The construction sector’s sinking circular foundations

Eurozone construction companies may have ambitions to improve circularity in their sector, but rising waste levels show things are not going to plan. While the circularity rate of building materials is higher than that of the EU economy overall, we're seeing signs of stagnation. Circular construction goals are starting to slip out of reach

Progress halted by construction waste

In the path toward creating a circular economy, the process of reducing waste levels is absolutely crucial – and we're seeing this take place slowly but surely in the European Union's economy as a whole. The total amount of waste has decreased by almost 3% in the last decade and by approximately 8% in the manufacturing sector.

However, it seems the opposite has occurred in the construction sector, with the amount of waste growing by more than 6% from 2010-2020. Construction waste refers to the waste and debris generated from building, renovation and maintenance, demolition and construction site clearance. This includes materials such as concrete, wood, metals, bricks, insulation materials, glass and plastics. And we'll be trying to understand the reasons why in the report.

It's important to consider the role of the European Commission in all this. As the green transition route continues to evolve, the EC presented a number of measures dedicated to making sustainable products the norm. The European Green Deal package, introduced last year, is set to play a major role in moving progress along. A key part of the proposal is the revision of the Construction Products Regulation, which aims to make the design and manufacture of construction products more durable, recyclable and easier to re-use.

But as we try to move closer to developing a circular economy, the construction industry is still a huge waste producer; in 2020, it contributed 37% of total waste in the EU.

Tonnes of waste generation in construction sector increases

Development total waste generation in EU-27 in absolute tonnes (not corrected for production volume development), Index 2010=100

What's going on?

Construction waste increases as production volumes fall

Transitioning towards a circular economy should signal a drop in the amount of waste in tonnes. An increase in production levels could provide one explanation for rising levels – yet, in relative terms, waste generation in the construction sector only appears to have worsened. The sector faced a drop in production levels by 7.6% in the years 2010-2020, while the manufacturing sector experienced a rise of 11.6% and all economic activity grew by 8.1% in the same period. As a result, the level of construction waste per unit output has increased even further.

Labour shortages and more renovation

We see two possible reasons for the increased amount of waste in the construction sector. Due to the shortage of workers, construction companies may opt for new materials instead of reusing old ones, as the latter can be more labour-intensive. Additionally, the share of the renovation and maintenance market has increased in recent years. Both the demolition and removal of existing building materials mean that renovation projects often generate more waste than new construction.

Contributions to waste in the EU

As we move closer to developing a circular economy, it is very important to pay attention to the construction sector as a huge producer of waste. In 2020, it contributed 37% of total waste in the EU.

Construction sectors produce more than a third of all EU waste

Share of generation of total waste in tonnes in EU-27, 2020

High-grade and low-grade circular construction

There are many different circular construction methods. The best option is to reuse high-grade building materials and parts – or even to repurpose the buildings themselves. In the construction sector, this is often seen in the transformation or renovation of existing buildings. Recycling should only be used as a last resort.

For instance, a wooden frame has a much higher value than the wood it is made of – and the circular economy is heavily centred around retaining as much value as possible. The more buildings we're able to repurpose and building material parts that can be reused, the better.

The difference between high and low-grade circular construction

Circularity stopped short in key initial stages

Circularity was typically not taken into consideration during the design stages for many buildings. Materials are also difficult to reuse for a number of reasons:

- In the design phase of the structure, the architect or engineer may not have taken the reuse of building materials into account

- Many used building materials are customised and don’t have standard measures, which makes reusing them difficult and less appealing

- Separating construction waste materials can often be challenging. For example, bricks are typically held together with cement, making it almost impossible to separate them for reuse

A high-grade circularity of building materials is often technically and economically unattractive, and as a result, many materials end up as rubble. This is typically why we see such low-grade reuse of construction waste.

Different ways to measure circularity

There are different ways to measure circular construction. The recovery rate is an indicator of the ratio of construction and demolition waste, which is prepared for re-use and recycling or subject to material recovery. This includes backfilling: when old concrete is crushed down and used as a filling to support or strengthen structures and groundwork. Backfilling is the lowest level in circular construction and is essentially downcycling.

The circularity rate indicates the share of material recycled (excluding backfilling) and brought back into the cycle, which saves the use of raw materials. This measure outlines the ratio of the circular use of materials (excluding backfilling) to the overall material use.

High recovery rate in construction

Enormous amounts of construction waste are brought back into the cycle. According to Eurostat data, almost all construction and demolition waste is recovered in Belgium and the Netherlands. In addition, the recovery rate in the European Union is 89%. But is this high-grade or low-grade circular construction and backfilling?

