECB and increasing uncertainty accelerated this trend. In July, three-in-four mortgage loans were at a fixed rate, which protects households from the sharp rise in mortgage rates as their monthly repayment burden remains stable. This keeps their creditworthiness intact, reducing the risks to the banking sector. Despite the popularity of fixed rates, floating-rate loans still represent the vast majority of total outstanding mortgages.

Fig. 4. Share of mortgage loans for dwellings with a fixed vs floating rate

INE, ING Research

Transaction data remain strong, but we expect momentum to slow

The sales figures for August recently published by INE do not (yet) show a weakening in the number of transactions. The number of transactions in August 2022 were still almost 15% higher than in the same month last year, which was already an exceptionally strong year in terms of transactions. If we compare with the pre-Covid period, the number of transactions in August was still 60% and 28% higher than in August 2019 and 2018, respectively. For the coming quarters, we expect the number of transactions to start declining. The cost-of-living crisis is putting strong downward pressure on real disposable income, combined with rapidly rising mortgage rates and weakening economic growth, which are creating strong headwinds for the property market. We expect the Spanish economy to dip into a mild recession from the fourth quarter onwards.

Fig. 5. Number of transactions, 2019-August 2022

INE, ING Research

Mortgage production still well above pre-Covid levels

Despite higher mortgage rates, mortgage production is holding up well for now. In the first eight months of this year, 14% more mortgages were issued than in the same period last year, and 2021 was already a strong year in terms of mortgage production. If we compare this to 2019, the year before Covid-19, the number of new mortgages in 2022 is up to 24% higher. In August, the last month for which figures are available, the number of new mortgages was still 10.9% higher than the same month last year. It is likely that many homeowners still took advantage of low interest rates in the first half of the year to refinance their existing mortgage loans at a fixed rate. Potential homebuyers also probably tried to get ahead of rising interest rates by accelerating their property purchases. Both factors will have boosted mortgage production in the first half of the year, but this effect will gradually diminish. Furthermore, increasing household pessimism and less favourable credit conditions will dampen demand for real estate, putting downward pressure on mortgage production.

Consumer confidence has deteriorated significantly in recent months, which shows that households are increasingly concerned about high inflation amid economic uncertainty. Consumer confidence has now fallen below the low seen at the beginning of the pandemic, and is now at its lowest level in almost 10 years. This could prompt potential home buyers to postpone their purchase decision in the coming months. The latest European Commission survey that gauges Spaniards' buying intentions to buy a home in the next 12 months is holding up much better for now than in other European countries, but has also weakened somewhat over the past year. During the Covid pandemic, the index had risen to its highest level since 2010. Although the index is still historically high, we see a downward trend in 2022.

Fig. 6. Mortgage production for dwellings, 2019- August 2022

INE, ING Research

Strong household growth and falling supply are likely to support price growth

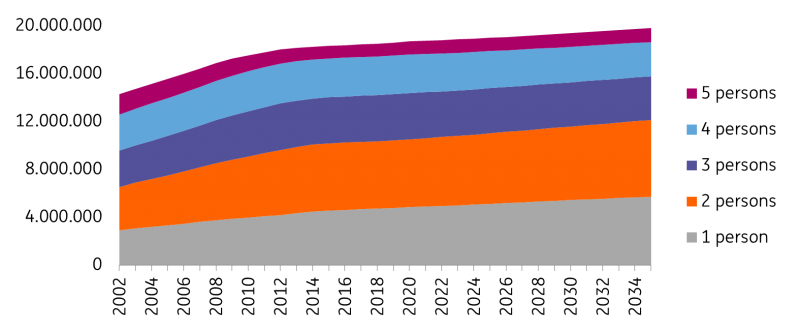

On the other hand, structural growth in the number of households will support the real estate market over the coming years. Due to strong household thinning, the number of households is increasing faster than population growth, which supports the demand side of the real estate market. Over the past 20 years, more than 20 million households have been added, a 70% increase. Between 2002 and 2012, the number of households increased particularly sharply with an average annual growth rate of 2.4%. The growth rate has slowed to an average of 0.4% per year over the past decade, but has continued unabated.

In the years ahead, household growth will continue to support the real estate market. INE forecasts that the number of households will increase by 1.1 million by 2035, a 5.3% increase in 13 years. This is mainly due to strong growth in the number of single and two-person families. These two groups are expected to grow by 16% and 11%, respectively, while the number of households with more than three people will shrink by about 5%. Spain already has a high proportion of flats (66%), compared with, for example, France (34%), Italy (55%) and Portugal (46%), but this proportion is likely to increase further over the next decade driven by a growing number of singles. In 2035, single people will account for 29% of all households, up from 26% in 2022 and 20% in 2002.

