Singapore exports yet to see virus impact

- 17 March 2020

- Singapore

We believe the Monetary Authority of Singapore will see through the surprisingly positive exports data and move to an easing path, more likely before the scheduled policy review in April

| 3% |

NODX growth in FebruaryYear-on-year |

| Higher than expected | |

Positive February NODX surprise…

Singapore’s non-oil domestic exports surprised with 3% year-on-year growth in February, a significant outperformance compared to the consensus, which was looking for about a 7% fall. Clearly, the consensus view was based on a hit to global demand from the Covid-19 outbreak, though the disease only started to spread globally (beyond China) in late February and the data has yet to reflect the complete impact, which is probably something we will see in the March data.

However, if there is anything reflecting the impact of the virus, it’s the 36% year-on-year plunge in shipments to China as the outbreak was peaking. China (and Hong Kong) absorbs about one-fourth of total NODX. The other main export destinations were rather buoyant, with shipments to Europe surging by 43% YoY, to the US by 23%, and to Japan by 62%, though all these strong gains are poised to be reversed in March. By main sectors, electronics stood out with 2.5% growth, the first positive in over a year and in stark contrast to the consensus of a 17% YoY fall. Pharmaceuticals also helped with strong gains.

… is no reason for the MAS to relax

This leaves NODX in the first two months almost flat from a year ago. The real test of the impact of Covid-19 on the economy will come in the March data when all the strength of the first two months is at risk of being scaled back, making this the most dismal quarter for GDP growth since the 2008 global financial crisis. Indeed, Prime Minister Lee Hsien Loong has warned that the fallout could be worse than the global financial crisis. We remain of the view that the added drags from weak exports, tourism and persistently weak domestic spending could nudge the economy into a recession in the first half of the year.

The Singapore Dollar money market and foreign exchange market are functioning normally in the face of heightened volatility in global and domestic financial markets. - MAS statement Friday.

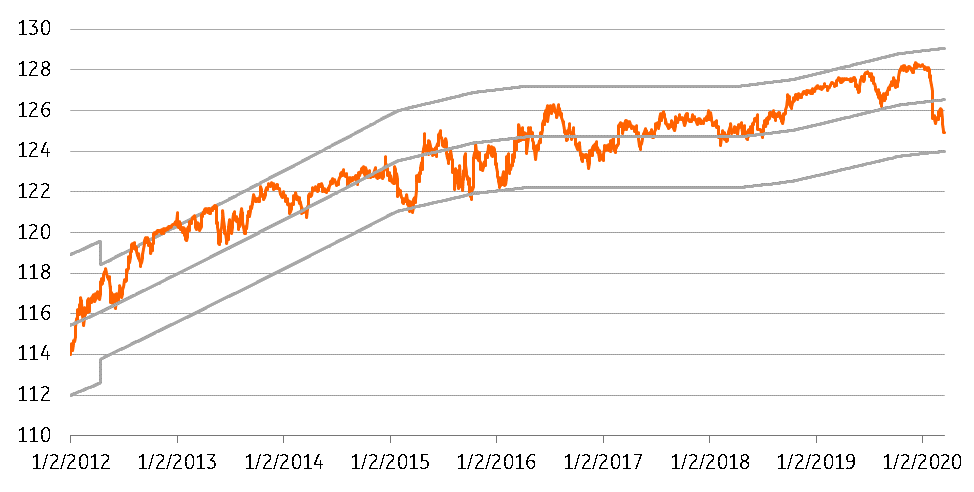

Meanwhile, we think the Monetary Authority of Singapore (MAS) will see through the positive February NODX figure and join the global central bank easing bandwagon. We expect it to ease by re-centering the Singapore dollar Nominal Effective Exchange Rate policy band at a lower level (currently about 1.3% below the mid-point of the band) and flattening the rate of appreciation. While the Fed’s second emergency rate cut on Sunday gave global central banks room to move off-cycle, the MAS has yet to come to terms with this situation. It may not be this way for too long though. An easing ahead of the next scheduled policy review in April seems more likely than not, in our view.

S$-NEER policy band

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more