Almost 90% of construction waste is recovered

Recovery rate of construction and demolition waste in 2020

The construction circularity rate (excluding backfilling) isn’t available for the EU. We can, however, take a look at the circular material rate for a bit more insight. This rate is only available for the building product group of concrete, cement, bricks and plaster – but these materials make up the bulk of construction waste.

Circularity rate for main building materials stagnates

Although building materials are often difficult to reuse, the circularity rate of concrete, cement bricks and plaster reached 14% in 2021. This means that 14% of material resources used in the industry came from recycled products and recovered materials, saving on the use of primary raw materials.

This is more than 2 percentage points higher than in the EU economy overall – but it now appears to be losing steam. While the circularity rate of all materials in the EU has increased from 10.8% to 11.7% since 2010, the circularity rate of main building materials hasn’t seen any improvement at all.

Stable circularity rate of building materials

Development circular material use rate by material type

Moving towards a more circular construction sector

Circular construction model: entire supply chain involved

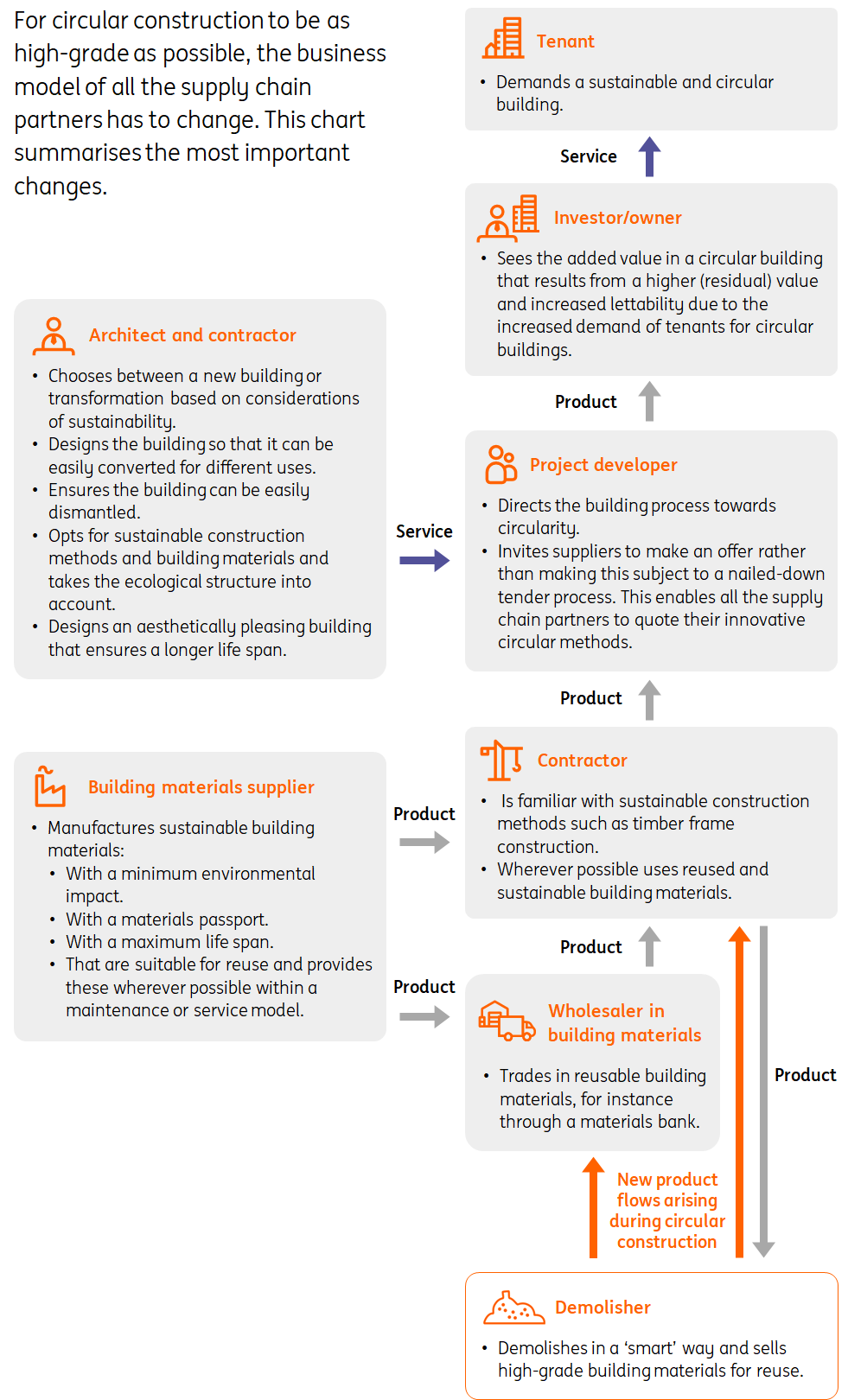

In order to change course, begin reducing construction waste and increase the circularity rate, not only contractors but the whole construction value chain must be involved. For circular construction to be as high-grade as possible, the business model of all supply chain partners has to change. Architects and owners have to decide whether old buildings will be reused or demolished, as well as how buildings can be easily converted for new owners.

