Russia-Ukraine crisis to reshape supply chains, flatten world trade

- 11 March 2022

- Transport & Logistics

The improvement in global supply chains has ended before it ever really began. The war in Ukraine will bring longer-lasting disruption and the trade outlook will bear the consequences of sanctions. Expect a new round of delays and protracted supply shortages

Supply chains: a new round of challenges

The war in Ukraine is putting global supply chains to the test again. Even before the conflict began, supply chain frictions had only improved marginally from the pandemic. While container handling had picked up significantly in many regions, schedule reliability - the actual on-time performance of individual vessel arrivals in ports tracked by Sea-Intelligence - dropped to 30.9%, marking a new all-time low. In terms of shipping rates, there has been some relief in the spot market, but the shift to long term contracts has meant that higher container tariffs are now locked in.

Russia and Ukraine: no major EU trade partners, but closely linked to several countries

The share of Ukraine’s global goods imports and exports only amounts to 0.3% each, while Russia’s export share is 1.9% and its import share is 1.4%. However, although the share in world goods trade is small for both countries, they are crucial oil, gas and grains exporters and have close links to Baltic states and other Eastern European countries, namely Lithuania, Bulgaria, Finland, and Latvia. On average, almost 40% of trade in these four countries was linked to Russia between 2015 and 2020, not only through goods imports and exports, but also through value added as partners in supply chains. Lithuania and Bulgaria have particularly close ties in this regard; Russian value-added as a percentage of final demand is roughly 6% in both countries. The trade share with Ukraine between 2015 and 2020 was far smaller, with Lithuania (1.9%), Hungary (1.7%) and Poland (1.5%) seeing the highest shares.

Sanctions are a blow for European trade with Russia and transit traffic

EU countries have banned exports of a range of high-tech products, equipment, materials, and machinery to Russia and extended the scope of sanctions to Belarus. These products cover at least 40% of the export package to Russia based on the EU sanctions list. Formal sanctions, in addition to extensive self-sanctioning, will have a strong impact on trade this year. Shipments to and from Russia have been banned, resulting in stagnating commodity flows. Due to the closure of Russian airspace, air freight traffic is being hindered. In addition, rail transport between Asia and Europe via Ukraine on the ‘Silk Road’ has been impeded, making transportation through both countries highly uncertain. In terms of tonnage, air cargo covers only 1% of world trade and the Silk Road takes 1-2% of container traffic between Asia and Europe. But in terms of value, this takes a much bigger share, as higher valued (consumer) products like electronics, pharmaceuticals and high-end agriproducts could be involved. According to the Kiel Trade Indicator, world trade could decline by 5.6% in February compared with the previous month, even though the conflict only started to escalate in the last week of February.

Distortion of commodity markets and trade impacts supply chains the most

The biggest hit to supply chains would come from any severe disruption to Russian energy exports, as several European countries are dependent on Russia for energy. But even in the absence of this, there are more challenges to come. In addition to exporting agricultural products such as wheat, corn, and sunflower oil (India, China, the Netherlands, and Egypt are large consumers) both Ukraine and Russia export large amounts of steel, palladium, platinum, and nickel, among others.