Moreover, supply is rising less rapidly than the number of households, which naturally puts upward pressure on prices. Between 2011 and 2021, the number of households increased by 5.4%, while the housing stock increased by only 2.9% over the same period, according to figures from the Ministry of Transport. For this year and next, we forecast a further decline in construction volumes, which will put additional pressure on the property market. The sharp rise in the cost of building materials puts an extra brake on construction activity. Production levels are currently more than 20% lower than before the Covid pandemic and we expect the sector to shrink for the fourth year in a row. For next year, we expect some marginal recovery. The upward trend in costs seems to have slowed. In addition, the Spanish construction sector will see some positive effects from investments in the EU recovery funds. Nevertheless, the number of households is also expected to continue to grow faster than the property supply in the coming years, fuelling price growth.

Fig. 7. Evolution of the total number of households, 2002-2035

INE, ING Research

Affordability under pressure, especially for low-income earners

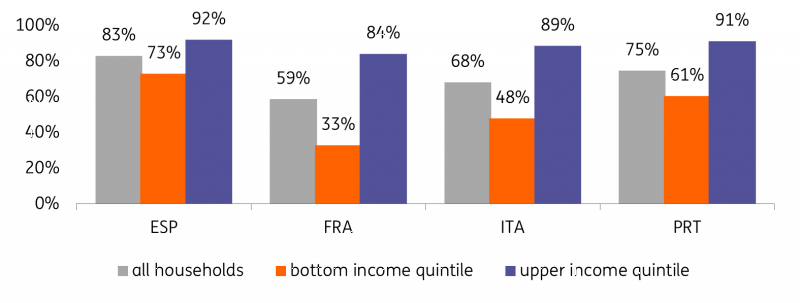

Property market inequality is relatively low in Spain. Compared to other European countries, home ownership in Spain is relatively high among low-income earners. According to Eurostat data, 73% of households in the lowest quintile are homeowners; only Hungary (78%) and Slovakia (80%) score better, and the proportion is much higher than in, for example, Italy (48%), Portugal (61%) and France (33%). The gap between the bottom and upper quintile is also much lower than in other European countries. However, the strong price increases in recent years combined with higher mortgage interest rates and declining purchasing power due to high inflation have put pressure on affordability, especially for lower-income earners. The housing cost overburden rate, or the proportion of the population living in households that spend 40% or more of their disposable income on housing, was 9.9% in 2021 compared to 8.2% in 2020. This is well above many other European countries, including Italy (7.2%), France (5.6%) and Portugal (5.9%).

Fig. 8. Homeownership across the income distribution

OECD, ING Research

Increasing focus on energy efficiency

Rising energy prices and high energy bills are a game-changer, including in the real estate market. We expect that when purchasing a home, more attention will be paid to energy efficiency, which will influence price trends. The price differences between energy-efficient homes and energy-wasting homes will increase in the coming years. There is increasing evidence from different countries of a clear relationship between the energy efficiency of a property and transaction prices. A one-letter improvement in a property’s energy performance certificate (or EPC) is estimated to increase the price by 8% in Austria, 4.3% in France and 2.8% in Ireland. In Belgium, research shows that a significant improvement in energy efficiency is associated with a 4.3% higher (advertised) price. Also, in Portugal, there is a significant relationship between eco-friendly dwellings (EPC value of A or B) and the median sales value per m². Most of this research predates the sharp rise in energy prices this year. Therefore, we expect these effects to have increased significantly by now.

In Spain, there is no convincing scientific evidence (yet) that houses with a better energy label (A or B) are sold at a higher price. Owners and sellers have no incentive to disclose their EPC score. As a result, houses with low energy scores can be sold at the same price as houses with good energy scores. Although generally favourable, climate conditions play in Spain's favour compared to more northern European countries (though cooling might become an issue if the climate warms up further), so the importance of energy efficiency for both home buyers and sellers will continue to increase, which will also lead to price differences in Spain. Sellers of energy-efficient homes have a strong competitive advantage that they can exploit. Anecdotal evidence also shows increasing interest in energy efficiency among home buyers. The more energy-efficient the home, the more it can reduce energy bills and thus generate savings. Moreover, increasingly stringent regulations will further accelerate the turnaround in the coming years.

We anticipate a soft landing in 2023

Although we expect a further cooling of the Spanish real estate market, a severe correction is unlikely. We expect the price level to be close to a peak and may fall slightly over the next two quarters. Currently, we expect a slight price drop during the winter months before recovering. In this way, we still arrive at 7% price growth for 2022 and 1% for 2023, considerably less than inflation. Real price growth will turn negative, expected to be -1.7% for this year and -3.4% for next year. Uncertainty, rising interest rates and a looming recession will dampen price growth. We expect the Spanish economy to fall into a mild recession from the next quarter onwards, which also makes the labour market outlook less rosy.

Moreover, household purchasing power is already under severe pressure from high inflation and energy prices. While the prospect of rising interest rates may temporarily cause households to speed up their buying process to get ahead of rising interest rates, this effect will gradually disappear. On the other hand, demand for property remains strong (for now). Both the number of transactions and mortgage production are still at very high levels. A supply that increases less rapidly than the number of households will continue to put upward pressure on prices. Spanish house prices have risen less rapidly than in most other European countries, which also makes a correction less likely.

Download

Download articleAuthor

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more