All supply chain partners need to embrace circular principles to make the process a success.

For instance, they may opt for more sustainable construction methods such as timber construction. Suppliers can offer bio-based materials (e.g. wood, straw, flax and hemp), and demolishers can ensure that building materials are reused at the highest possible grade. All supply chain partners – from owner and architect to demolisher – need to embrace circular principles to make the process a success.

Most opportunities for wholesalers and demolishers

For demolishers, opportunities exist in circular construction through smart demolition. They can extract whole building parts from a demolition site by dismantling the building in a way that specifically allows these parts to be reused. Distribution of such materials provides new opportunities for wholesalers, who have networks of contractors and can therefore buy used building materials to sell again. If the trend of circular construction continues, this will result in fewer sales of new building materials for suppliers, as "old" building materials are reused more frequently.

The chart below summarises the most important changes to be made for the circular construction process to be able to take place. See further our circular construction report which answers the following questions:

- Is there a demand for circular construction?

- How does circular construction work?

- What are the limitations?

- What role does ‘from ownership to use’ play and for which supply chain partners are there opportunities?

How does circular construction work?

Who does what?

An increasing number of construction companies have ambitions in circular construction. Several large European construction companies are trying to promote circular construction, decreasing the amount of waste and improving the circularity rate. Here are some examples:

Bouygues Construction

Bouygues Construction is transforming its building processes in the supply chain to implement circular economy strategies. To do so, they've outlined four priorities: selecting sustainable and recyclable materials in the design phase, reducing the amount of resources used during construction, recovering and re-using materials on-site and recycling materials. At Hôtel des Postes, Bouygues re-used structural components, doors and external joinery along with various other building parts. For instance, they repurposed the old carpet for new insulation.

Skanska

Skanska focuses on resource efficiency by reusing and recycling materials and products where possible. Concrete, demolition waste, mixed construction waste and wood are the four largest waste types for the company. They reduce waste with smarter design, planning, procurement and logistics.

In 2022, 72% of total waste was recycled, 8% was set for reuse and 13% received another waste treatment. 6.8% of generated waste went to landfill, which does not yet meet the company's target of less than 5%. Skanska applied circular solutions during the construction of the office building Epic in Malmö, using concrete from the Copenhagen metro, excess bricks from the Epic façade, window frames and beams from other demolition projects, and recycled PET bottles for sound-absorbing canvas in the façade.

Hochtief

Hochtief has a sustainability plan, with goals for 2025 outlining various targets. Circularity is just one of the dimensions, with targets including an 80% recycling rate of waste in 2025 and a consecutive increase thereafter. In 2022, the recycling rate hit 88.7% – already exceeding the original target.

Promoting life-cycle analyses by actively engaging clients in at least 200 building projects in 2025 is yet another target. Hochtief also intends to increase the proportion of projects in which the used materials are digitally logged by at least 10% per year, which should make the reuse and dismantling of used building materials simpler.

Royal BAM Group

Circularity is one of the six key themes for BAM’s sustainability strategy. In the short term, it aims to enhance the transparency of material usage and offer circular construction methods. The company's circular construction initiatives include the "Madaster Platform", a digital tool that documents the materials used in construction projects and promotes their reuse.

By 2030, BAM plans to reduce non-biobased materials by 50% compared to 2019 levels. Additionally, the company strive to reduce its production construction process and office waste by 75% by 2030 compared to 2015 levels.

Looking ahead, cooperation remains key

It's now become critical for a real shift to take place in the construction sector if rising waste levels are to have any chance of falling. Stronger regulation could solve one part of the puzzle, but the transition needs to be covered every step of the way – from clients and contractors to demolishers and the building material industry.

Larger construction companies are already adopting circular policies to help turn the tide, but smaller companies must also step up efforts for any real change to occur. The construction sector is very fragmented, with a high number of these smaller firms playing a key role – and it's crucial that action comes from all sides moving forward.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more