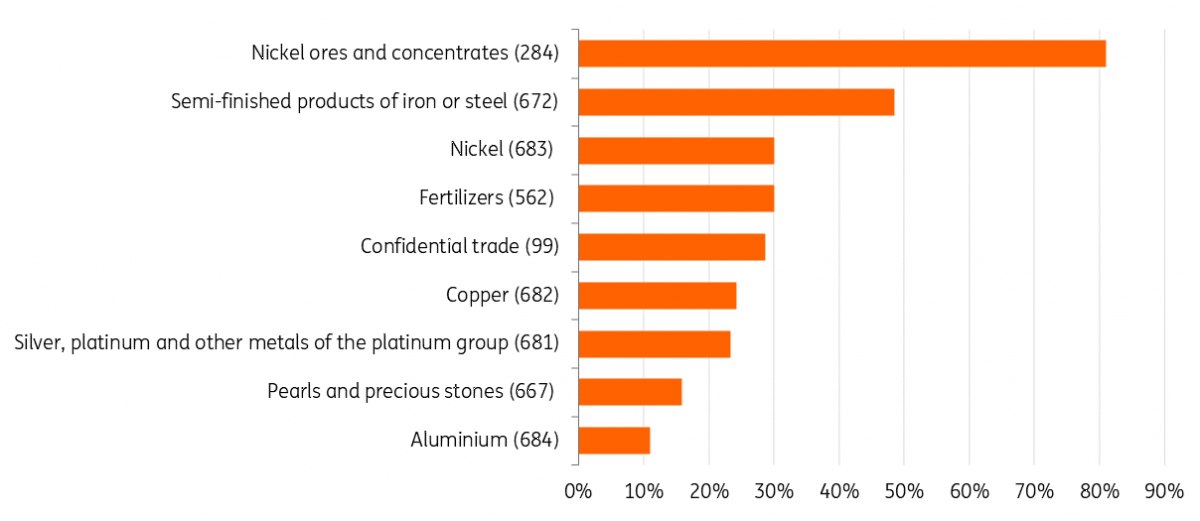

Selected imports from Russia based on most traded goods between EU and Russia %-share of Extra-EU imports

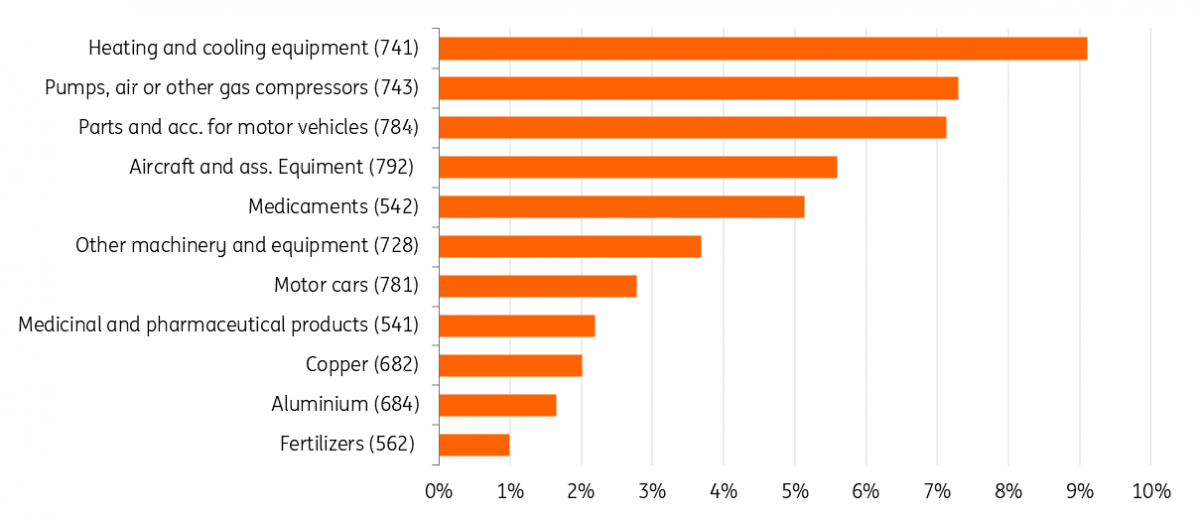

Selected exports to Russia based on most traded goods between EU and Russia %-share of Extra-EU exports

In fact, 81% of nickel ores and concentrates of the EU’s Extra EU-27 imports come from Russia. Specifically, the EU gets 30.1% of its nickel imports, 48.5% of semi-finished products of iron or steel and more than 20% of copper and platinum from Russia. Belgium and Denmark receive over 90% of their Extra-EU share of semi-finished steel from Russia while Latvia relies on Russia for 92% of its fertilisers. Russia’s share in German Extra-EU imports for semi-finished iron or steel products amounts to 74% and 46.1% for copper. Even if the trading amounts are not always high, there are clear dependencies in some areas.

Automotive sector already faces supply chain consequences

The automotive industry, in particular, faces renewed operational problems because of the war, while the semiconductor shortage continues to drag on. BMW and VW have already seen production interrupted at European sites due to disruptions in the supply of components from Ukraine, such as wire harnesses. This affects both the production of conventional cars and electric vehicles, with some lead times extending into next year.

Avoidance of Russian ports and mutual closing of air space leads to new inefficiency and less air cargo capacity

Overseas: Self-imposed restrictions by exporting European companies and the looming closure of ports for Russian vessels as well as re-routing to avoid affected areas are creating delays and uncertainty. Some of the world’s largest container carriers including MSC, Maersk, CMA CGM and Hapag Lloyd, controlling about 60% of global container shipping, have suspended bookings of nonessential cargo to and from Russia and partially also Ukraine due to safety reasons. Consequently, cargo for these destinations is piling up in ports. But even if cargo is still shipped to Russia – and payment can be accepted – it will still receive extra customs inspection due to the sanctions in place, delaying handling and shipments in European ports. Some 10% of the total annual container throughput at the port of Rotterdam, Europe’s largest port, is linked to Russia and 13% of its total volume, with large amounts of heavy crude oil, LNG and coal. Rotterdam serves also as a hub for several metals. About 5% of throughput is linked to Russia at the second and third largest European ports, Antwerp and Hamburg. But this is not limited to shipping and seaports, as air traffic is perhaps even more affected.

Overland and through the air: The blockage of the Ukraine rail route has already limited transport capacity and detours have to be made by air. Consequently, capacity is suffering from new reductions due to inefficiencies and loss of freight capacity. For example, Lufthansa anticipates a 10% capacity reduction on the Asia-Europe route due to the conflict between Russia and Ukraine. And one of the world's largest cargo-only carriers, Airbridge cargo, is also based in Russia. On top of this, soaring fuel prices are significantly pushing up transport costs. Another large airfreight carrier, Cargolux, introduced a surcharge because of the implications of the war for capacity and routes.

Shortage of workers: 10.5% of all seafarers come from Russia and 4% from Ukraine, according to the International Chamber of Shipping. In the Black sea, many crewed vessels are stuck due to hostilities and port closures. The closure of airspace makes travelling and relocation for seafarers more difficult as well. The truck driver shortage in Europe could also intensify as an estimated 4,000 to 5,000 truck drivers are held up in Ukraine, according to IRU. Although this is only a fraction of the 3.8 million heavy truck and bus drivers employed in the EU, it intensifies the shortage of 400,000 truck drivers across the EU.

What does this mean for supply chains and our trade outlook?

Delays and congestion suggest longer-lasting problems for supply chains. Sailing and air freight schemes have to be reorganised and delays will intensify as Russian products are subject to sanctions, meaning that container cargo destined for Russia will receive extra customs inspection. Delivery of crucial preliminary products to European manufacturers will be delayed, if they arrive at all. On top of that, scarcity and delays mean further price pressures, resulting in rising prices for producers and consumers.

World trade will weaken more sharply than previously expected. Following the pandemic, continued supply chain troubles and higher inflation and shipping costs pose further downside risks to our trade outlook. Sanctions on several products previously exported to Russia, voluntary bans on exports and efforts to reduce oil and gas imports will all hit global trade this year. Nevertheless, we continue to expect some growth in world trade volume in 2022. The US economy and the Asian region ex-China have limited direct economic linkages to the area, speaking in favour of continued trade, although they are not immune to the indirect consequences of this conflict, such as a sharp drop in demand from Europe. Trade growth might hover just above the 0% area if the war drags on. But whatever happens, trade flows will be significantly reshaped.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

This article is part of the following bundle

A global power struggle

- This bundle contains 9 Articles